August 22, 2025

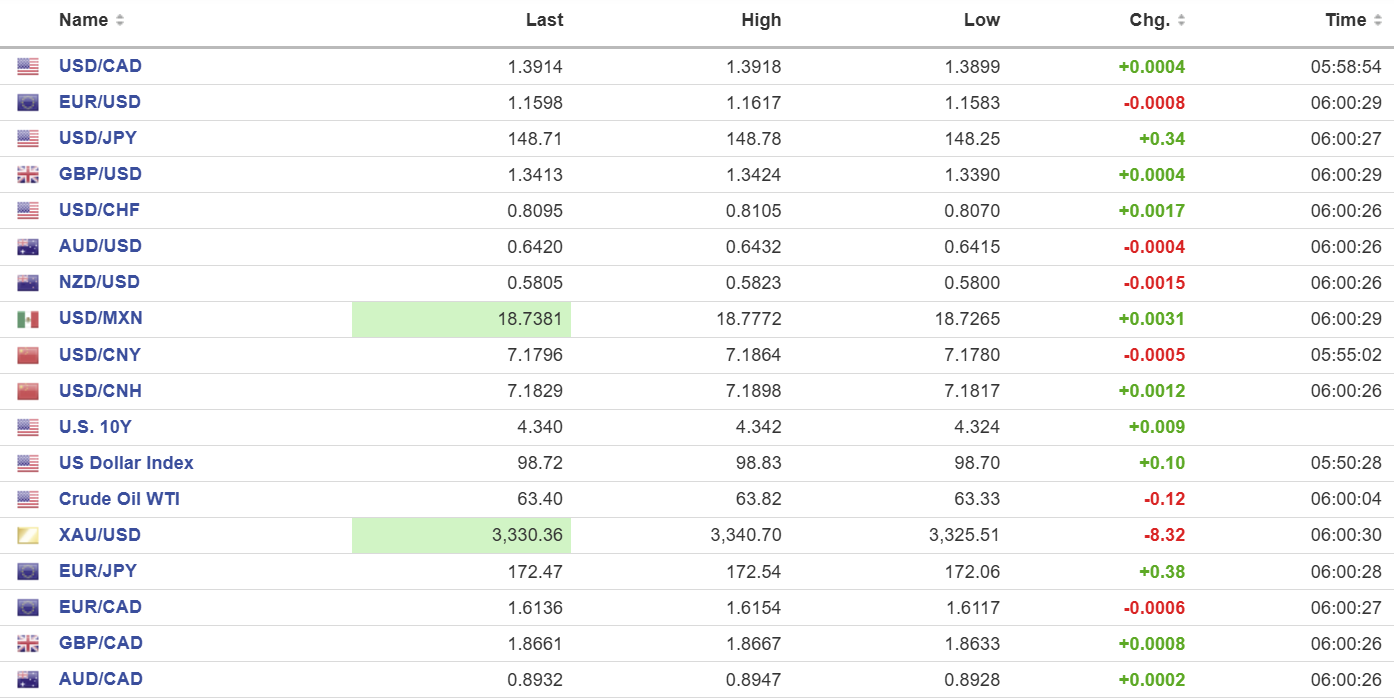

USDCAD open 1.3914, overnight range 1.3899-1.3919, close 1.3919

USDCAD rallied yesterday after traders reacted to the second-tier US S&P PMI data. In America, the ISM PMI is the more prominent report as its history dates back to 1948 and its surveys are broader and more encompassing compared to the S&P survey.

Regardless, traders did not care about such distinctions, and the stronger-than-expected S&P PMI results led to a steep downgrade in the odds for the Fed to cut rates in September. The US dollar rallied across the board, and the Loonie went along for the ride.

The Jackson Hole Symposium is in full swing today, and although Fed Chair Powell’s speech is the headliner, ECB President Christine Lagarde and BoE Governor Andrew Bailey are also delivering remarks.

WTI oil prices traded in a 63.31-63.82 range and continued to be supported by falling US inventories and the ongoing Russia/Ukraine war.

Canada Retail Sales for June rebounded, rising 1.5% m/m as expected (May -1.1%) while ex-autos surged 1.9% (forecast 1.1%, previous -0.2%). The gains are mostly payback after May’s slump from tariff-induced caution and the data was ignored.

USDCAD Technical Outlook:

The intraday technicals are bullish. USDCAD cracked resistance in the 1.3890 area yesterday but the follow through lacked conviction as the rally stalled before resistance at 1.3920. If USDCAD remains above 1.3860 the trend is toward 1.4000

The medium-term picture remains unchanged. USD/CAD is bullish above 1.3760 inside a well-defined 1.3540-1.3950 band. The break above the 100-day moving average at 1.3790 suggesting further gains toward the 200-day moving average at 1.4035.

For today, USDCAD support is 1.3860 and 1.3810. Resistance is 1.3930 and 1.3970. Today’s Range: 1.3860-1.3960

Muddying the Waters

It was only a week or so ago when CME FedWatch odds for the Fed to cut rates on September 17 were around 92%. This morning, they are 69.8%. Yesterday’s S&P Global PMI data was the catalyst for the move noting that flash US Manufacturing PMI rose to 53.3 from 49.8 in July, a 39-month high.

S&P Chief Business Economist Chris Williamson noted, “the data are consistent with the economy expanding at 2.5% this year.” He went on to say that the economic upturn fueled a surge in hiring and “allowed companies to pass tariff-related costs to the consumers.”

The kicker was this comment: “The resulting rise in selling prices for goods and services suggests that consumer price inflation will rise further above the Fed’s 2% target in the coming months.”

That sparked a rally in the US Dollar index from 98.31 to 98.3 overnight while lifting the US 10-year Treasury yield to 4.33% from 4.29%.

Fed Chair Powell’s speech from Jackson Hole is at 10:00 am.

Taking Stock

Asian equity markets were perky. Japan’s Topix recouped yesterday’s losses and rose by 0.58%. Hong Kong’s Hang Seng gained 0.93% but Australia’s ASX 200 fell 0.57%.

As of 8:50 am , the French CAC-40 Index is up 0.23%, the UK FTSE 100 is up 0.9%. and the German DAX is flat. S&P 500 futures have risen by 0.22% while the US 10-year Treasury yield is at 4.314%. Gold (XAUUSD) is 3325.93 and the US Dollar Index (DXY) is 98.68.

EURUSD

EURUSD consolidated yesterday’s losses in a 1.1583-1.1617 range due to downwardly revised German Q2 GDP (actual -0.3% q/q vs previous -0.1%), lowered odds for the Fed to cut rates in September, and a lack of progress in Russia/Ukraine ceasefire talks.

GBPUSD

GBPUSD found a bottom at 1.3390 and climbed to 1.3424 with traders content to await Powell’s speech. UK GfK Consumer Confidence was -17 compared to -19 previously. Traders were also looking ahead to a long weekend as UK markets are closed Monday.

USDJPY

USDJPY consolidated yesterday’s gains in a 148.25-148.75 range. The broad-based US dollar demand following yesterday’s S&P PMI data and the resulting rise in US Treasury yields overshadowed Japanese inflation data which came in largely as expected.

AUDUSD

AUDUSD traded sideways in a 0.6415-0.6432 range and is at its lows for this week due to greenback strength following yesterday’s US PMI data.

USDMXN

USDMXN traded in a 18.7184-18.7772 range. Then dropped t0 to 18.6803 after Mexican inflation and GDP numbers. Core inflation (0.09%) and headline inflation (-0.02%) both came in below expectations, indicating continued disinflation. Quarterly GDP rose 0.6%, improving from last quarter’s decline but slightly below forecasts, while year-on-year growth remained flat at 0%, reflecting subdued economic activity.

USDCNY

PBoC fix: 7.1321 vs exp. 7.1871 (Prev. 7.1287)

Shanghai Shenzhen CSI 300 rose 2.10% to 4378.00

China stocks surge because of ongoing rotation into equities and hopes for more government economic support in the coming days

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics