July 31, 2025

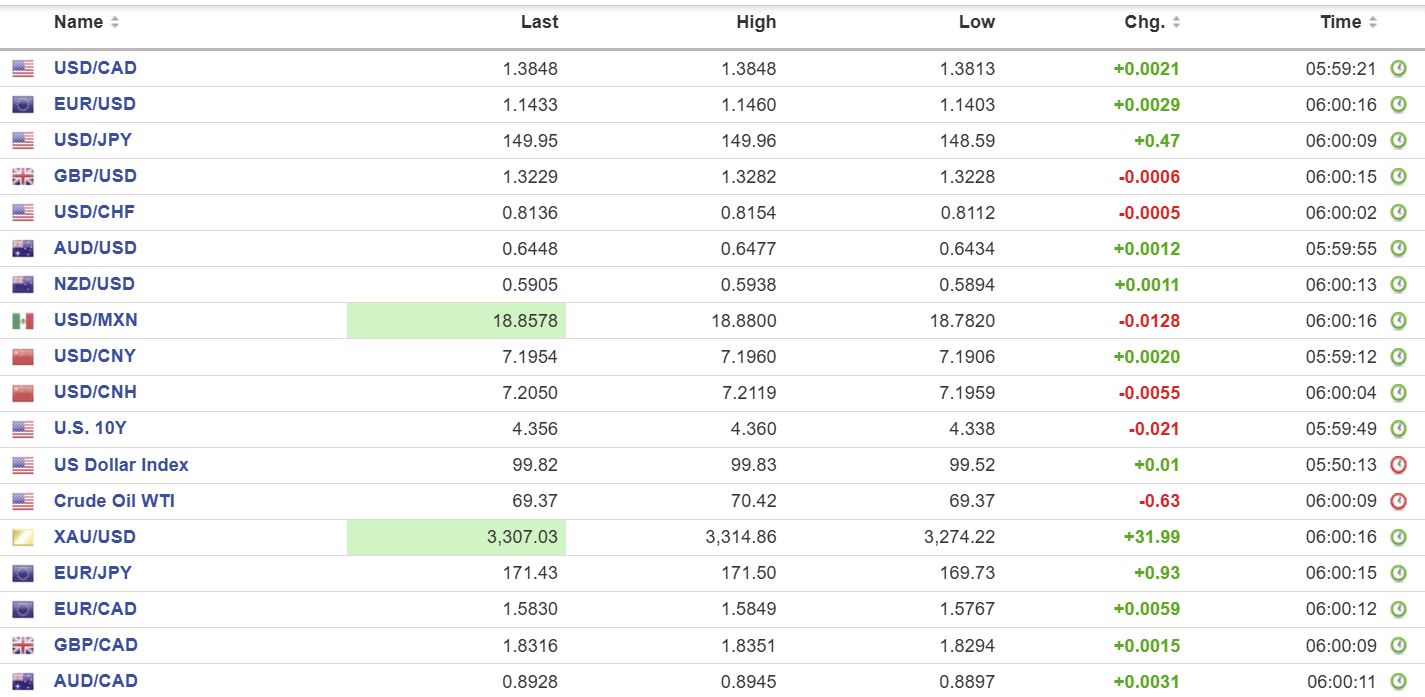

USDCAD open 1.3848, overnight range 1.3813-1.3848, close 1.3830

USDCAD is on a tear and shredding resistance levels as a timid Bank of Canada, and hawkish Fed fuel broad-based US dollar gains. The rally is being boosted due to Trump’s plans to hit Canada with 35% tariffs starting tomorrow.

That 35% tariff could rise even further after Mark Carney announced Canada would recognize Palestine as a state in September. Trump tweeted “Wow! Canada has just announced that it is backing statehood for Palestine. That will make it very hard for us to make a Trade Deal with them. Oh’ Canada!!!

The Bank of Canada took the easy road. They left rates unchanged claiming trade uncertainty clouded the outlook. They could have cut rates to give the economy a boost and consumers some relief since inflation is within targe and then hike them if inflation heats up. It’s not like they don’t have a history of reversing previous decisions.

WTI is consolidating gains in a $69.37-70.42 range support after the US increased sanctions on China’s Iranian crude imports and promised 25% tariffs on India for buying Russian oil. However, rising US crude inventories and Trumps tariffs are muddying the outlook for crude demand, which is slowing gains.

Canada May GDP contracted by 0.1%, as expected.

Weekly jobless claims rose by 1,000 to 218,000 and the Fed-favourite inflation measure, core-PCE-price index was a tad higher than expected rising 2.6% y/y compared to the forecast of 2.5% and 2.4% in May.

USDCAD Technical Outlook:

The intraday technicals are bullish. There is steep uptrend channel on the 4-hour chart with a base of 1.3800 and a top of 1.3880. A topside break targets 1.3950 while a move below 1.3800 will lead to a rest of 1.3660 support.

Longer term, uptrend momentum is building and looking to break above the 100 day moving average at 1.3863 to target the 200-day moving average at 1.4042. However the RSI suggests USDCAD is becoming overbought

For today, USDCAD support is 1.3790 and 1.3760. Resistance is 1.3870 and 1.3910. Today’s Range: 1.3790-1.3890

Trump Stirs the Pot

Trump burned through the bandwidth on his TruthSocial account yesterday and overnight with a flurry of tariff announcements. Taiwan, India, and Canada were all on the receiving end as he flattered and chastised America’s former friends.

He said South Korea would invest $300 billion in the US on assets directed by himself. The South Koreans should just write that “investment” off. Trump spent $1.1 billion to build the Trump Taj Mahal casino, which opened in 1990. One year later it was in bankruptcy, and by 2017, it was sold for $50 million.

India faced Trump’s wrath. India is being hit with a 25% tariff for supporting Russia by buying its crude.

The copper industry was singled out with a 50% tariff on copper pipes and wiring, but Trump failed to offer up much in the way of details.

Source: Trading Economic

FOMC Fuels Dollar Rally

The U.S. dollar surged overnight, fueled by a trifecta of upbeat data: 3.0% Q2 growth, solid ADP job gains, and Powell’s hawkish lean at the FOMC press conference. Powell responded to a question by saying that the U.S. economy was not behaving like monetary policy was modestly restrictive, which reduced the odds for a September rate cut.

Trump waited to today to tweet is displeasure and boy, he was really unhappy. “Jerome “Too Late” Powell has done it again!!! He is TOO LATE, and actually, TOO ANGRY, TOO STUPID, & TOO POLITICAL, to have the job of Fed Chair. He is costing our Country TRILLIONS OF DOLLARS, in addition to one of the most incompetent, or corrupt, renovations of a building(s) in the history of construction! Put another way,“Too Late” is a TOTAL LOSER, and our Country is paying the price!”

Taking Stock

Wall Street closed with losses due to the FOMC meeting, and that negative sentiment was exacerbated by tariff news, which weighed on Asian equity indices. Australia’s ASX 200 lost 0.15%, while Hong Kong’s Hang Seng plunged 1.60%. Japan’s Topix rose 0.70% after the BoJ left rates unchanged.

European bourses gave up earlier gains following todays US PCE data, The UK FTSE 100 is up 0.14% while the German DAX is down 0.12% and the French CAC-40 down 0.30% S&P 500 futures have risen 0.93% but are below their best levels as of 5:45 am PDT. The U.S. dollar index (DXY) is 98.88, and Gold (XAUUSD) is $3,310.50. The U.S. 10-year Treasury yield is 4.346%.

Meta and Microsoft Q2 earnings were higher than expected. However, tech companies will be facing additional scrutiny today after a UK regulator said Microsoft and Amazon are hurting cloud competition.

EURUSD

EURUSD traded in a 1.1403–1.1460 range and remains under pressure due to lingering resentment over the EU/U.S. trade deal and the FOMC decision to leave rates unchanged. The single currency didn’t get any support from German inflation data or the slightly improved June Eurozone unemployment rate (actual 6.2%, compared to the revised 6.2% in May).

GBPUSD

GBPUSD traded poorly and is at the bottom of its 1.3211–1.3282 range in New York. The currency pair is suffering from a combination of broad U.S. dollar strength post-FOMC and divergent Fed and Bank of England interest rate outlooks. The BoE is expected to cut rates by 25 bps to 4.00% from 4.25% on August 7.

USDJPY

USDJPY soared to 149.99 from 148.59 after the Bank of Japan left interest rates unchanged. The statement erred on the side of caution, noting trade war uncertainties and the prospect that inflation increases could stall.

AUDUSD

AUDUSD consolidated recent losses in a 0.6434–0.6477 range and remains under pressure from diverging Fed and RBA interest rate outlooks. The Fed left rates unchanged, and even a rate cut in September is debatable, while the RBA is expected to cut rates by 25 bps on August 12. Trump’s 50% tariffs on copper also weighed on sentiment. Support from better-than-expected economic data helped limit losses. Australia’s June retail sales rose 1.2% (forecast 0.4%, May 0.5%) and building permits surged 11.9% in June.

USDMXN

USDMXN extended this week’s rally, rising from 18.7820 to 18.8800 due to looming tariff risks and the somewhat hawkish FOMC bias. President Claudia Sheinbaum and Trump are talking today. She is trying to convince Trump to cancel his planned 30% tariff that goes into effect tomorrow.

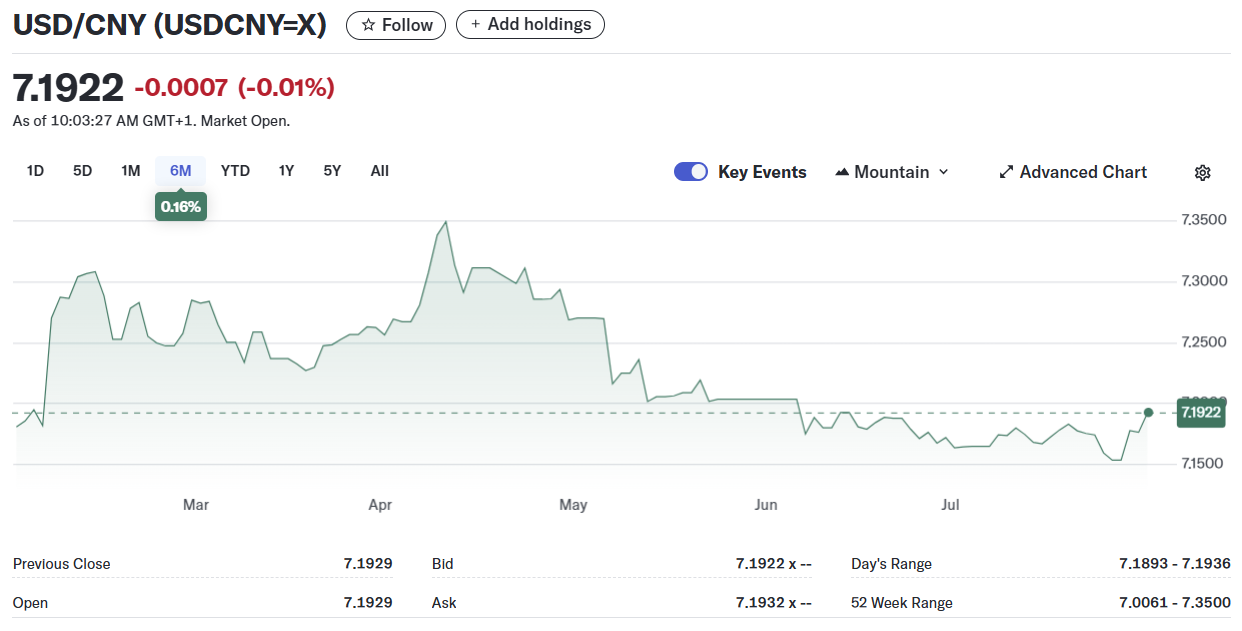

USDCNY

PBoC fix: 7.1494 vs exp. 7.2062 (Prev. 7.1441)

The Shanghai Shenzhen CSI 300 fell 1.82% to 4075.59.

The PBoC stepped in to support the yuan in the face of broad-based U.S. dollar strength against the G-10 due to the FOMC leaving rates unchanged. With tariff talks ongoing, Chinese authorities do not want a weak yuan to hamper negotiations.

China’s July Manufacturing PMI fell to 49.3 from 49.7 in June, while the Non-Manufacturing PMI dipped to 50.1 from 50.5.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics