December 2, 2025

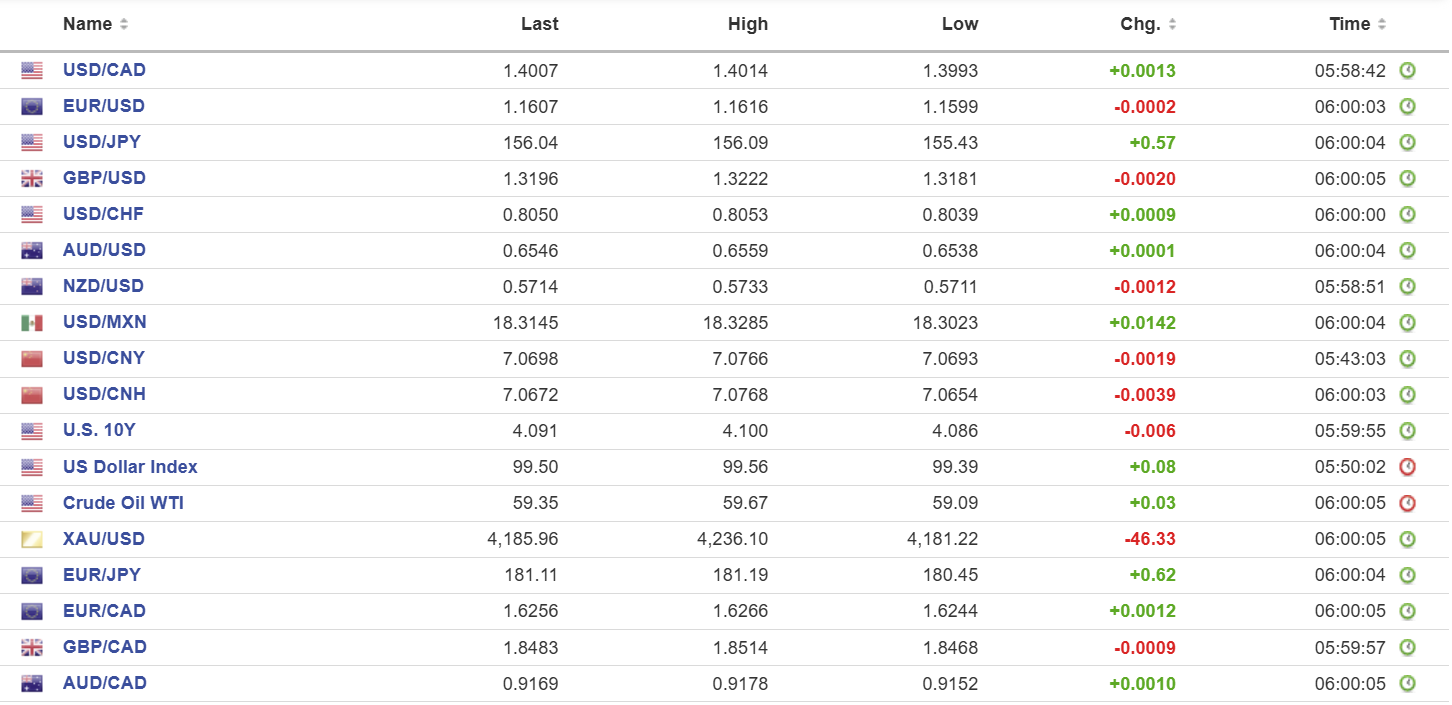

USDCAD open: 1.4007, overnight range 1.3993-1.4015, close 1.4000

USDCAD is mildly bid albeit in a quiet FX session due to a lack of market moving data or events. Friday’s USDCAD losses after the GDP data have given way to profit-taking following the jump in US 10-year treasury yields which is evidence of market “risk aversion.”

The greenback’s demand was spurred by yesterday’s ISM Manufacturing PMI data which declined to 48.2 from 48.7. The softer readings in new orders (47.4) and employment (44.0) painted a picture of weak demand and ongoing head-count reductions.

Laurentian Bank of Canada is no more. The company sold parts of itself to Fairstone Bank for $1.9 billion, while National Bank of Canada takes all the retail and small business assets. National Bank will pay something based on outstanding balances at closing. When all is said and done, there will not be any Laurentian branches in Quebec and most of its 2715 employees will be looking for a job.

Oil prices chopped about in a 59.09-59.67 range with gains capped by the risk of Russian oil returning to the market although that view was tempered by the risk Trump invades Venezuela.

USDCAD Technical Outlook

USDCAD tested support in the 1.3950-60 area yesterday and it held. The subsequent rebound drove prices though the descending trendline from November 25, at 1.4005 and if sustained, opens the door to further gains to 1.4060. A break below 1.3990 confirms the rally was merely a correction and the focus will return to testing support in the 1.3950 zone.

The medium-term technicals are unchanged. They are bullish with prices still above the 100 day moving average (1.3896) and 200 day moving average (1.3921) with strong resistance in the 1.4140-70 area.

For today, USDCAD support is at 1.3990 and 1.3960. Resistance is at 1.4040 and 1.4070.

Today’s Range: 1.3990-1.4040

Fraying Nerves

Rising Japanese JGB yields, plunging Bitcoin prices, and shaky stock markets and choppy FX markets are evidence that traders are feeling a tad risk averse. In addition, the lack of actionable and current US economic data has encouraged many traders to close their books for the year while others are biding their time until the December 10 FOMC meeting.

Taking Stock

Asian equity markets were steady and uneventful. Hong Kong’s Hang Seng index rose 0.24% while Australia’s ASX 200 rose 0.17%, and Japan’s Topix was flat.

As of 7:15 am, European bourses are trading positively. The German DAX is up 0.74%, the French CAC-40 has gained 0.33%, and the FTSE 100 index is up 0.28%. The US Dollar Index (DXY) is 99.47, the US 10-year Treasury yield is 4.11%, and gold (XAUUSD) is $4202.17.

EURUSD

EURUSD traded narrowly in a 1.1599–1.1616 band with traders keeping an eye on Russia/Ukraine peace talks. Eurozone inflation ticked up to 2.2% y/y in November, compared to 2.1% in October. The number is so close to the ECB inflation target of 2.0% that it will not impact ECB decision making, and it was ignored by traders. That sentiment was echoed by ECB Governing Council member Martin Kocher who said, “We can’t and shouldn’t conduct micro management via monetary policy.”

GBPUSD

GBPUSD drifted in a 1.3181–1.3222 band with the low seen in early NY trading. Opposition parties have decided that Chancellor Reeves misled the country about the country’s fiscal situation ahead of last week’s budget. They want her gone, but a spokesman at Prime Minister Kerr Starmer’s office reportedly said, “The PM has full confidence in Chancellor Reeves.” That statement may boost the odds that Ms. Reeves is fired in 2026 higher than the 63.6% on November 26. UK BRC Shop Prices rose 0.6% in November (previous 1.0%) and Housing Prices rose 0.3% m/m in November. The results were ignored.

USDJPY

USDJPY rallied from 155.43 to 156.09, which recouped all its losses from Friday. Broad-based US dollar demand after US 10-year Treasury yields rose from 4.036% yesterday to 4.10% today helped fuel the gains. The topside may be limited by expectations for a BoJ rate hike on December 19.

AUDUSD

AUDUSD traded quietly in a 0.6538–0.6559 band with prices supported by divergent central bank outlooks. The RBA could raise rates sooner than expected while the Fed is in easing mode. Australia’s current account deficit widened to AUD 16.6 billion from AUD 16.3 billion in Q2.

USDMXN

USDMXN inched higher in an 18.3023–18.3285 range due to widespread US dollar demand. USDMXN continues to be weighed down by the cautious Banxico outlook, which contrasts with expectations the Fed will be easing aggressively in the coming months.

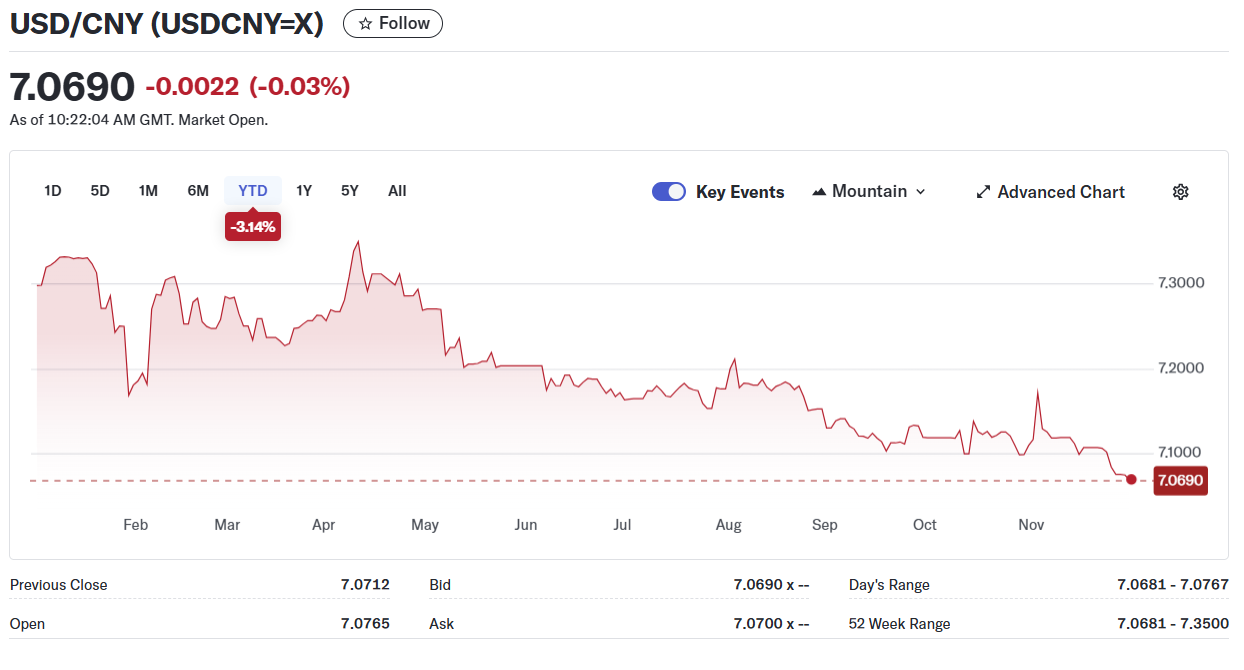

China

PBoC Fix: 7.0794 vs exp. 7.0746 (Prev. 7.0759)

Shanghai Shenzhen CSI 300 fell 0.48% to 4554.33

SCMP reports that a survey of 627 members of the German Chamber of Commerce in China, 57% of those companies are accelerating efforts to partner with Chinese rivals.

Morgan Stanley analysts are forecasting that China’s ongoing property slump will continue throughout Q1 2026

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics