October 15, 2025

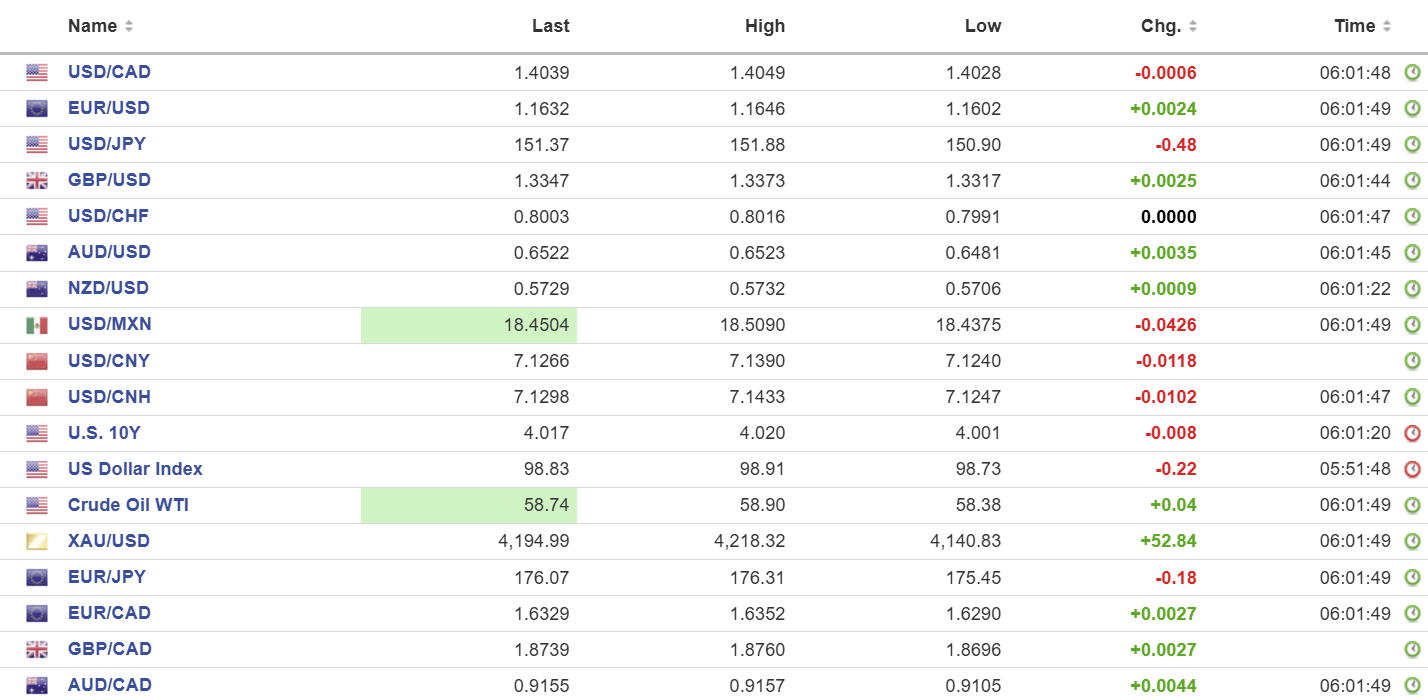

USDCAD open: 1.4039, overnight range 1.4028-1.4049, close, 1.4047

US tariffs took another toll on Canada. Stellantis (formerly Chrysler) announced it would shift Jeep Compass manufacturing from Brampton to Illinois which could mean that the 3000 employees on layoff since 2023 are not every going back to work.

WTI oil traded in a 58.38-58.90 range before climbing to 59.23 in NY trading. The weakness in prices is due to the International Energy Agency forecasting an oil surplus of about 4.0 million bpd in 2026. The escalating US/China trade tensions have exacerbated the situation.

Canada Manufacturing sales fell 1.0% in August which was a tad better than the -1.5% expected but still far worse than the 2.3% gain in July. Wholesale Sales fell 1.2% m/ compared to a gain of 1.2% in July.

USDCAD Technical Outlook

The intraday technicals are bullish above 1.3970 but looking over-extended suggesting that resistance at 1.4110 will contains gains today.

The medium-term technicals show a firm uptrend, supported by a well-defined ascending staircase pattern on the 4-hour chart. The trend is supported by prices remaining above the 200-day moving average (1.3970) and by the rising trendline near 1.3980. For today, USDCAD support is at 1.4010 and 1.3970. Resistance is at 1.4070 and 1.4110.

Today’s Range: 1.3980-1.4070

The Ball is in Jay’s Court

Yesterday, Fed Chair Jerome Powell snatched control of global financial markets that have been gripped in chaos since Friday. Escalating China/U.S. trade tensions, political dysfunction in France and the U.S. amidst fears of a stock market bubble were pushed to the back burner when Mr. Powell put rate cuts into the spotlight. He told delegates to the National Association for Business Economics, “You’re at a place where further declines in job openings might very well show up in unemployment.” That sentence convinced analysts and traders that a rate cut was a done deal on October 29. Risk sentiment turned positive, the U.S. dollar retreated, and stocks rallied. Except, the odds of a 25 bp rate cut were already around 94%, so nothing really changed.

Taking Stock

Asian equity markets jumped on the positive shift in risk sentiment following Powell’s comments about possible rate cuts. Japan’s Topix rallied 1.58%, Australia’s ASX 200 gained 1.03%, and Hong Kong’s Hang Seng rose 1.84%.

As of 5:30 AM PDT, European indexes are higher except for the UK FTSE 100, which is down 0.31%. The French CAC-40 has surged 2.37%, and Germany’s DAX has risen 0.10%. S&P 500 futures are up by 0.74%, and the U.S. Dollar Index (DXY) is 98.88. The U.S. 10-year Treasury yield is 4.018%, while gold (XAUUSD) trades at 4187.38 after reaching 4218.32 overnight.

EURUSD

EURUSD rallied from 1.1602 to 1.1646, snapping a 10-day losing streak. The single currency got a lift from political developments in France after Prime Minister Sebastien Lecornu delayed pension reform until after the 2027 election, earning Socialist Party support and improving his chances of surviving a non-confidence vote expected Thursday. Eurozone Industrial Production fell 1.2% m/m in August, better than forecast (-1.6%) but down from July’s 0.3% gain.

GBPUSD

GBPUSD traded higher in a 1.3317-1.3373 range as traders looked past soft UK job data and focused on prospects of lower Fed rates. An IMF report projecting that the UK will have the slowest improvement in living standards among G-7 economies had no noticeable impact on the currency.

USDJPY

USDJPY traded in a 150.90-151.88 band, clawing back some of yesterday’s losses amid general U.S. dollar weakness. Gains were capped by the prospect of lower U.S. rates, which kept buyers cautious near the 152.00 level.

AUDUSD

AUDUSD traded higher in a 0.6481-0.6523 range as traders shrugged off renewed China/U.S. trade tension concerns, focusing instead on Powell’s dovish tone. Markets are looking ahead to Australia’s employment data due tomorrow for fresh direction.

USDMXN

USDMXN erased Tuesday’s gains, falling within an 18.4376-18.5090 band as traders priced in the likelihood of lower U.S. interest rates, which diminished the dollar’s yield appeal.

China

PBoC fix: 7.0995 vs (forecast 7.1281 and Prev. 7.1021)

Shanghai Shenzhen: CSI 300 rose 1.48% to 4606.29

September CPI fell 0.3% y/y (forecast -0.1%, previous 0%).

September PPI fell 0 .3% y/y (forecast -2.3%, previous -2.7% y/y)

PBoC allows yuan to fix below 7.10, which is the highest level in about a year which analysts say is a deliberate move to convey strength to the world ahead of trade negotiations.

China’s Communist Party holds its annual Plenum from October 20-25. Officials are expected to prioritize boosting household consumption while curbing supply side imbalances.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics