November 21, 2025

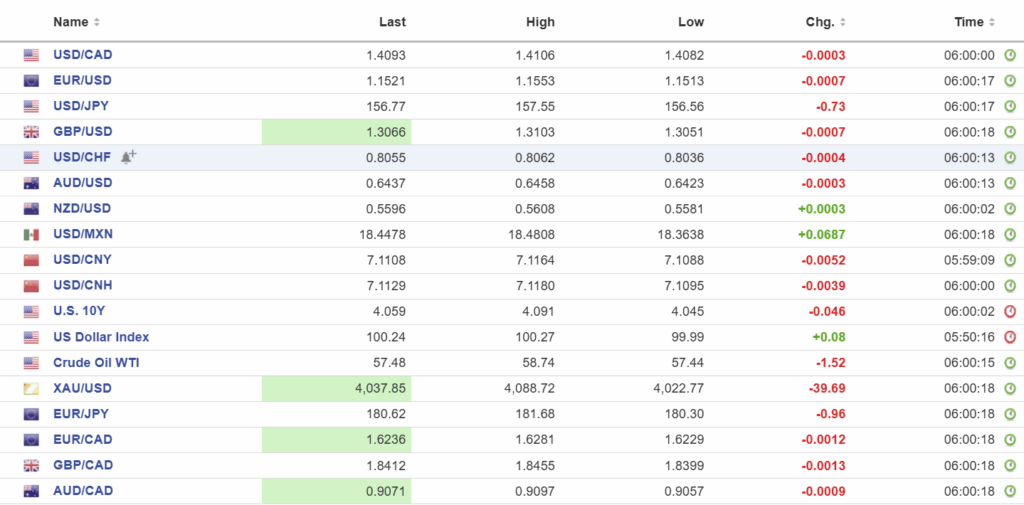

USDCAD open: 1.4093, overnight range 1.4082-1.4106 close, 1.4098

USDCAD was sideswiped by US economic data yesterday as traders reacted to what a best is a confusing mix of data and at worse, stale, and incomplete. Nevertheless it was enough for JPMorgan to yank their 25 bp rat cut forecast off the table and opt for a no-change result.

Broad-based US dollar demand, and downbeat economic comments from BoC policymakers on Wednesday underpinned USDCAD.

Canadian Retail Sales data surprised to the upside with the ex-auto’s component rising 0.2% m/m (forecast -.0.5%, while the headline number was as expected at -0.7%. The data is neither here nor there as it precedes Trump ending trade talks after the Ontario tariff ad.

WTI traded in a 57.44-58.74 range but is recovering its losses in NY trading and sits at 58.28. Oil prices are under pressure from hopes that Trump’s Ukraine/Russia peace plan bears fruit , although the EU is not in favour.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish while trading above 1.4060 which is being guarded by minor support at 1.4080. A decisive move above 1.4120 targets 1.4160.

The medium-term technicals are bullish while prices are above 1.4040 and are looking for a break of 1.4150 to target 1.4280. The momentum indicators are elevated but not overbought.

For today, USDCAD support is at 1.4080 and 1.4040. Resistance is at 1.4120 and 1.4160.

Today’s Range: 1.4080-1.4160

AI Deja Vu

Ai’s have long been known to suffer from hallucinations and for guessing at answers but with style. Yesterday (and overnight) they experienced déjà vu after disappointing, but dodgy, US employment numbers lowered December rate cut odds and reopened AI valuation wounds. The result is that stocks are poised to end the week with losses evoking memories of the Trump Liberation Day meltdown, while the US dollar rallied.

Michigan Consumer Sentiment and S&P Global Manufacturing and Services PMI data are on deck.

Taking Stock

Asian equity markets closed deep in the red. Hong Kong’s Hang Seng plunged 2.38%, Japan’s TOPIX dropped 1.84%, and Australia’s ASX 200 lost 1.59%.

As of 7:30 am, the German DAX is down 0.86%, the French CAC-40 has lost 0.34%, and the FTSE 100 index is down 0.38%. S&P 500 futures are down 0.36%, the US Dollar Index (DXY) is 100.33, the US 10-year Treasury yield has eased to 4.05%, and gold (XAUUSD) is $4049.11.

EURUSD

EURUSD traded erratically in a 1.1513–1.1553 range with the peak in Europe and the low in early NY trading. The price action remains a US dollar story due to downgraded expectations for a Fed rate cut in December. JPMorgan revised its outlook for Fed rates to unchanged from down 25 bps. ING analysts wrote that the Eurozone manufacturing and services PMI showed the economy was on a growth path. However, Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, seems to disagree. He wrote: “For months the manufacturing sector of the eurozone has been marooned in a no-man’s land of directionlessness. Production has picked up slightly since March of this year, but the overall situation has not improved during this period.”

GBPUSD

GBPUSD mirrored EURUSD moves and is trading near the bottom of its 1.3051–1.3103 band. UK PMI data disappointed. S&P Global Chief Economist Chris Williamson wrote: “November’s flash PMI surveys brought disappointing news on the UK economy. Economic growth has stalled, job losses have accelerated, and business confidence has deteriorated. The PMI is broadly consistent with no change in GDP in November and a meagre 0.1% quarterly pace of growth so far in the fourth quarter.” Traders are focused on the Autumn Budget due next Wednesday.

USDJPY

USDJPY dropped from 157.55 to 156.55 in a lively trading session. Prime Minister Sanae Takaichi’s government announced a 21.3 trillion yen ($135.4 billion) stimulus plan, but it still needs help from other parties to pass the spending bill. The news overshadowed the CPI and PMI data.

Meanwhile, Finance Minister Satsuki Katayama hinted at FX intervention when he said, “We are alarmed by recent one-sided, sharp moves in the currency market. It is important for currency rates to move stably, reflecting fundamentals. We will take appropriate action as needed against excess volatility and disorderly market moves, including those in the long term.”

AUDUSD

AUDUSD traded quietly in a 0.6423–0.6458 range, but with a negative bias due to US dollar strength from reduced odds of a Fed rate cut in December. AUDUSD downside received some support after October Manufacturing PMI data was better than expected (actual 51.6, previous 49.7).

USDMXN

USDMXN soared in a 18.3638-18.4808 range due to broad US dollar strength after the outlook for Fed rate cuts eased.

China

PBoC Fix: 7.0875 vs exp. 7.1154 (Prev. 7.0905)

Shanghai Shenzhen CSI 300 fell 2.44% to 4453.61.

China/Japan spat continues. Analysts are suggesting that China’s reaction is a not-so-subtle warning to other nations like the US, South Korea and Australia and to not change their existing policies on Taiwan.

China is buying record amounts of Russian LNG and at steep discounts.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics