September 10, 2025

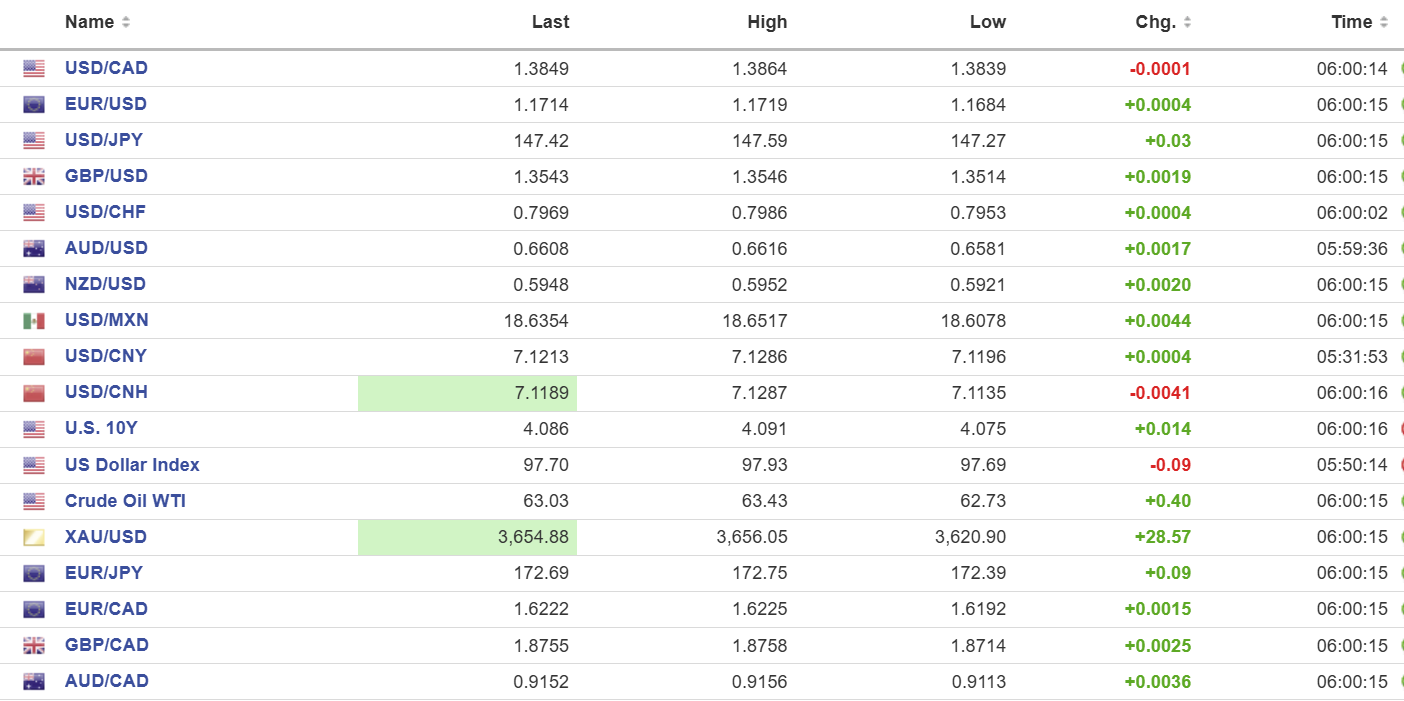

USDCAD open 1.3849, overnight range 1.3839-1.3864, close, 1.3843

USDCAD rallied from 1.3794 to 1.3860 yesterday with the rally driven by the US Bureau of Labor Statistics revisions to the nonfarm payrolls data from March 2024 to March 2025. BLS reported that America lost 911,000 jobs more than previously reported. The news followed on the heels of a very weak Canadian employment report last Friday and traders thought that if the US jobs market is weaker than thought, Canada’s may be in worse shape.

USDCAD rallied despite oil prices rising from 61.45 on Monday to 63.43 overnight after Israel bombed a Hamas sanctuary in Qatar. Oil prices are supported by concerns of supply disruptions from the Middle East because of that action.

The lack of actionable US and Canadian economic data ahead of tomorrow’s US CPI results suggests another lackluster trading session is in store.

USDCAD Technical Outlook:

The intraday technicals are bullish above 1.3820 and are looking for a break above 1.3890 to extend gains to 1.3960. A move below 1.3820 targets 1.3760 and suggests further 1.3660-1.3860 consolidation.

The medium-term picture is bullish with a symmetrical triangle formation warning that a topside break of resistance in the 1.3920-1.3950 zone would open the door to further gains to 1.4450, although good resistance would be seen at 1.4020 and 1.4150.

For today, USDCAD support is 1.3820 and 1.3780. Resistance is 1.3890 and 1.3920. Today’s Range: 1.3790-1.3890.

Inflation Cools

US Producer Prices cooled. Headline PPI fell 0.7% to 2.6% y/y compared to last month’s 3.3%y/y reading. Core PPI fell 0.9% y/y to 2.8% (forecast 3.5% y/y. Ho-hum, the Fed is focused on the labour market and today’s data will do nothing to delay the 25 bp Fed rate cut that is baked in.

Taking Stock

Asian equity indexes closed higher led by a 1.01% gain in Hong Kong’s Hang Seng. Japan’s Topix rose 0.60% and Australia’s ASX 200 climbed 0.31%.

As of 5:30 am EDT, European equities are off their best levels. The French CAC 40 is up by 0.44%, the UK FTSE 100 has climbed 0.14%, and the German DAX is flat. S&P 500 futures are ticked higher, post PPI and are up 0.30%. The US Dollar Index (DXY) has climbed to at 97.84, Gold is little changed at $3,644.63, and the US 10-year Treasury yield is 4.068%.

EURUSD

EURUSD traded cautiously in a 1.1684-1.1719 range ahead of Thursday’s ECB meeting. News that Poland shot down Russian drones that entered its airspace spooked traders in the early going but prices bounced from the low to open near the overnight peak in NY. France has a new Prime Minister, Sebastien Lecornu, whose first job was to deal with rioting “Block Everything” protestors in Paris. Obviously, Paris is no longer for lovers.

GBPUSD

GBPUSD traded uneventfully in a 1.3514-1.3546 range. Prices are supported by a generally bearish US dollar view on Fed rate cut speculation and by speculation that although the ECB will leave rates unchanged, the outlook will be dovish. In contrast, the BoE will also leave rates unchanged but issue a slightly hawkish outlook, supporting GBP.

USDJPY

USDJPY traded sideways in a 147.27-147.59 range. Falling US Treasury yields and a potential tariff deal with the US pave the way for BoJ rate hikes and are weighing on the currency pair.

AUDUSD

AUDUSD is consolidating this week’s gains in a 0.6581-0.6616 range. The prospect of a steeper and faster pace of US Fed rate cuts combined with an apparent thaw in US/China trade tensions is underpinning prices.

USDMXN

USDMXN traded in a 18.6078-18.6517 range and has found a bit of a floor after dropping from 18.8620 last week. The week-long downtrend is intact below 18.6840 and looking for a break of support at 18.5000 to target 17.6000.

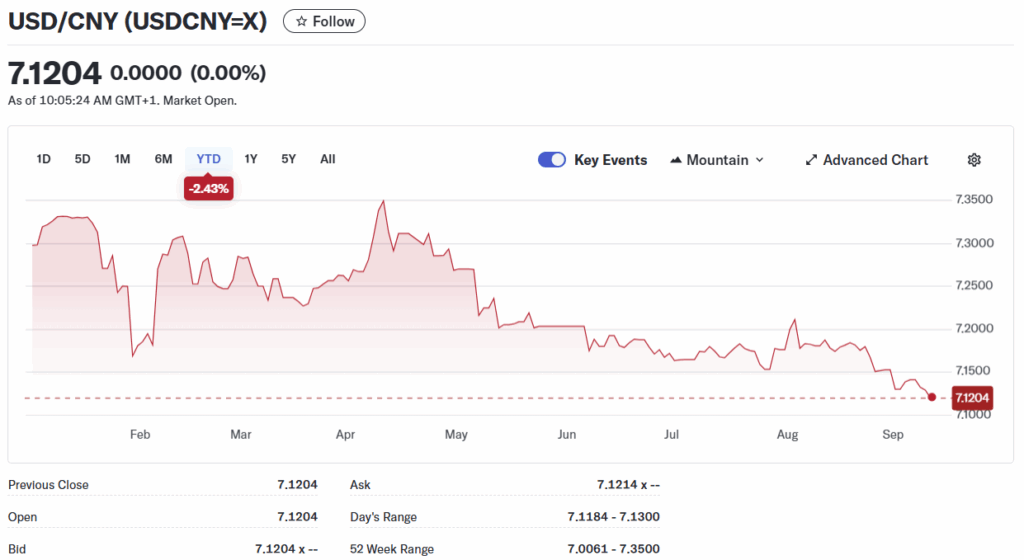

USDCNY

PBoC fix: 7.1062 vs exp. 7.1359 (Prev. 7.1008)

Shanghai Shenzhen CSI 300 rose 0.21% to 4445.36

Chinese August CPI 0.0% m/m vs 0.4% in July, and -0.4% y/y vs 0.00%.

August PPI -2.9% vs July -3.6%.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics