July 14, 2025

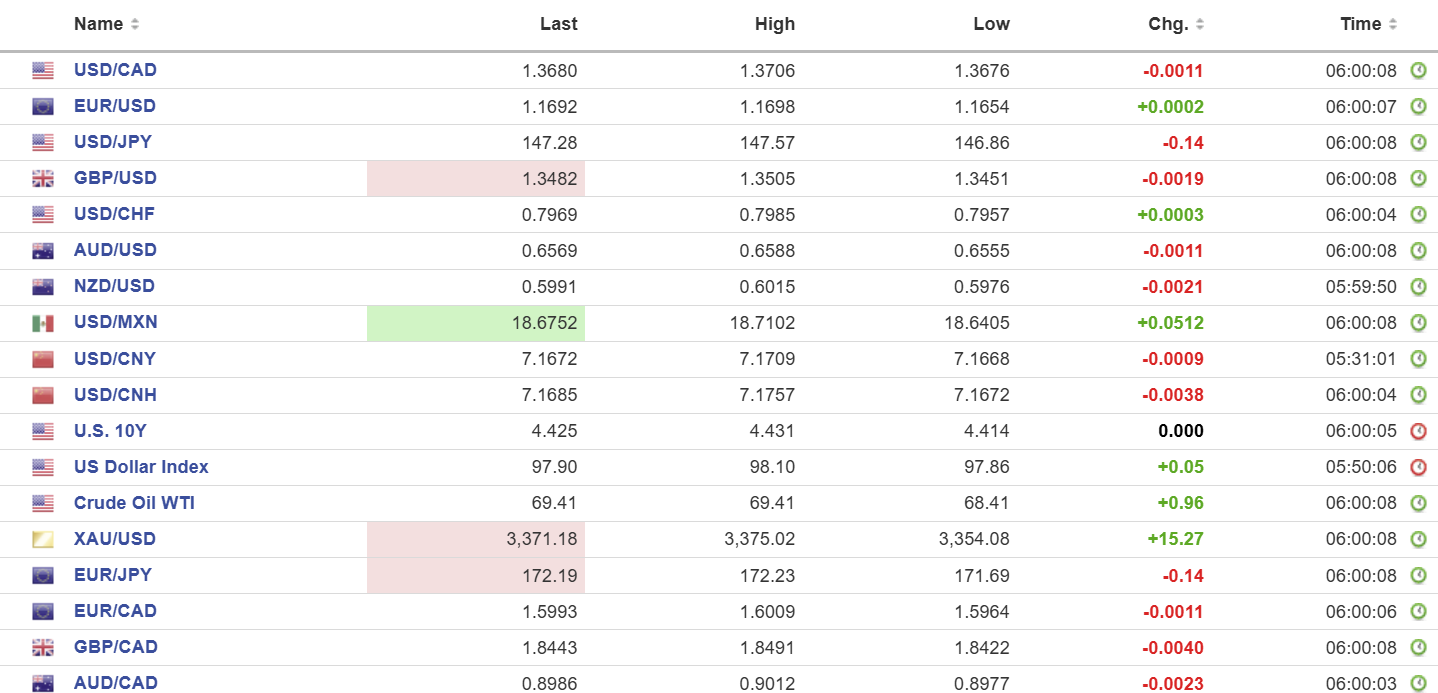

USDCAD open 1.3680 overnight range 1.3673-1.3706, close 1.3691

Another day, another Trump tariff tantrum. Trump is on a mission to rule the world via trade and is using tariffs to achieve his goal while also using them as a cudgel to beat on leaders he doesn’t like.

Canada continues to get special attention. Trump announced that tariffs on Canadian imports to the US would rise to 35% effective August 1, while other tariff letter recipients (EU and Mexico) get hit with 30% levies. Is it lingering animosity because of Trudeau? It seems to be the case as evidenced by Trump’s tweet that Rosie O’Donnell, a born and bred US native, should lose her citizenship.

Canada’s June inflation data is due tomorrow and expected to rise to 1.9% y/y from 1.7%. If so, the BoC is unlikely cutting rates on July 30.

WTI rose from 68.41 to 69.65 and is near the top in NY trading despite Opec’s production increase announcements. Oil markets supply is tighter than previously expected which is underpinning prices in the near term. News that Saudi Iranian crude shipments to China surged and China’s latest trade data support the view of increased demand.

Canada wholesale sales data is on tap while the US calendar is empty.

USDCAD Technical Outlook:

The intraday technicals are unchanged-they are bullish above 1.3650 and looking for a break above the 1.3710 are to extend gains to the 1.3750-60 zone. to extend gains to 1.3800. A move below 1.3650 targets 1.3610.

The two-week old USDCAD uptrend channel is intact while prices are between 1.3660. and 1.3760. A break below the channel bottom will extend losses to 1.3610 then 1.3560.

For today, USDCAD support is 1.3650 and 1.3620. Resistance is 1.3710 and 1.3750. Today’s Range 1.3650-1.3720

Trump Tariff Circus

Trump issued tariff letters to the EU and Mexico announcing a 30% tariff effective August 1. The letters landed in the middle of ongoing trade negotiations. The FX reaction faded rapidly as traders are becoming inured to Trump’s tantrums. Investors and traders are dealing with “tariff fatigue,” and the shock value of Trump tariff announcements has diminished greatly compared to Liberation Day, and US equity markets recently hit record highs.

Nixing Powell

Trump and his administration remain very frustrated with Fed Chair Powell’s refusal to bow to Trump’s wishes. Powell can only be fired for “cause,” and Trump and his cronies are busy inventing a cause. They think they have found it in the Fed’s $2.5 billion headquarters renovation plans. Trump whined, “Jerome Powell has been very bad for our country. We should have the lowest interest rates on Earth and we don’t. And yet he is spending $2.5 billion rebuilding the Federal Reserve building.”

Taking Stock

Asian equity indexes suffered from tariff angst and closed with small losses, except the Hong Kong Hang Seng index, which eked out a 0.26% gain. Australia’s ASX fell 0.11%, while Japan’s Topix closed flat.

European traders were spooked by Trump’s EU tariff letter, and the German DAX is down 0.83%, followed by the French CAC 40 index, which is down 0.36%. The UK FTSE is trading 0.40% higher, as Trump likes Britain. S&P 500 futures have lost 0.26%, while gold (XAUUSD) is 3358.71 after touching 3375.02 overnight, as of 5:30 am PDT

EURUSD

EURUSD traded in a 1.1654–1.1698 range overnight. The single currency recouped all of its Asian losses sparked by Trump’s announcement of 30% tariffs on imports from the EU effective August 1. The TACO trade is alive and well in Europe. The EU is seeking alternatives to US trade and hopes to team up with other victims of Trump’s tariff-letter campaign.

GBPUSD

GBPUSD traded negatively in a 1.3451–1.3505 range, but prices are off the low in early NY. Sterling is being pressured from comments by Bank of England Governor Andrew Bailey reiterating that “the path for interest rates is downward.” His comments, combined with Friday’s disappointing UK GDP data, raised the odds for a 25 bps rate cut to 4.00% in August.

USDJPY

USDJPY chopped about in a 146.86–147.57 range, with prices underpinned by the surge in the US 10-year Treasury yield from 4.318 on Thursday to 4.431% just before NY opened. Gains were slowed after Japan’s machinery orders rose 4.4%, a tad more than the 3.4% expected. However, the result was still below the 6.6% y/y result in April.

AUDUSD

AUDUSD traded in a 0.6555–0.6588 range, supported by the latest Chinese trade data, while gains were limited by broad US dollar strength on fresh risk aversion sentiment thanks to Trump’s latest tariff announcements.

NZDUSD

NZDUSD traded defensively in a 0.5976–0.6015 range due to a bout of risk aversion sentiment fueling US dollar demand after Trump inflamed global trade tensions again. RBNZ left rates on hold last week at 3.25% amid ongoing trade drama. NZ electronic card retail sales rose 0.5% m/m in June vs a drop of 0.1% in May.

USDMXN

USDMXN gapped higher, rising from Friday’s close of 18.6373 to 18.7102 in early Asia in the wake of Trump’s surprise 30% tariff announcement on goods imported to the US from Mexico. USDMXN is trading at 18.6833 in early NY after effectively filling the “gap.” Mex/US interest differentials favour the peso and are hampering USD gains. President Sheinbaum said she still expects to negotiate a better deal.

USDCNY

PBoC fix: 7.1491 vs exp. 7.1744 (Prev. 7.1475)

Shanghai Shenzhen 300 rose 0.07% to 4017.67

China’s trade surplus widened far more than expected (actual $114.77 b, forecast $109.0 b, May $103.22 b) for a gain of 5.8% y/y. Imports rose 1.1% y/y (forecast 1.3%, previous −3.4%).

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance