November 19, 2026

USDCAD open: 1.4003, overnight range 1.3983-1.4020, close 1.3990

USDCAD is ignoring domestic influences including economic data and the latest Canadian government budget. Traders are focused on Wall Street and the latest tech stock correction because of chatter about inflated AI spending. Nvidia’s earnings are released at the end of the day, after the 2:00 pm release of the October 29 FOMC minutes. That suggests traders will stay close to home leaving USDCAD inside its well-traveled 1.3960-1.4060 range.

And after very Liberal budget for the past 10 years, taxpayers across the country sing “Saint Peter don’t you call me, ‘cause I can’t go, I owe my soul to the Liberal store. You work all day and what do you get? One day older and deeper in debt” ( Tennessee Ernie Ford’s “Sixteen Tons’).

WTI oil gave back yesterday’s gains and is trading at the bottom of its 59.45-60.78. Prices traded defensively following yesterday’s API report showing US weekly inventories rose by 4.4 million barrels last week.

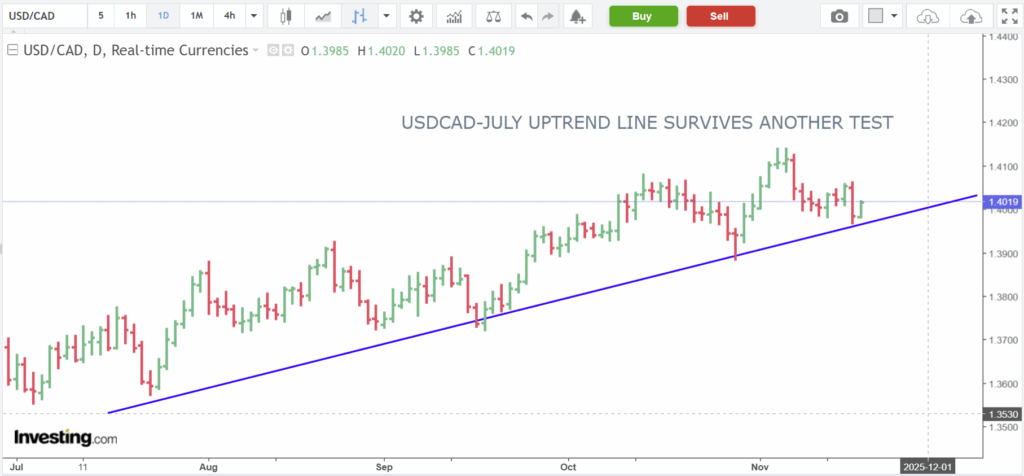

The intraday USDCAD technicals are slightly bearish while trading below 1.4020 which is suggesting that the gains from the overnight low are merely a correction before the next leg lower. If so, USDCAD may test the long term uptrend line at 1.3960.

Longer term, the 1.4090 represents the 50% Fibonacci retracement of the October 2025-January 2025 range and will continue to act as resistance while the 61.8% level at 1.3940 is the floor.

For today, USDCAD support is 1.3960 and 1.3940. Resistance is 1.4020 and 1.4060. Todays range 1.3980-1.4060.

FOMC Minutes and Nvidia

The FOMC minutes may just reignite the debate about the “divided Fed,” which has been reinforced in a series of speeches and interviews by numerous policymakers. Trump reiterated that he wants Fed Chair Jerome Powell gone and said he could name a successor before Christmas.

There are plenty of US economic reports released this morning but the quality of the data is questionable, which suggests it will have limited impact.

The Tech stock/AI rout is the story and Nvidia’s quarterly earnings results will either accelerate the sell-off or ignite another rally. They won’t be available until after the market is closed.

Taking Stock

Asian equity continued to trade negatively but not nearly as bad as yesterday. Japan’s Topix fell 0.17%, Hong Kong’s Hang Seng index lost 0.38% and Australia’s ASX 200 dropped 0.25%.

As of 5:40 am PT, European bourses are in mixed. The German Dax is up 022%, while the French CAC 40 is flat and the UK FTSE 100 is down 0.19%. S&P 500 futures have gained 0.33%, the U.S. Dollar Index is 99.69, the 10-year Treasury yield is 4.108% and gold (XAUUSD) is 4112.16.

EURUSD

EURUSD traded in a 1.1566-1.1597 range, with the release of the Eurozone October inflation data not much of a factor. Both headline and core inflation figures were steady or slightly softer than previous readings, confirming that price pressures remain under control and are not accelerating. Labour cost growth eased to 3.5% from 3.6% y/y. Today’s data reinforces expectations for the ECB to remain on hold.

GBPUSD

GBPUSD dropped to 1.3101 from 1.3156 after October CPI data showed inflation rising 3.6% y/y, a tick higher than the 3.5% that was expected but down from 3.8% in September. PPI data was also softer than anticipated, which reduces the need for the BoE to raise rates. Traders are also cautious ahead of the November 28 Fall Budget.

USDJPY

USDJPY traded erratically in a 155.22-156.20 range, with the low seen in early Asian trading. Yen demand from risk aversion sentiment stemming from the global stock market sell-off is offset by reports of new fiscal stimulus and an expected rate hike being pushed out until the spring. The ongoing China/Japan feud is also underpinning USDJPY, as are firm US Treasury yields. Traders are also leery of FX intervention.

AUDUSD

AUDUSD traded in a 0.6476-0.6512 range, with the bottom seen following Q3 wage growth data which was 0.8% q/q, as expected and unchanged from Q2. AUDUSD is trading defensively due to weak equity markets which impact commodity currencies.

USDMXN

USDMXN consolidated yesterday’s losses in an 18.3147-18.3555 range, with favourable Mexican/US interest rate differentials acting as a headwind to gains. The slightly more hawkish tone from Banxico is another factor limiting USDMXN gains. However, traders are turning their attention to Mexico’s debt after Mexico’s finance executives association warned that growing debt could trigger credit downgrades in 2026. It estimates that Mexico’s public sector debt is over $1.0 trillion.

China

PBoC fix: 7.0872 vs exp. 7.1121 (Prev. 7.0856)

Shanghai Shenzhen CSI 300 rose 0.44% to 4588.29

Dutch government revokes its use of Goods Availability Act. It does not formally mean that Nexperia is being “returned” to China, but it does represent a significant easing of Dutch state intervention in the company.

China escalates its feud with Japan and re-banned aquatic products from Japan unless Japan PM Takaichi first “retracts these wrong statements and take concrete steps to uphold the political foundation of bilateral relation.”

EU opens anti-dumping investigation into Chinese exports of robotic lawnmowers into the EU.

Open High Low Close

Sources: Bloomberg, Reuters, Investing.com

.

.

Sources: Bloomberg, Reuters, Investing.com

.

.