September 15, 2025

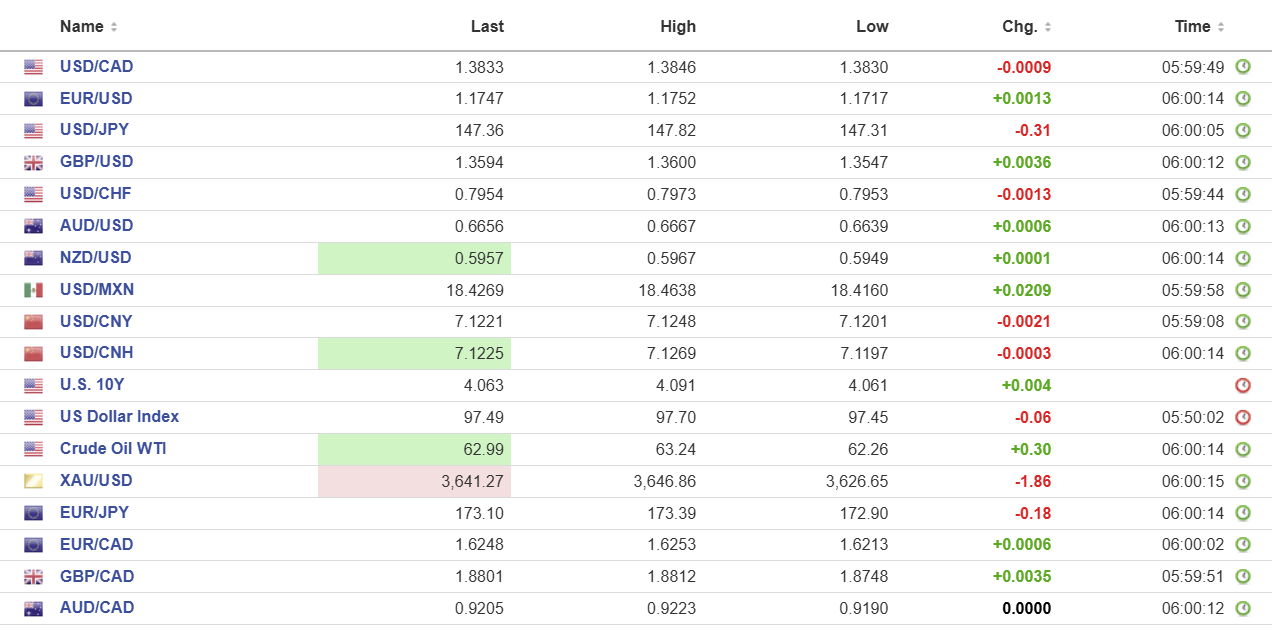

USDCAD open 1.3831 overnight range 1.3815-1.3846, close, 1.3845

USDCAD drifted lower overnight due to broad US dollar weakness and continued the trend in NY today. Traders are awaiting CPI data tomorrow and The Bank of Canada meeting Wednesday. A 25 bp rate cut is priced in following the latest weak employment report.

Politicians return to parliament after being absent since the middle of June. The government is expected to table a budget in October and Carney hinted that it would include an increase in the deficit.

Oil prices ticked higher, rising from 62.26 to 63.24 before settling in at 62.79 in NY after Trump demanded that Europe stop buying Russian crude, promising major sanctions if NATO countries follow suit. In addition, news that Ukrainian drones hit the Kirishi refinery in Russia underpinned prices.

Canada Manufacturing Sales rose 2.5% m/m in July, easily topping the 1.8% forecast. Wholesale Sales rose 1.2% m/m which missed the 1.3% target but beat the June 1.0% increase.

The New York Empire State Manufacturing Index fell 8.7 compared to the forecast of 5 and 11.9 in August.

USDCAD Technical Outlook:

The intraday technicals are bearish with the move below 1.3840 setting the stage for a test of the end of July uptrend line at 1.3780. A break above 1.3860 would shift the focus to 1.3900.

The medium-term picture is neutral with continued consolidation in a 1.3760-1.3900 range expected. A decisive break below 1.3780 would target 1.3710.

For today, USDCAD support is 1.3810 and 1.3770. Resistance is 1.3860 and 1.3890. Today’s Range: 1.3770-1.3860.

The Calm Before the Rate Cuts

It is a typical Monday morning in FX land—Trump predicting a “big cut” to interest rates this week, and headlines about China/US trade talks. In addition to the Fed meeting, the Bank of Canada, the Bank of England and the Bank of Japan monetary policy meetings are on tap. The US dollar traded defensively against the major G-10 currencies but remained inside well-defined ranges.

Taking Stock

Asian equity indexes closed with gains, except for Australia’s ASX 200 which fell by 0.13%. Japan’s Topix rose 0.40% and Hong Kong’s Hang Seng gained 0.22%.

As of 5:55 am PDT, European equities are posting gains. The French CAC 40 is up 1.27%, the German DAX has gained 0.38%, the UK FTSE 100 is flat and S&P 500 futures have gained 0.27%. The US Dollar Index (DXY) has dropped to 97.33, Gold is 3651.22 and the US 10-year Treasury yield is 4.038%.

EURUSD

EURUSD is trading at the top of its 1.1717-1.1751 range despite Fitch downgrading France to A+ from AA. The rating agency said the downgrade was because of French political instability and rising debt. The news was expected and therefore, a non-event. Traders are awaiting Wednesday’s FOMC decision.

GBPUSD

GBPUSD is trading in a 1.3547-1.3600 range at its session peak ahead of a busy week. UK employment data is due Tuesday, inflation news on Wednesday and the Bank of England monetary policy meeting Thursday. The BoE is expected to leave rates unchanged at 4.0%. No country does “pomp and pageantry” better than the UK and on Tuesday and Wednesday Trump will be feted like the Second Coming of the Messiah. King Charles and Camilla will be trotted out to schmooze with the President in hopes that the UK can remain on Trump’s good side.

USDJPY

USDJPY is at the bottom of its 147.28-147.82 range on general US dollar weakness and soft US Treasury yields. Traders are also leery ahead of the Japanese election on October 4. The BoJ is universally expected to leave rates unchanged on Friday.

AUDUSD

AUDUSD traded in a 0.6639-0.6667 range due to broad US dollar weakness. The Aussie economic calendar is empty until Thursday when employment and inflation reports are released.

USDMXN

USDMXN is under pressure and dropped from 18.4638 to 18.4121. Prices are being undermined by the modest improvement in Mexico’s inflation rate, upgraded GDP growth projections and expectations for Wednesday’s Fed rate cut to be the first of at least three more. Mexican and Chinese trade representatives are meeting over Mexico’s planned tariff hike on Chinese autos. A decisive break below 18.4100 targets 17.5000.

USDCNY

PBoC fix: 7.1056 vs exp. 7.1213 (Prev. 7.1019)

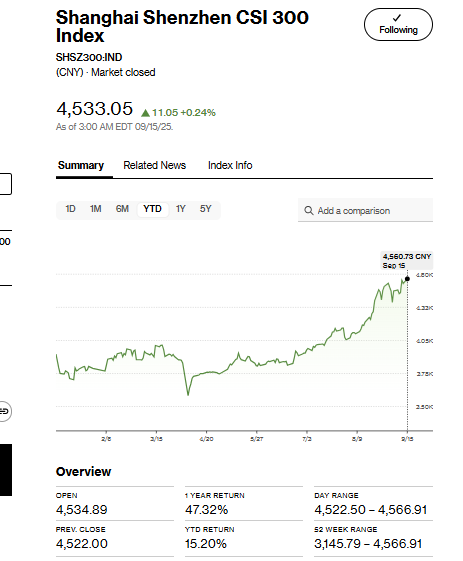

Shanghai Shenzhen CSI 300 rose 0.24% to 4533.05

China Industrial August production rose 5.2% y/y (previous 5.7%) and Retail Sales rose 3.4% (previous 3.7%).

China finds Nvidia broke anti-monopoly rules in the Mellanox Technologies deal in 2020 even as US/China trade talks are ongoing in Madrid. US Democrats sent a letter to Trump demanding that an order to reduce overproduction be part of any US/China trade deal.

China Vice Premier He Lifeng meets with US Treasury Secretary Scott Bessent in Spain next week.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics