Agility Forex Daily Commentary

July 2, 2025

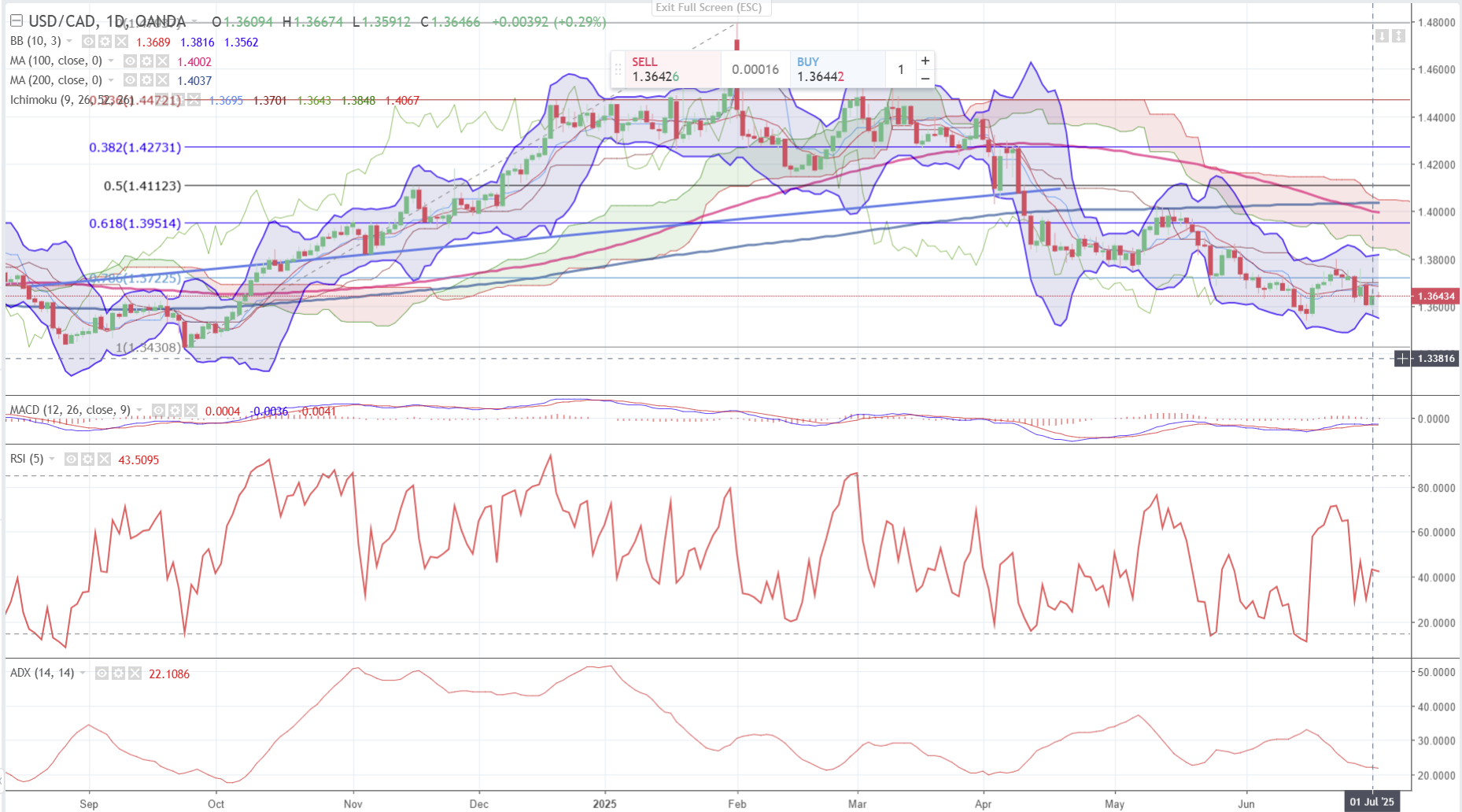

USDCAD open 1.3651, Range July1-July 2, 1.3592-1.3670, close 1.3646

USDCAD traded defensively yesterday until steady US jobs data and Fed Chair Powell’s comments about leaving rates unchanged gave the greenback a bit of a boost.

Canada and the US are negotiating a a trade framework after Prime Minister Mark Carney cancelled the Digital Services Tax (DST)aimed at US tech companies. Trump wasn’t the only one cheering the news— Canadians were just as elated. It is more than the Tech companies would have passed the entire cost of the DST onto Canadian consumers which would have also raised the GST tax on the bill.

Today’s ADP data showed that the US lost 33,000 jobs in June (forecast 95,000 vs 37,000 in May) but Challenger job cuts were far less than in May, (actual 48,000 vs May 93,8600. Market barely reacted and are on the look-out for headlines around the Big Beautiful Bill which now faces another vote in the House of Representatives.

There are no Canadian economic reports of note today.

USDCAD Technical Outlook:

The intraday technicals are bullish above 1.3590 and looking for a a break above 1.3670 to target 1.3720, then 1. 3760.. A move below 1.3590 suggests a retest of support in the 1.3540-50 zone.

Longer term, USDCAD is targeting a move to 1.3510 while prices are below 1.3700 but momentum indicators are neutral. A move above 1.3700 targets 1.3810

For today, USDCAD support is 1.3590 and 1.3550. Resistance is 1.3670 and 1.3710. Today’s Range 1.3610-1.3710

Markets in Brief

Canadians returned from Canada Day celebrations today while American’s are getting ready for their July 4th Independence Day holiday tomorrow.

President Trump continues to insult Fed Chair Jerome Powell and also threatened Japan with a tariff hype of 30-35% or more unless Japan’s caves in to his demand to import US rice.

Trump’s Beautiful Bill squeaked through the Senate, 51- 50 after VP JP Vance broke the tiebreaker. Next stop-US House of Representatives.

Stock Taking

Asian equity indexes closed on a mixed note, Hong Kong’s Hang Seng gained 0.62%, Australia’s ASX 200 rose 0.66% while Japan’s Topix fell 0.21%.

European bourses erased earlier gains and are in negative territory, except for the French CAC 40 which is up 0.82%. The German Dax is flat while the UK FTSE 100 index is down 0.27%. S&P 500 Futures gave up earlier gains and are down 0.11%.

The 10-year US Treasury yield has climbed to 4.28% after touching 4.185% yesterday. Gold (XAUUSD) is 3348.30.

EURUSD

EURUSD traded in a 1.1762-1.1829 range yesterday and opened close to the low in NY today. The downside pressure stemmed from a somewhat resilient US JOLTS report. A number of ECB policymakers, including President Christine Lagarde, said that supply shocks were a concern, but interest rates were still likely to head lower. EU officials are reportedly willing to accept a 10% basic tariff from the US if the Americans agree to cut tariffs on other sectors including cars and pharmaceuticals. Chalk another win up for Trump.

GBPUSD

GBPUSD continued to consolidate last week’s gains in a 1.3638-1.3790 range since yesterday and is trading at 1.3702 in early NY. Prices were weighed down by dovish comments from BoE Governor Andrew Bailey, who said that slowing economic growth and a weaker employment picture suggested gradually lower interest rates.

USDJPY

USDJPY hopped about inside yesterday’s 142.70-144.36 range. The bottom was seen after a better-than-expected Tankan report on Tuesday weighed on USDJPY until US data and Powell’s unchanged interest rate outlook boosted prices. Japan and US trade talks are front and center. Trump is annoyed that Japan did not bow to his demand to import US rice and said that without a deal by his July 9 deadline, Japan would be slapped with 30-35% tariffs.

AUDUSD

AUDUSD bounced inside yesterday’s 0.6554-0.6592 range. Selling pressure from weaker-than-expected S&P Global June Manufacturing PMI (actual 50.6 vs forecast 51) was offset by a higher Chinese Manufacturing PMI reading. Overnight, soft building permits and disappointing retail sales numbers left AUDUSD rangebound.

NZDUSD

NZDUSD traded sideways in a 0.6072-0.6106 range with lingering support from Tuesday’s higher-than-forecast business confidence data underpinning prices, while a rebound in the US dollar vs the majors capped gains. ASB bank economists expect that the RBNZ will leave rates unchanged at the July 9 meeting.

USDMXN

USDMXN snapped a seven-day losing streak and climbed in 18.7315-18.7687 after touching 18.6618 yesterday, a level last seen in August 2024. Yesterday’s US data and Fed Chair Powell’s “wait-and-see” attitude toward interest rate cuts supported prices.

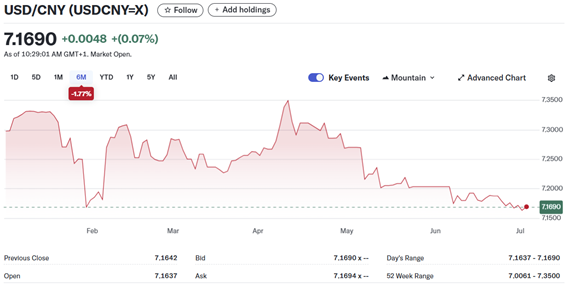

USDCNY

PBoC fix: 7.1546 vs exp. 7.1623 (Prev. 7.1534),

Tuesday PBoC fix: 7.1534 vs exp. 7.1509 (Prev. 7.1586)

Shanghai Shenzhen 300 rose 0.02% to 3943.68

Caixin June Manufacturing PMI 50.4, (Previous 48.3).

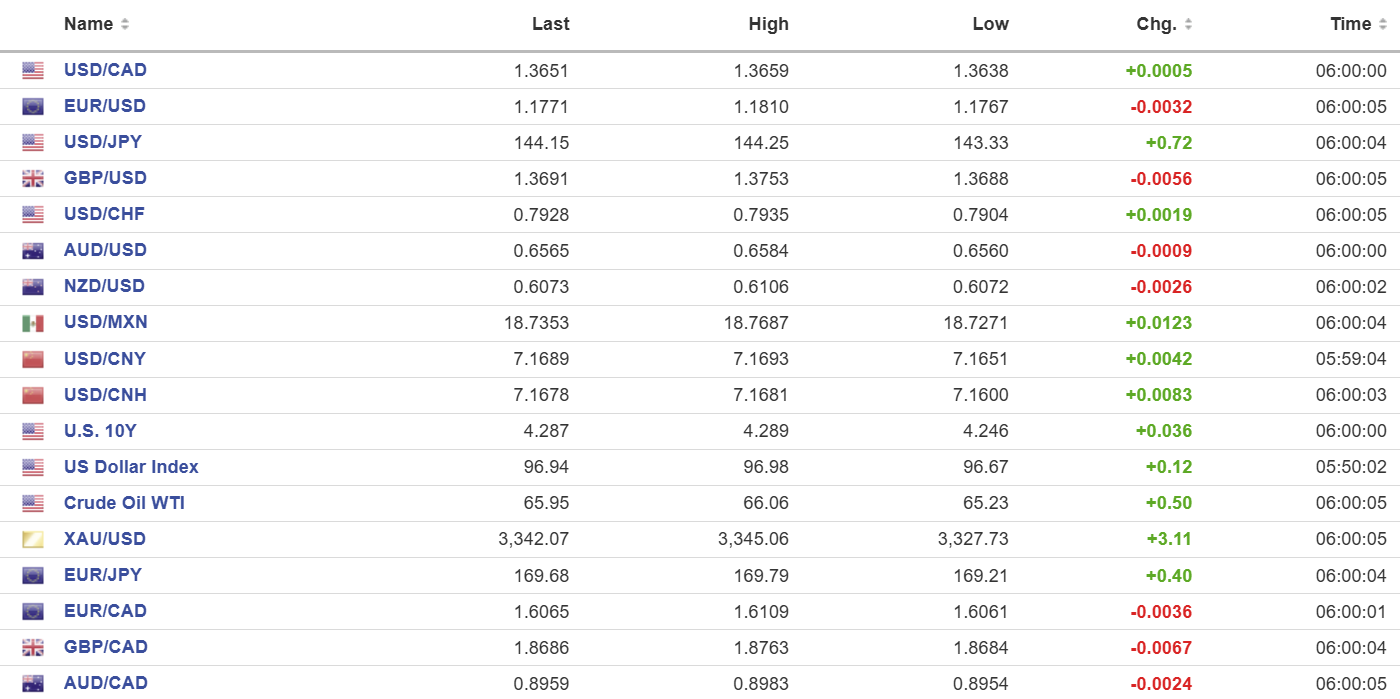

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance