November 13, 2025

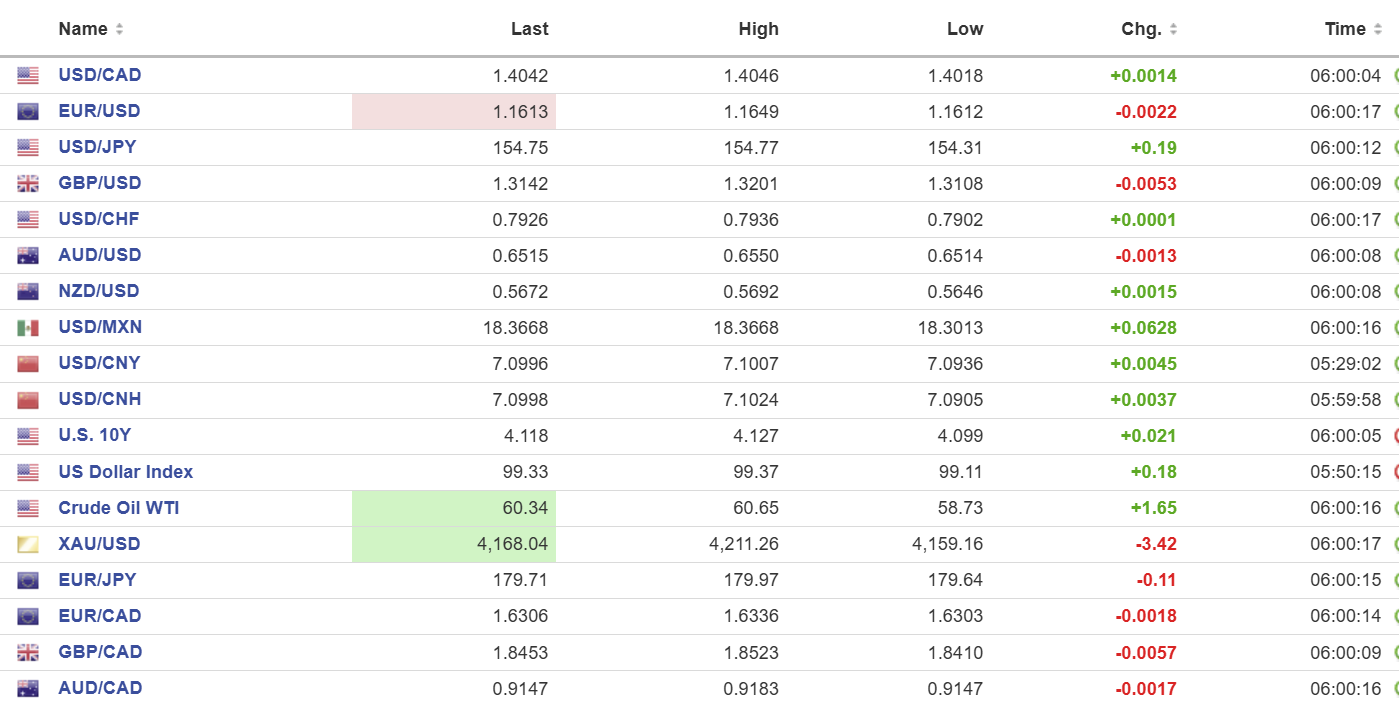

USDCAD open: 1.4039, overnight range 1.4018-1.4046, close, 1.4036

USDCAD rallied on the back of wide-spread US dollar demand on downgraded odds for the Fed to cut rates in December, which are 49.9% today, compared to 94.4% a month ago. A spate of hawkish comments from a slew of Fed officials and concern about the quality of upcoming US economic data have derailed easing hopes.

Prime Minister Mark Carney announced a batch of major projects like rare earths mining, electricity and LNG which will get fast tracked in what he called a “nation building” effort. Carney said that to get approval the projects have to advance the interests of Indigenous people and must contribute to sustainable clean growth. So, there you have it. Mr. Carney remains focused on his personal climate change agenda rather than the prosperity of Canadians.

WTI oil popped to 60.65 from 58.73 on general US dollar strength and on news that Ukraine launched drone and missile attacks on Russia’s Novorossiysk oil terminal that forced it to shut down. Prices have since retreated to 59.73.

Canada Manufacturing Sales surprised to the upside, rising 3.3% m/m in September,(forecast 2.8%) as did Wholesale Sales which rose 0.6% m/m compared ot the forecast for flat growth.

USDCAD Technical Outlook

The intraday USDCAD technicals flipped to bullish with the break above 1.4020 yesterday and are looking for a move through resistance at 1.4050 to extend gains to 1.4080. A move below 1.4010 puts 1.3960 in play.

The medium term technicals are unchanged from yesterday. They are bullish as long as USDCAD holds above the 1.3840 to 1.3940 support zone 100-day MA (1.3835), and the 200-day MA (1.3945). This area has repeatedly contained corrective dips and preserves the medium-term pattern of higher lows. A sustained move above 1.4100 would target the 1.4180–1.4250 area.

For today, USDCAD support is at 1.4010 and 1.3960. Resistance is at 1.4080 and 1.4120

Today’s Range: 1.3990-1.4090.

Surprise! Tariffs Cause Food Shortages

Trump is beginning to realize that his tariff strategy has consequences for Americans, at least those that like to eat and are not members of Mar-a-Lago. He is considering broad exemptions on some tariffs to help reduce elevated food prices, which may include citrus and beef products.

Trump is also annoyed that his “great name” is being sullied by what he is now calling “the Jeffrey Epstein Hoax.” He is irate that the media is reporting how his name comes up 1,500 times in Epstein’s emails, along with all those pictures of a smiling Donnie with his bestie Epstein. What a hoax, indeed.

Risk Aversion Returns

Traders are finishing the week a tad risk averse as the euphoria following the news that the US government reopened turned to fear that corrupted and dodgy US data will force the Fed to leave rates unchanged next month.

Those fears were underscored by comments from Fed officials Wednesday and yesterday. St. Louis Fed President Alberto Musalem, Cleveland Fed President Beth Hammack, and Minneapolis Fed President Neal Kashkari expressed variations of the theme that policymakers need to proceed with caution due to uncertain data and sticky inflation.

Taking Stock

Asian equity markets closed with losses led by a 1.57% drop in Hong Kong’s Hang Seng index. Australia’s ASX 200 fell 1.36%, and Japan’s Topix lost 0.65%.

As of 5:40 am PT, European bourses are deep in the red. The UK FTSE 100 leads the way, losing 1.80% so far. The German DAX has lost 1.75%, and the French CAC 40 is down 1.59%. S&P 500 futures have lost 1.21%, the US Dollar Index (DXY) is 99.07, and the US 10-year Treasury yield is 4.075%. Gold (XAUUSD) is 4053.53, down 118.99 since yesterdays close.

EURUSD

EURUSD traded in a 1.1609-1.1649 range as it consolidated gains from the US government reopening announcement. The single currency barely budged when Eurozone employment, trade, and Q2 GDP data was released as traders are focused on the US interest rate outlook.

GBPUSD

GBPUSD enjoyed a wild ride in a 1.3101-1.3201 band on reports and rumours surrounding the upcoming budget on November 26. GBPUSD hit the low on a report that Chancellor Rachel Reeves and Prime Minister Keir Starmer were bailing on plans to scrap income tax hikes. Traders view that move as putting politics above the country’s finances. Then another rumour emerged that the Office for Budget Responsibility (OBR) delivered improved financial forecasts, which may have negated the need for hikes. It is all fun and games until budget day.

USDJPY

USDJPY consolidated yesterday’s losses in a 154.31-154.77 band. Analysts do not think that the Takaichi administration has an interest in intervening in FX markets partly because it would deplete reserves that may be needed to offset US tariffs.

AUDUSD

AUDUSD gave back yesterday’s gains and is trading at its session low in a 0.6505-0.6550 range. The losses are due to renewed US dollar strength on profit taking and risk aversion ahead of the weekend.

USDMXN

USDMXN drifted higher in an 18.3013-18.3843 band and is near the top in early NY trading. USDMXN snapped an October uptrend with the move below 18.4250 on Monday, and as long as prices are below 18.4420, today’s rally is just a correction.

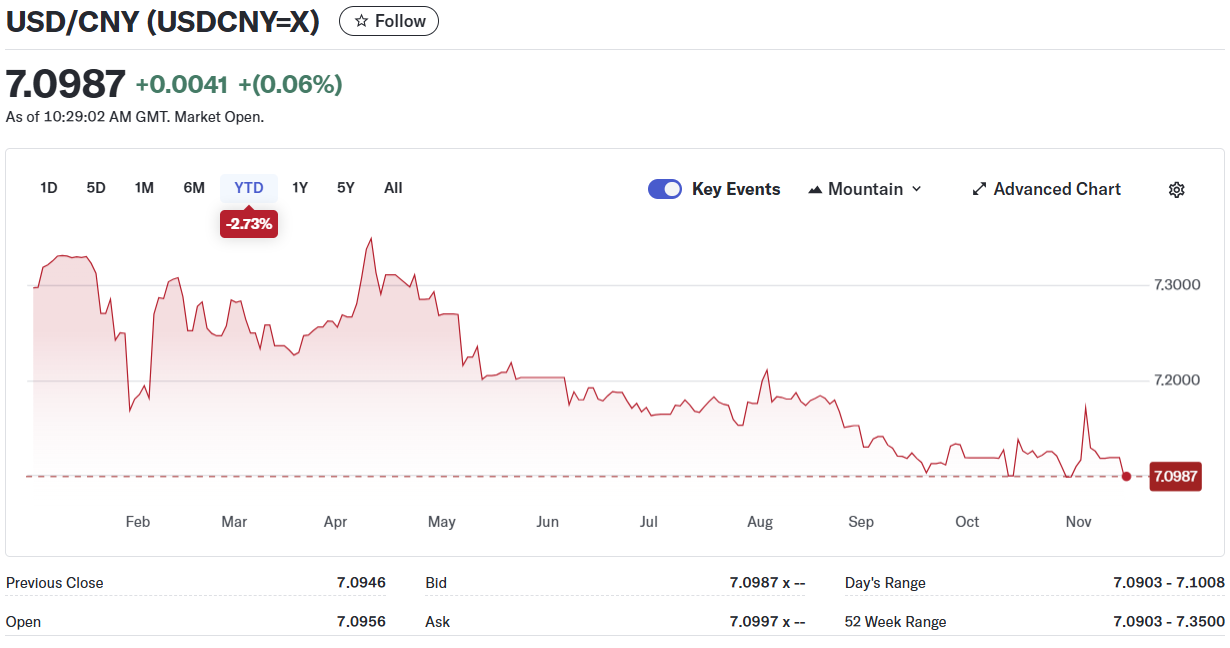

China

PBoC Fix: 7.0825 vs exp. 7.0964 (prev. 7.0865).

Shanghai Shenzhen CSI 300 fell 1.57% to 4628.14.

China is still annoyed that Japanese Prime Minister Takaichi met with a Taiwan official.

October Industrial Production 4.9% y/y (forecast 5.5%, September 6.5%).

Beijing summoned Japan’s Ambassador Kenji Kanasugi to yell at him because Japan Prime Minister Sanae Takaichi suggested Japan could use its military if a Taiwan contingency was seen as a “survival threatening situation” for Japan. She later clarified that she was speaking hypothetically. Her clarification did not satisfy Chinese officials.

Retail Sales 2.9% y/y (forecast 2.8%, prev. 3.0%)

Unemployment Rate Urban Area 5.1%, Prev. 5.2%)

House Prices -2.2% y/y vs September. -2.2%

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading EconomicsDaily