November 4, 2025

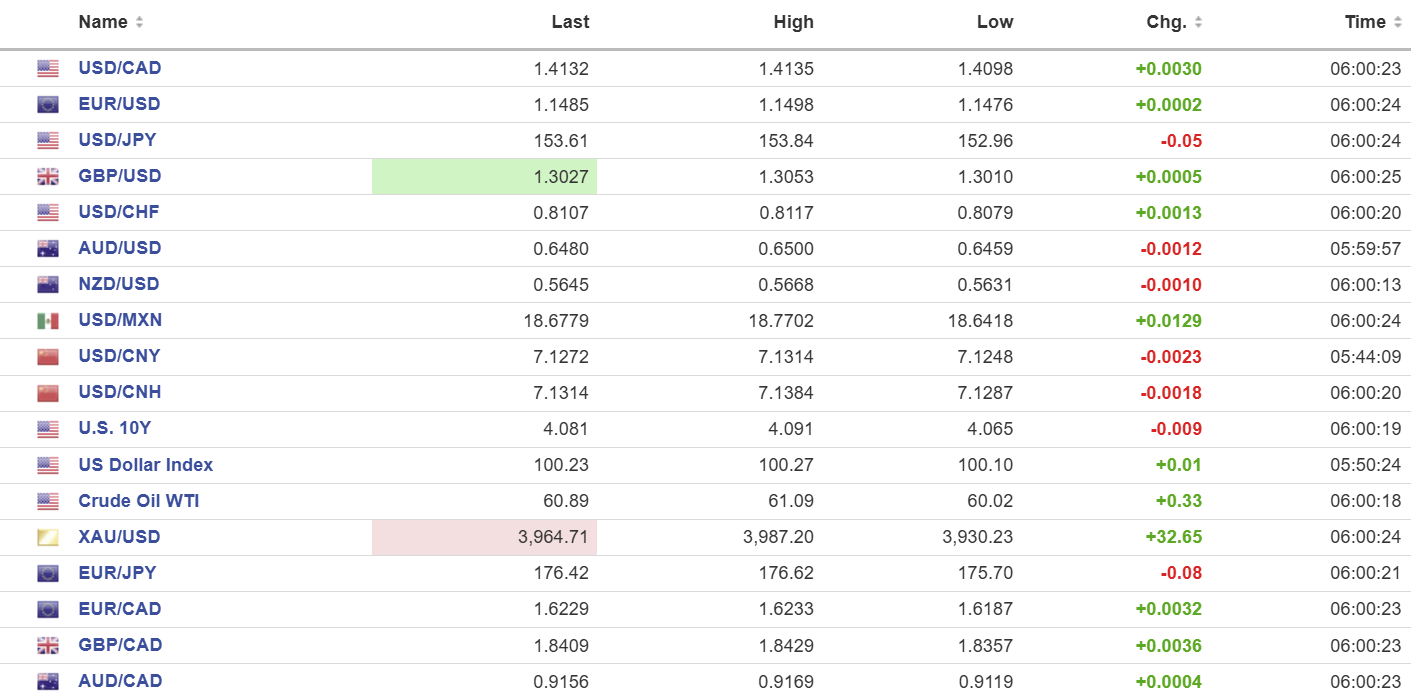

USDCAD open: 1.4132, overnight range 1.4098-1.4139, close, 1.4104

The Canadian dollar is a lot weaker than it was on Halloween due to last week’s hawkish comments from Fed Chair Powell which forced the market to recalibrate its US interest rate outlook. In addition, the thaw in trade tensions between the US and China combined with the ongoing US government shutdown and the ongoing tech stock correction are fueling broad US dollar demand.

The Federal government tabled a budget (Our Plan: Building Strong). It’s a plan for $178 billion in new spending over 5 years, offset by savings of around $56 billion from a “Comprehensive Expenditure Review.” The deficit which last budget was projected to be less than $42 billion, will balloon to $78 billion.

The budget also maintains Canada’s extremely-flawed climate objectives with its industrial carbon-pricing system in place which is an indirect carbon-tax hike on consumers.

WTI oil prices track steadily higher in a 60.02-61.09 range, underpinned by higher than expected US crude inventories. The American Petroleum Institute reported crude inventories rose by 6.5 million barrels in the week ending October 31.

Bank of Canada Governor Tiff Macklem and Deputy Governor Carolyn rogers testify before the House of Commons Standing Committee on Finance today then repeat the performance to the Senate tomorrow.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish while trading above 1.4110 and looking for a break above the 1.4170-1.4195 area to target 1.4270. However, momentum and volatility indicators are screaming “over-bought.” A break below 1.4110 suggests further weakness to 1.4010.

The medium-term technicals are bullish with USDCAD comfortably above the major moving averages and underpinned by key support in the 1.3960 area.

For today, USDCAD support is at 1.4110 and 1.4060. Resistance is at 1.4170 and 1.4110.

Today’s Range: 1.4070-1.4170

Tech Stock Correction:

The US dollar is rallying across the board on the back of a sharp tech stock correction. Stock market sweetheart Nvidia (NVDA: Nasdaq) has lost 5.3% since posting a record high of $212.19 on October 28. Tesla (TSLA: Nasdaq) is down 6.2% this week and Amazon lost 1.84% yesterday. Coincidentally, the sell-off occurred following “correction” warnings from the CEOs of JPMorgan Chase, Morgan Stanley, and Goldman Sachs.

Tariffs on Trial

The US Supreme Court is hearing arguments against Trump’s tariffs today to determine if the president has the authority to impose tariffs under emergency powers. Yesterday, Trump tweeted, “Tomorrow’s United States Supreme Court case is, literally, LIFE OR DEATH for our Country.”

Employment in the Spotlight

US ADP data barely caused a ripple in FX markets despite showing a gain of 42,000 jobs in October, easily beating the 25,000 expected. The report noted that although jobs rebounded from tow months of weak hiring, the gains were not broad-based.

Taking Stock

Asian equity indexes closed with losses. Japan’s TOPIX lost 1.19%, Hong Kong’s Hang Seng was flat, and Australia’s ASX 200 dropped 0.13%.

As of 5:30 am PT, the German DAX is down 0.33%, the French CAC-40 index is flat, and the UK FTSE 100 index is up 0.15%. S&P 500 futures are down by 0.11%, and the US Dollar Index (DXY) is 100.19. The US 10-year Treasury yield is 4.104%, and Gold (XAUUSD) is 3973.96

EURUSD

EURUSD traded narrowly in a 1.1476–1.1498 range as it consolidates this week’s losses. The single currency is garnering a bit of support after HCOB Eurozone and German Composite and Services PMIs were a tad firmer than expected. The report noted that “a key driver of growth in the services sector was Germany.” Traders are waiting for today’s US ADP data.

GBPUSD

GBPUSD remains under pressure and traded in a 1.3010–1.3053 range. Widespread US dollar demand, ongoing UK budget angst, and rising expectations for a Bank of England rate cut in December are fueling the sell-off. A move below 1.3000 could extend losses to the April low in the 1.2705 area.

USDJPY

USDJPY climbed in a 152.96–153.64 range on US dollar strength from sliding global equities, which reversed the “safe-haven yen” trade yesterday. Japan’s Vice Minister for International Affairs Atsushi Mimura raised the odds for FX intervention when he noted that “yen moves were deviating from what might be expected.” However, officials are not expected to act until prices are above 155.00.

AUDUSD

AUDUSD drifted lower in a 0.6479–0.6500 range. S&P Global Services PMI helped to contain the downside, rising to 52.5 from 52.4 in September, as did steady Services PMI data from China.

USDMXN

USDMXN climbed then fell in an 18.6418–18.7702 range, supported by general US dollar strength and domestic economic data showing softened consumer confidence and manufacturing activity. Banxico is expected to deliver a 25-basis-point rate cut tomorrow.

China

PBoC Fix: 7.0901 vs exp. 7.1336 (Prev. 7.0885)

Shanghai Shenzhen CSI 300 rose 0.19% to 4627.26

RatingDog Services PMI unchanged at 52.6 in October.

China targets 4.17% GDP annual growth through 2035.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics