June 4, 2025

USDCAD open 1.3714, overnight range 1.3694-1.3732, close 1.3721

USDCAD is treading water ahead of today’s Bank of Canada monetary policy decision which will be a non-event as policymakers will leave rates unchanged. You need to wait until tomorrow to get some insight into the BoC’s thinking. That’s Deputy Governor Sharon Kozicki discusses the decision before the C.D. Howe Institute at 12:35 pm ET.

Trump has slapped a 25% tariff increase (to 50%) on steel and aluminum imports to the US affecting about 6.56 million metric tons. He graciously exempted the UK from the additional 25% tariff bump due to a pending US/UK trade deal and a dinner with the King. In addition, the UK’s 49,129 tons of steel exports is too insignificant to worry about.

Canada is not taking this latest assault sitting down—well, actually we are, at least until the G-7 meeting in Kananaskis June 16-17. That’s when, as Toronto Sun columnist Brian Lilly suggests, a US/Canada tariff deal will be announced.

WTI oil prices consolidated Tuesdays gains in a 63.07-63.72 range supported by a 3.3-million-barrel decline in US crude inventories last week. Bloomberg noted that Iranian crude shipments to China fell. Alberta wildfires have disrupted about 7% of Canadian crude production with at least two oilsands plants shutdown.

ADP Employment was expected to have rebounded from 62,000 in April to 115,000 in May. It didn’t happen. Instead, ADP reported just a 37,000 increase in jobs which means the “Fed on Hold” debate just got more intense.

The US dollar retreated, and bonds bounced. The US 10-year yield dropped from 4.465 at the start of the session to 4.412%.

US ISM Services PMI index is expected to tick up to 52 from 51.6.

Chart: USDCAD daily

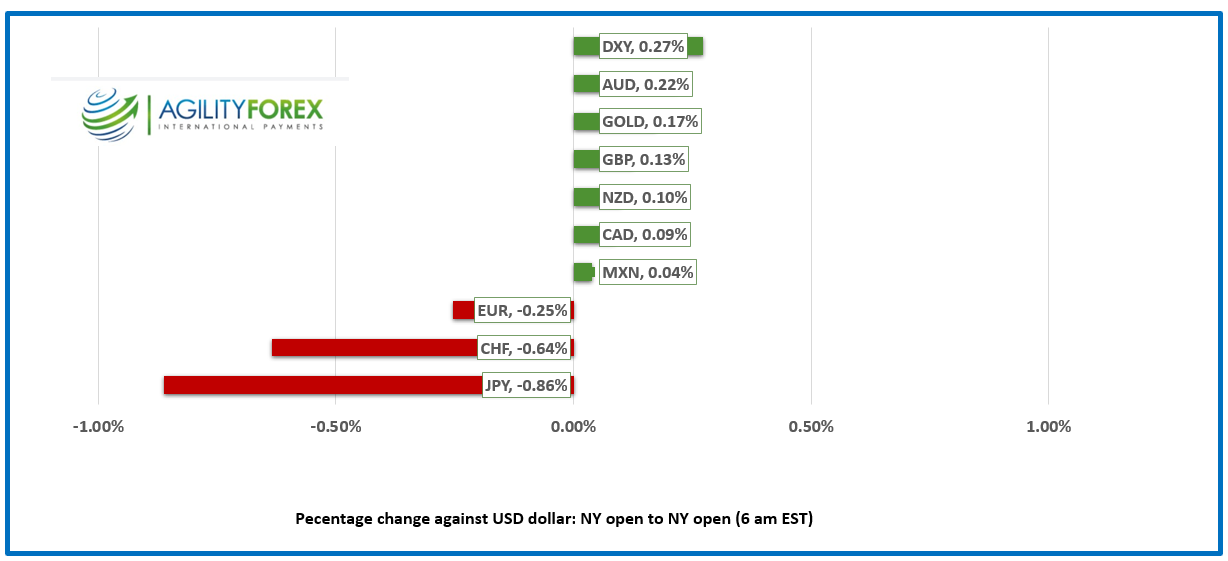

FX at a Glance

Rare Earth Ain’t Your Grampa’s Rock Band

China controls about 90% of all rare-earth metals, and Trump’s actions have disrupted the flow of these critical materials used in everything from smartphones and computers to EVs and fighter jets and a whole mess of other things. China reacted to Trump’s tariffs by imposing restrictions on exports of rare minerals. Those restrictions have caused several European auto parts and auto-making plants to close. US and Canadian car manufacturers are just as vulnerable.

That is one of the reasons why Trump is so desperate to have Xi Jinping call him, and that desperation is why he tweeted “ I like President XI of China, always have, and always will, but he is VERY TOUGH, AND EXTREMELY HARD TO MAKE A DEAL WITH!!!

Xi said, “Call you? — Maybe.” There are unconfirmed reports of a Trump/Jinping call on Friday.

Fed-speak and Data Point to Unchanged US Rates

Several Fed officials have spoken about the uncertainty around the impact of tariffs on inflation for leaving interest rates at current levels, and yesterday’s JOLTS job openings data supported the view.

The positive close on Wall Street helped to underpin Asian equity indexes, and they closed in the green. Australia’s ASX 200 led the way with a 0.89% gain while Japan’s Topix rose 0.51%. European bourses followed suit. The French CAC 40 index is up 0.64%, and the German DAX has climbed 0.58%. S&P 500 futures are up 0.16% as of 6:45 a.m. The 10-year Treasury yield is 4.454%, and gold (XAUSUD) is 3351.41.

EURUSD

NY Open: 1.1384 Overnight Range: 1.1357-1.1404

EURUSD is trading cautiously ahead of tomorrow’s ECB meeting when it is almost guaranteed to deliver a 25 bp rate cut. Services PMI data was marginal. S&P Global wrote, “The eurozone economy has grown for the fifth month in a row, but this interpretation requires a certain amount of goodwill, as the overall index of 50.2 is only marginally above the expansion threshold and the pace of growth also slowed slightly in May.”

GBPUSD

NY Open: 1.353, Overnight Range: 1.3501-1.3546

GBPUSD continues to spin its wheels, and the news that the UK was exempted from the 25% tariff increase on steel and aluminum had little impact. The UK must still pay the existing 25% tariff. UK Services PMI was a tad firmer than expected, rising to 50.9 from 50.2 in April.

USDJPY

NY Open: 142.86, Overnight Range: 143.68-144.39

USDJPY consolidated yesterday’s gains while maintaining a bullish bias. The rally was sparked by improved risk sentiment and lower odds of a Fed rate cut in the near term. The BoJ is wrestling with higher inflation, which may be exacerbated by Trump’s tariffs, which may hamper efforts to raise interest rates.

AUDUSD

NY Open: 0.6475, Overnight Range: 0.6451-0.6481

AUDUSD remained rangebound after Q1 GDP disappointed and only rose 0.2% q/q compared to the 0.4% expected and 0.6% q/q previously. Economists suggest the lack of growth was due to frugal consumers and slowing government spending.

NZDUSD

NY Open: 0.6012, Overnight Range: 0.5992-0.6017

NZDUSD traded sideways due to the lingering impact of soft Chinese data and ongoing US/China trade tensions.

USDMXN

NY Open: 19.2167, Overnight Range: 19.2015-19.2484

USDMXN remains on the defensive despite Trump’s latest insult of bumping steel and aluminum tariffs by 25% to 50% and yesterday’s firmer-than-expected JOLTS data.

China

PBoC fix: 7.1886 vs exp. 7.1977 (Prev. 7.1869).

Shanghai Shenzhen 300 rose 0.43% to 3868.74

China may announce a big Airbus order (hundreds of planes) when EU leaders visit Beijing.

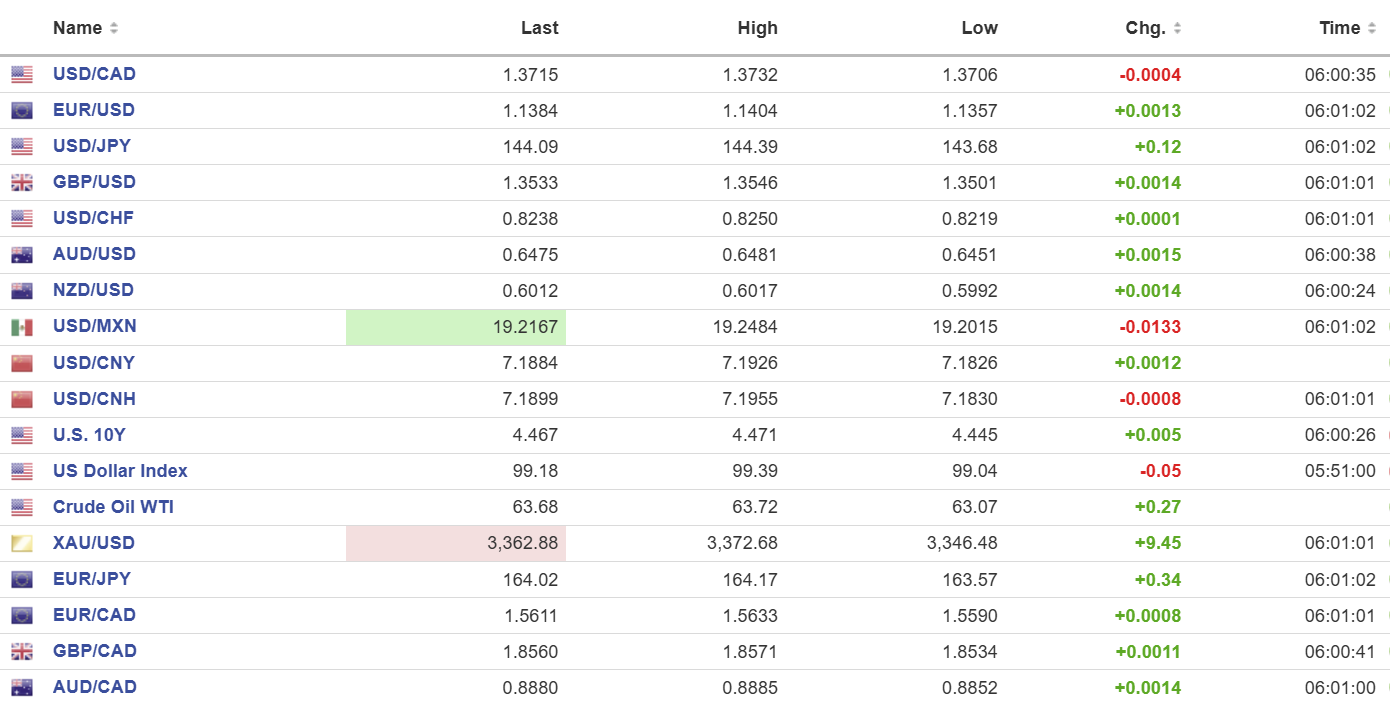

FX high, low, open (as of 6:00 am ET)

Sources: Yahoo Finance, Oanda, Investing.com, Bloomberg.