October 30, 2025

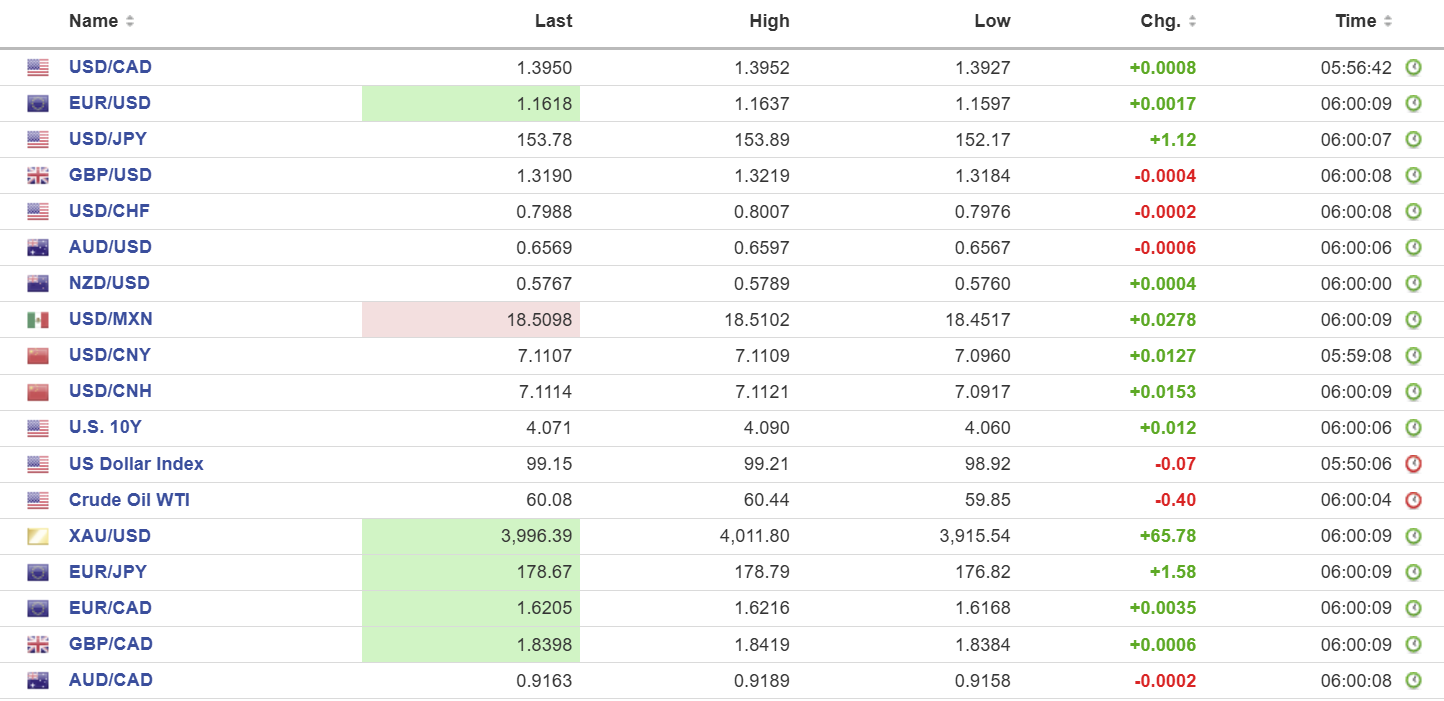

USDCAD open: 1.3950, overnight range 1.3927-1.3985, close, 1.3942

USDCAD had a lively session yesterday, sliding to 1.3888 following the BoC rate decision then rebounding after the FOMC meeting.

Yesterday, the Bank of Canada’s delivered a hawkish rate cut and lowered its benchmark rate to 2.25%. The move was expected but the statement appeared to slam the door on further easing. It said “If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment.” Essentially, the BoC is telling the Federal government “We’ve done our bit; the rest is up to you.”

The USDCAD slide lasted until the FOMC statement. The Fed trimmed its benchmark rate but Fed Chair Jerome Powell warned “future rate cuts are far from certain.” That set the tone for the US dollar for the rest of the day and overnight.

The US dollar index spiked higher and USDCAD rallied partly because of traders unwinding short dollar positions established in anticipation of the Fed cutting its benchmark to 3.0% by early next year. After Powell’s comments that outcome looks unlikely.

WTI oil traded in a 59.85-60.84 range overnight, almost identical to Wednesday’s overnight band. Prices were underpinned after the Energy information Agency EIA) reported that crude stocks fell by 6.85 million barrels last week.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish. Prices appear to have carved out a base in the 1.3890 area and today’s decisive break above the 1.3960 resistance area, sets the stage for further gains to 1.4030.

The medium-term technicals are bullish after the test of support at 1.3880 failed. The subsequent rally above the 200 day moving average at 1.3951 and through 1.3960 resistance, sets the stage for a retest of the 1.4050 area.

For today, USDCAD support is at 1.3940 and 1.3910. Resistance is at 1.4010 and 1.4050

Today’s Range: 1.3940-1.4020

Trump and Xi Make Nice

The Donald and Xi are back being besties after what Trump described as “an amazing meeting.” He said, “Overall, I guess on the scale of from zero to 10, with 10 being the best, I would say the meeting was a 12.” In turn, Mr. Jinping described the two countries as “partners and friends,” then gushingly said to Trump, “China’s development goes hand in hand with your vision to make America great again.” The result was that Trump cut the tariffs levied on China for fentanyl production to 10 % from 20 % and Xi hit the pause button on export curbs of rare earth minerals.

FOMC Decidedly Undecided

The FOMC surprised no one when they cut the overnight rate to 4.0 % and announced an end to quantitative tightening. Governor Stephen Miran voted for a 50 bp rate cut while Kansas City Fed President Jeffrey Schmid wanted to leave rates unchanged.

In his press conference, Fed Chair Powell suggested that a follow-up move in December is not a done deal, saying, “A further reduction in the policy rate at the December meeting is not a foregone conclusion—far from it.”

The news sent Treasury yields and the US Dollar Index soaring.

Taking Stock

Asian equity indexes closed with Japan’s Topix gaining 0.69 %, Hong Kong’s Hang Seng dropping 0.24 %, and Australia’s ASX 200 falling by 0.48 %.

As of 6:45 AM, European indexes are negative. The UK FTSE 100 index is down by 0.46 %, the German DAX has lost 0.17 %, and the French CAC-40 index is off by 0.66 %. S&P 500 futures are down by 0.16 %, and the U.S. Dollar Index (DXY) is 99.23. The U.S. 10-year Treasury yield is 4.08 %, and Gold (XAUUSD) is 3986.40.

EURUSD

EURUSD dropped in the wake of the hawkish Fed rate cut, then traded with a negative bias in a 1.1576-1.1637 band. Today’s ECB meeting (no rate cut expected) has been overshadowed by Powell’s comments suggesting that a December rate cut is not a foregone conclusion. German inflation and GDP results were close to expectations, while Eurozone Economic Sentiment rose to 96.8 from 95.6. The data has been a non-factor for traders.

GBPUSD

GBPUSD is at the bottom of its 1.3159–1.3219 range, with traders still concerned around the upcoming UK budget and the Bank of England meeting. The BoE is widely expected to leave rates unchanged at 4.0 % due to the November 20 Autumn budget, but some banks, like Goldman Sachs, are pencilling in a 25 bp rate cut.

USDJPY

USDJPY traded with a bid and is at the top of its 152.17–154.28 overnight range in early NY. The surprisingly hawkish Fed and the BoJ’s “no change” decision combined to fuel demand. The BoJ’s decision was not much of a surprise because policymakers are trying to make sense of the new tariff regime and the state of the U.S. economy. As usual, they are awaiting “more data.” The surge in the U.S. 10-year Treasury yield from a low of 3.975 % yesterday to 4.11% is underpinning gains.

AUDUSD

AUDUSD traded in a 0.6546–0.6597 range, little changed from yesterday’s band despite the thawing of U.S. and China trade tensions. That’s because of broad U.S. dollar demand by traders unwinding short-dollar bets after the odds for a Fed December rate cut dropped sharply.

USDMXN

USDMXN rallied from 18.451 to 18.5487 supported by weak Mexican Q 3 GDP numbers (actual -0.3% q/q, (forecast -0.3%, previous 0.6%) and the hawkish Fed rate cut.

China

PBoC Fix: 7.0864 vs exp. 7.1056 (Prev. 7.0843)

Shanghai Shenzhen: CSI 300 fell 0.80% to 4709.91

China suspends rare earth curbs for one year and that the US will halt the rule targeting subsidiaries of blacklisted firms. China and the US have agreed to a one-year suspension of reciprocal port fees.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics