August 18, 2025

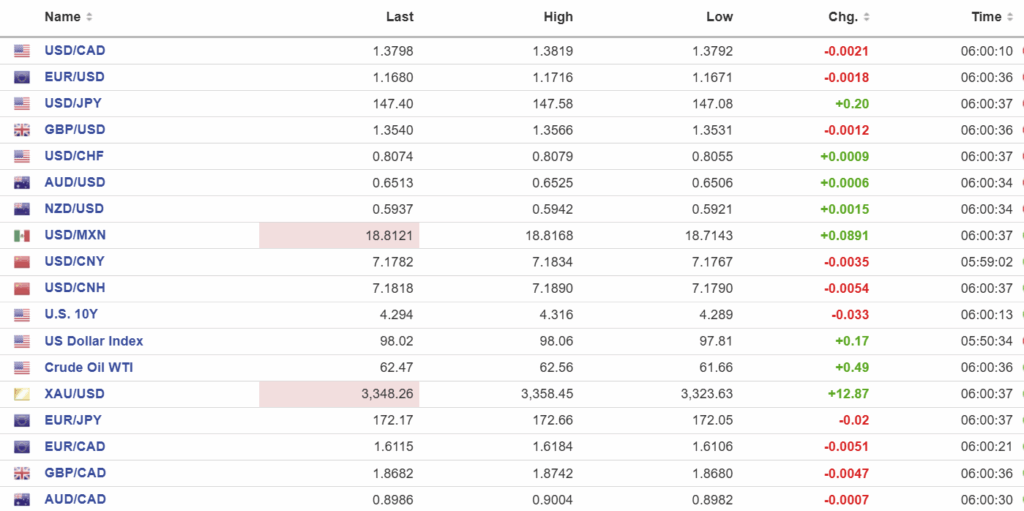

USDCAD open 1.3798, overnight range 1.3783-1.3819, close 1.3820

USDCAD drifted lower overnight in a quiet trading session and continued to do so in early NY trading due to a lack of actionable economic data and caution ahead of tomorrow’s European leaders meeting with Trump at the White House.

Canadian dollar traders are adjusting to Friday’s US economic data which collectively downgraded the odds for a Fed rate cut in September. Not by much—the CME FedWatch odds are 82.6% from around 92% last week.

Chicago IMM positioning is a big drag against USDCAD gains as those speculators are heavily short Canadian dollars (about CAD 7.92 billion, or US5.73 billion).

WTI oil prices traded in a 61.66-62.56 range as they attempt to fill the gap between Fridays close (63.12) and the Asia open today (62.18). Traders were disappointed in the lack of progress from the Trump/Putin talks.

USDCAD Technical Outlook:

The intraday technicals are bullish above 1.3750 and are looking for a decisive break above the 1.3830 to test resistance (and the August peak) A break below 1.3750 targets 1.3690.

The medium-term technical picture remains bearish while prices are below the 1.3950 area (61.8% Fibonacci retracement of September 2024 to February 2025 range). A decisive move above 1.3950 would negate the view. A move below 1.3720 targets 1.3650.

For today, USDCAD support is 1.3740 and 1.3700. Resistance is 1.3830 and 1.3880. Today’s Range: 1.3740-1.3820

Cautious Start to Busy Week.

Markets are off to a quiet start today, but the tempo will pick up as the week rolls on. Traders, especially in Europe, will be watching as leaders from the U.S., Ukraine, the EU, Germany, the U.K., France, Italy, and NATO meet to discuss Russia and Ukraine. The meeting is unlikely to deliver a breakthrough, but markets will be quick to seize on any hint of stronger Western unity—or signs of division.

On Wednesday, the release of the July 30 FOMC minutes will highlight internal divisions after two members broke ranks and sided with Trump in calling for rate cuts—both angling to position themselves as Powell’s potential successor.

Friday, Fed Chair Jerome Powell is the keynote speaker at the annual Kansas City Fed’s Jackson Hole Symposium. This year’s theme is “Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy.” Riveting, I know, but after Friday’s stronger-than-expected Control Retail Sales data, higher import prices, and a robust NY Fed Manufacturing Index, Powell should be comfortable sticking to his “unchanged for longer” interest rate policy.

Taking Stock

Asian equity markets closed higher. Japan’s Topix rose 0.43% while Australia’s ASX 200 gained 0.23%. The Hong Kong Hang Seng fell 0.37%.

As of 5:30 am PDT, European bourses are in the red. The French CAC-40 Index has fallen 0.72%, the German DAX is down 0.32% and the U.K. FTSE 100 is flat. S&P 500 futures are down 0.11% and the 10-year Treasury yield and is 4.307%. Gold (XAUUSD) is 3346.76 and the U.S. Dollar Index (DXY) sits at 98.04

EURUSD

EURUSD retreated from 1.1716 to 1.1671 overnight, partly due to the lack of any progress from the highly touted Trump/Putin meeting in Alaska but largely from the collapse in the Eurozone trade surplus (Actual €7 billion, forecast €17.58 b and previous €16.5 b). Traders are hoping that tomorrow’s EU meeting in Washington will end with positive developments toward ending Putin’s war with Ukraine. However, Powell’s end-of-the-week speech at Jackson Hole is more important for FX markets.

GBPUSD

GBPUSD traded sideways in a 1.3531-1.3566 range as it continues to consolidate gains from the beginning of the month. Analysts are convinced that the BoE has adopted a less dovish approach to rates with just 50 bps more of easing expected. That view will be tested on Wednesday with the release of July inflation (CPI forecast 3.7%, June 3.6% y/y).

USDJPY

USDJPY drifted in a 147.08-147.58 range in a quiet session. A lack of actionable data and a high degree of caution ahead of Friday’s Powell speech are containing price action. A steady 10-year Treasury yield at 4.30% is providing a bit of support.

AUDUSD

AUDUSD traded quietly in a 0.6506-0.6525 band with prices mildly supported by last Wednesday’s Australian jobs data, which served to reduce the pressure on the RBA to cut rates further.

USDMXN

USDMXN recouped Friday’s losses and rallied in a 18.07143-18.8168 range after Friday’s U.S. economic data appeared to downgrade Fed rate cut expectations. Longer term, USDMXN is in a downtrend channel from April with the top at 18.900 and the base at 18.1700, undermined by solid economic data, interest rate differentials, and the postponement of U.S. tariffs.

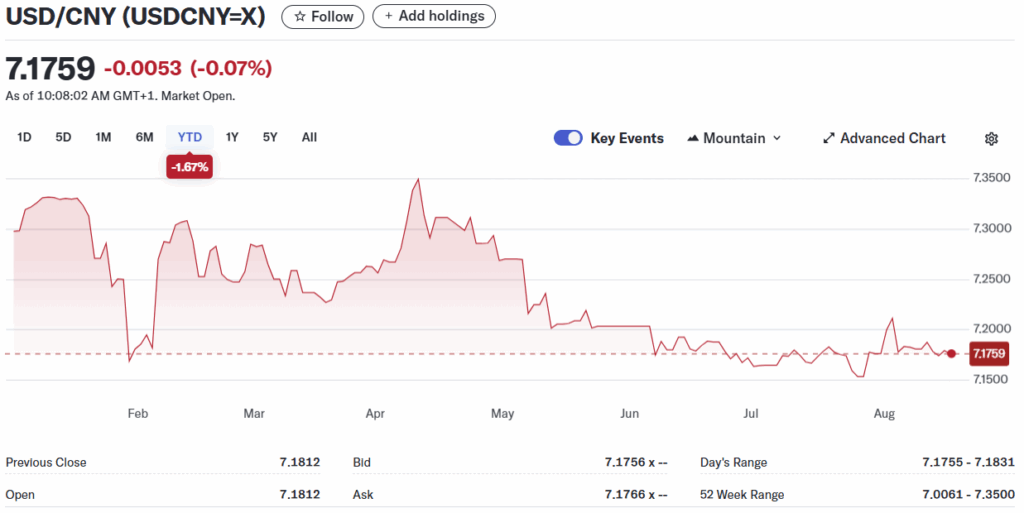

USDCNY

PBoC fix: 7.1322 vs exp. 7.1793 (Prev. 7.1371).

Shanghai Shenzhen CSI 300 rose 0.88% to 4239.41.

Trump announces delay in hiking China tariffs over Beijing’s purchases of Russian crude.

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics