September 16, 2025

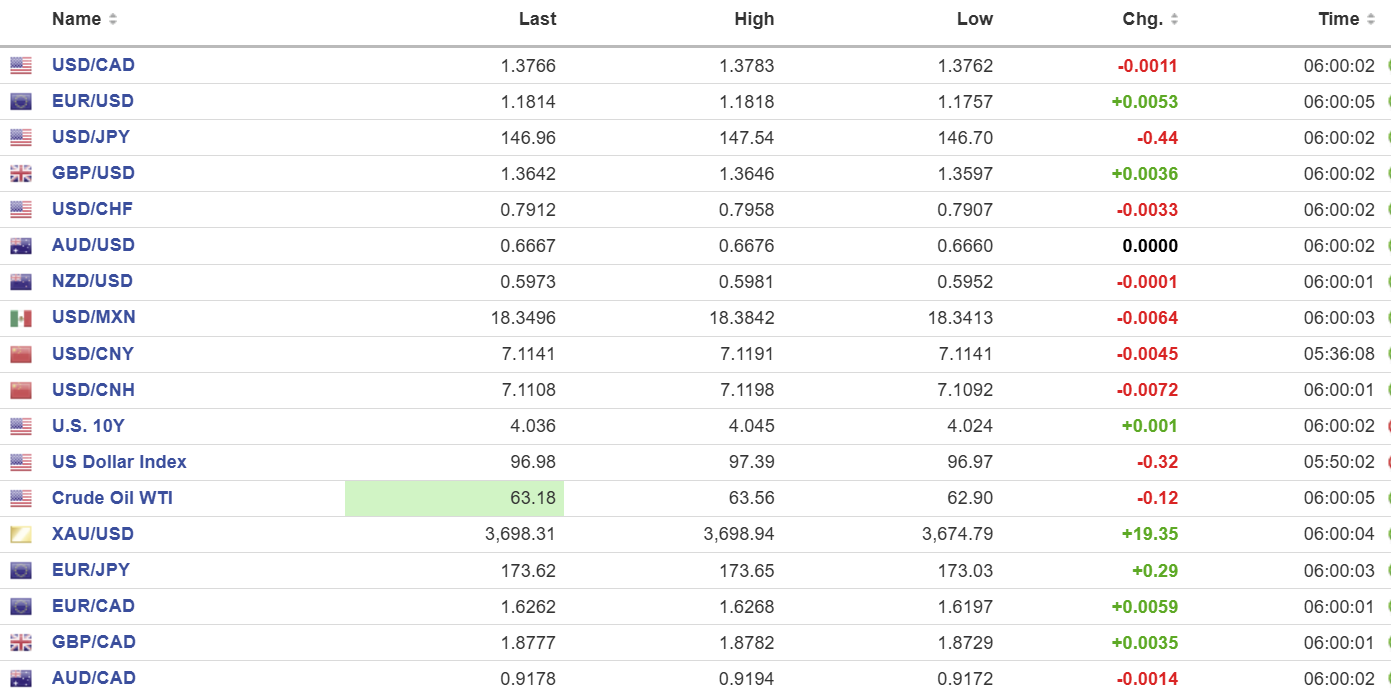

USDCAD open 1.3766 overnight range 1.3746-1.3783, close, 1.3780

USDCAD slid sharply yesterday and continued this morning in NY. The skids were greased by soft US Treasury yields and Trump loyalist, Stephen Miren’s successful confirmation as Fed Governor. He will be part of FOMC meetings starting today and that raises speculation that the Fed will embark on deeper and a faster pace of rate cuts.

Canadian inflation rose 1.9% y/y which is below the forecast for a 2.0% gain but higher than the 1.7% in July. Bank of Canada’s Core CPI measure rose 2.6% y/y, unchanged from July. The results won’t stop the BoC from cutting rates by 25 bps tomorrow, but they may encourage a more hawkish outlook from policymakers.

WTI oil prices are in the middle of the overnight 62.90-63.56 range with gains capped by the soft US dollar. However, prices are underpinned by ongoing concerns of Russian supply disruptions from Ukrainian drones attacking Russian oil infrastructure and concerns of additional US and European sanctions

USDCAD Technical Outlook:

The intraday technicals are bearish, confirmed by yesterday’s move below the end of July uptrend line at 1.3780 and targeting support at 1.3720. A decisive break of 1.3720 sets the stage for a steeper decline to 1.3570.

The medium-term technicals suggest that USDCAD is consolidating between 1.3600 and 1.4000 albeit with a bearish bias now. A break below 1.3600 sets the stage for losses to 1.3300 while a move above 1.4000 puts 14400 in play.

For today, USDCAD support is 1.3740 and 1.3710. Resistance is 1.3790 and 1.3830. Today’s Range: 1.3720-1.3820

Winners and Losers.

President Trump got a win. Stephen Miran, the Chair of the Council of Economic Advisors for Trump, who took a leave of absence from that job, is now a temporary Fed Governor. He won the Senate confirmation in a landslide 48-47 vote.

Trump was also a loser. Fed Governor Lisa Cook remains a Fed Governor, despite Trump sending her a letter to tell her she was fired for mortgage fraud. Yesterday, a Federal appeals court upheld the lower court ruling that Cook’s transgressions (if proven) were not sufficient grounds for removal.

That sets the stage for a lively FOMC debate with at least one voter wanting a 50, or even 100 basis point rate cut, while others vote to leave rates unchanged.

US Data Won’t Derail Rate Cut

Americans are undeterred by tariffs and continue to shop. US Retail Sales rose 0.6% m/m in August, the same as the upwardly revised July result. The key Retail Sales Control Group reading was 0.7% m/m in August compared to 0.4% in July. The results barely caused a ripple in FX or equity markets.

Taking Stock

Asian equity indexes closed on a mixed note. Japan’s Topix and Australia’s ASX 200 rose 0.25% and 0.28% respectively while the Hong Kong Hang Seng closed flat.

As of 8:40 am EDT, European equities are playing defense. The German DAX is down 0.68%, the UK FTSE 100 has lost 0.31% while the French CAC 40 is down 0.11%. S&P 500 futures have ticked 0.12% higher but off its best level.. The US Dollar Index (DXY) is 97.11, Gold is 3688.19, and the US 10-year Treasury yield sits at 4.059%.

EURUSD

EURUSD has caught a bid and is at the top of its 1.1757-1.1822 overnight range in early NY. The gains were fueled by weak NY Empire State data yesterday, news of Trump lackey Stephen Miran being confirmed as Fed Governor, raising speculation of an accelerated pace to Fed rate cuts in the coming months. Traders are ignoring French political dysfunction and a deteriorating German economic situation as per the latest ZEW Index. The EURUSD uptrend from August 1 is intact while prices are above 1.1680.

GBPUSD

GBPUSD mirrored EURUSD moves and rallied to 1.3650 from 1.3597. Prices are underpinned for the same reasons as the Euro but got an added boost from the UK employment report which showed that the jobs market was cooling, but not fast enough to prompt a rate cut this week. The short-term GBPUSD technicals are bullish above 1.3560 and looking for a break above 1.3680 to target 1.3900.

USDJPY

USDJPY continued to fall and traded in a 146.70-145.54 range overnight on the back of Fed and BoJ interest rate divergence. The Japanese election will keep the BoJ on hold at Friday’s meeting while the Fed is universally expected to cut rates by 25 bps tomorrow. Today is also the day that lower US tariffs on Japanese goods, including cars, begin.

AUDUSD

AUDUSD drifted higher in a 0.6660-0.6676 range supported by broad US dollar weakness and falling Treasury yields. RBA Assistant Governor Sarah Hunter said the risks to the domestic economic outlook were balanced, suggesting interest rates will be left unchanged at the September 30 policy meeting.

USDMXN

USDMXN continued to slide in a 18.3256-18.3842 range, on the back of general US dollar weakness ahead of tomorrow’s FOMC announcement. Mexican markets are closed today for Independence Day.

USDCNY

PBoC fix: 7.1027 vs exp. 7.1159 (Prev. 7.1056)

Shanghai Shenzhen CSI 300 fell 0.21% to 4523.24.

Trump and Xi are supposedly planning to chat Friday. China moves into top 10 of World’s Most Innovative Nations—Germany out.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics