November 12, 2025

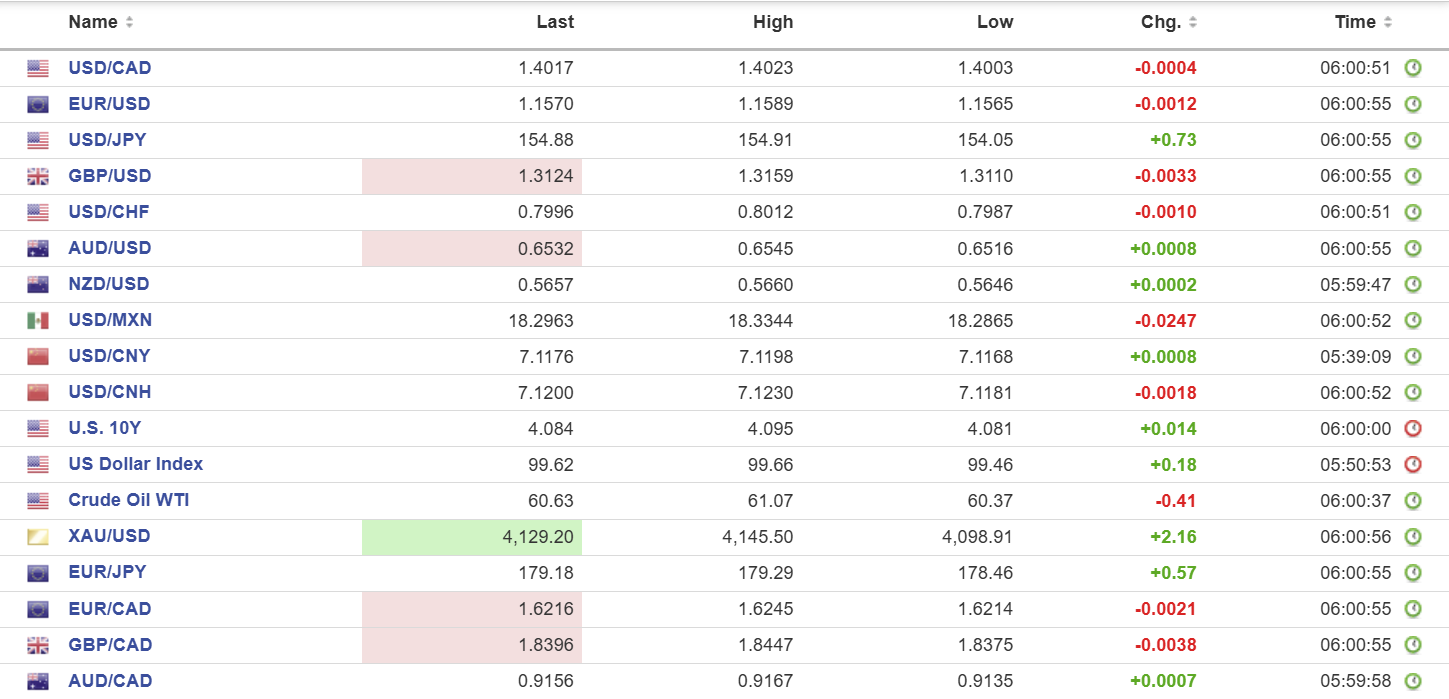

USDCAD open: 1.4017, overnight range 1.4003-1.4023, close, 1.4020

USDCAD tested the 1.4000 support area because of improved global risks sentiment following news that the US government shutdown may be coming to an end. The House of Representatives votes on the senate proposal this afternoon.

The Bank of Canada’s Summary of Deliberations report is on tap today. Analysts will be parsing the report to find clues about the future direction of rates. The October 29 rate cut to 2.25% was seen as a hawkish cut because Tiff Macklem implied that monetary policy could not do any more to boost economic growth; it was up to the government.

And it seems like the government will be dropping the “economic-boosting” ball. Carney refuses to announce new oil pipelines which are economic cash cows. Instead, he is announcing “major projects” which are guaranteed to burn through borrowed cash.

In that environment it is difficult to see USDCAD losses being sustained for any length of time.

WTI oil traded defensively in a 60.37-61.07 range with prices weighed down by ongoing concerns of an oil glut, exacerbated by Opec production increases.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish below 1.4030 and looking for a break aof support in the 1.4000 area to extend losses to the 1.3950-60 support zone. A move above 1.4050 suggests renewed 1.4000-1.4100 consolidation.

The long term uptrend from September 2008 is intact while prices are above 1.3170 (monthly chart) and the trendline is guarded buy support at 1.3360.

For today, USDCAD support is at 1.4000 and 1.3960. Resistance is at 1.4040 and 1.4070.

Today’s Range: 1.3990-1.4060.

The “House” Has the Ball

Markets are hoping that the longest U.S. government shutdown in history ends this afternoon when the House of Representatives votes on a funding bill approved by the Senate. Traders will shift their focus to the backlog of U.S. economic data that will soon be coming down the pipe.

There are plenty of Fed policymakers offering their views on the interest rate outlook today including NY Fed President John Williams, Trump’s toady Stephen Miran, Christopher Waller, Philadelphia Fed President Anna Paulson, Boston Fed President Susan Collins, and Atlanta Fed President Raphael Bostic.

Taking Stock

Asian equity markets are mostly higher. Hong Kong’s Hang Seng rose 0.85%, Japan’s TOPIX gained 1.14%, but Australia’s ASX 200 fell 0.22%.

As of 5:30 am PT, European bourses are mixed with the German DAX and the French CAC-40 up 1.29%, while the UK FTSE 100 index is flat. S&P 500 futures are up 0.34%, the U.S. Dollar Index (DXY) is 99.63, and the U.S. 10-year Treasury yield is 4.088%. Gold (XAUUSD) is $4131.59.

EURUSD

EURUSD traded in a 1.1565-1.1589 range overnight as it consolidated yesterday’s gains. Traders ignored yesterday’s German ZEW data and today’s German inflation data, which were as expected.

GBPUSD

GBPUSD traded erratically in a 1.3110-1.3159 range overnight. Yesterday’s weaker-than-expected U.K. employment data (-22,000 jobs in the three months ending in September; unemployment rate rose to 5.0% from 4.8%) raised the odds for a BoE rate cut in December. The U.K. press is rife with reports that Prime Minister Starmer could face a leadership challenge after the U.K. budget is delivered, which have been denied.

USDJPY

USDJPY continued to rally, rising from yesterday’s low of 153.05 to 154.91, where it is trading in early NY — a level last seen in February 2025. The move prompted Japanese Finance Minister Satsuki Katayama to hint at FX intervention to strengthen the yen. He said, “We’re seeing one-sided, rapid currency moves of late,” and added, “The government is watching for any excessive and disorderly moves with a high sense of urgency.” That’s the usual bluster, and it was ignored by traders. USDJPY continues to be bolstered by ongoing expectations of new fiscal stimulus, improved risk sentiment, and downgraded odds for a BoJ rate hike.

AUDUSD

AUDUSD traded in a 0.6215-0.6545 range but has slipped from the peak in early NY. RBA Deputy Governor Andrew Hauser said that policymakers were debating whether current monetary policy was restrictive enough to contain inflation, which underpinned the currency.

USDMXN

USDMXN added to yesterday’s losses in an 18.2865-18.3344 range on broad U.S. dollar weakness following the U.S. political news. The break below 18.3400 is setting the stage for a retest of the 2025 low of 18.1765. The USDMXN slide occurred despite soft economic data. Industrial production fell 2.4% y/y in September, but the result was still better than the -3.3% reading in August.

China

PBoC Fix: 7.0833 vs exp. 7.1141 (prev. 7.0866). Tuesday: 7.0866 vs exp. 7.1204 (prev. 7.0856).

Shanghai Shenzhen CSI 300 fell 0.13% to 4645.91.

China’s purchases of soybeans have reportedly stalled despite Trump’s claim that Beijing promised to buy 12 million tons.

A PBoC report says policymakers will implement a “moderately loose” monetary policy to ensure “reasonable and ample” liquidity. The report suggested that monetary policy easing is likely to be delayed, not set aside.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics