By Michael O’Neill

The Canadian dollar tends to avoid a lot of drama in December, and this year should not be any different. In the past 10 years, and in the absence of global turmoil, the Canadian dollar managed to squeeze out gains in six of them. These are textbook year-end flows, driven not by domestic Canadian dynamics but by the global process of reducing USD exposure, rebalancing foreign equity portfolios, and unwinding hedges. In a normal year, this is what December looks like.

From 2020 onward, the chart shows USDCAD drifting lower into year-end as oil stabilized, risk appetite improved, and markets anticipated easier Fed policy. The exception was 2024, when the Canadian dollar lost about 2.5% with Trump’s looming presidency weighing on the currency. It is still early days, but the Canadian dollar is already grinding higher, and even the December 10 FOMC meeting is unlikely to derail the trend unless the Fed delivers a hawkish surprise.

Volatility is Depressed

It may be the season to be jolly, but USDCAD volatility indicators are feeling depressed. That’s because they are.

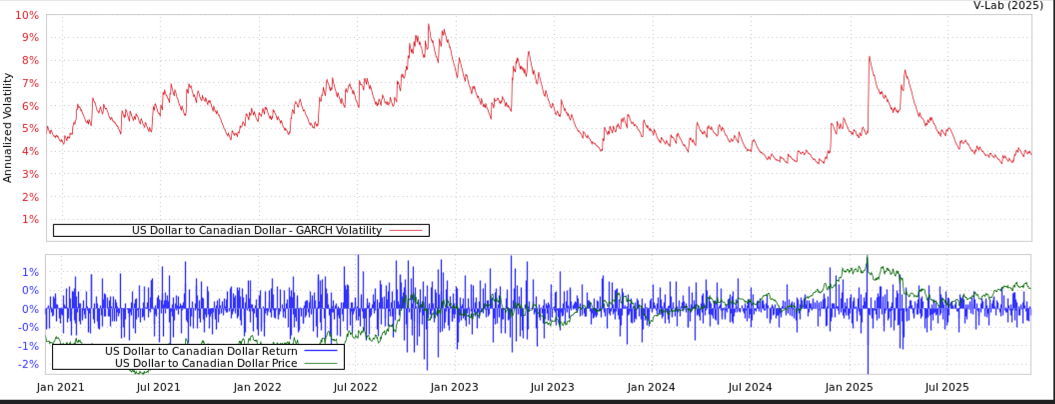

USDCAD volatility has slipped into one of its quietest phases in half a decade, and that sets the tone for the next month. The most recent GARCH (Generalized Autoregressive Conditional Heteroskedasticity) estimate sits at 3.84 percent, placing current conditions in the bottom 10% of the past five years and well below the historical average of 5.50 percent. In layman’s terms, it suggests traders do not expect any dramatic moves.

(Note: heteroskedasticity simply means that the error variance is not constant.)

Chart: USDCAD GARCH Volatility Analysis

Source: VLAB.Stern.nyu.edu.

Fed Delivers Early Christmas Gift

The odds that the FOMC delivers a 25 bp rate cut next week are 90%, which is kind of like a kid peeking at Christmas presents before Santa arrives — it crushes the surprise. That doesn’t mean policymakers won’t channel the Grinch. The Committee is far from united. Four members have argued for rate cuts at this meeting, five others have suggested it is too soon, and Fed Chair Jerome Powell and two other colleagues aren’t giving any clues. The debate could get messy, but for the most part it will just be noise as markets fully expect that the 2026 version of the Fed will be marionettes whose strings are controlled by Trump. And Mr. Trump wants to slash rates.

Away in an Ottawa Manger

Bank of Canada Governor Tiff Macklem does not face the same animosity as his Fed counterpart, but his rate decision is not any easier. He has already signaled that policymakers are inclined to keep rates steady, reminding markets at the October 29 meeting that the central bank has pushed its policy tools as far as it reasonably can. Further economic stimulus needs to come from the federal government.

His outlook appeared reinforced last week following Canada’s robust 2.6% gain in Q3 GDP. The reinforcement evaporated quickly thanks to sickly, frail details. Q2 growth was revised lower, export performance was flat, and there was continued softness in business investment. Those details have many forecasters assuming that Q4 growth could stall out. That should trigger a rate cut, but the BoC is likely to remain on the sidelines and await more data.

Hark! The OECD Angels Sing

The brain trust at the Organization for Economic Cooperation and Development are singing Canada’s praises, although off-key and quietly. They are looking for the domestic economy to rebound, albeit very weakly, as long as inflation remains soft.

The OECD claims that Canada is in a “rebuilding phase,” following the tariff shock that clobbered exports and business investment earlier in 2025, left GDP in the red, and put business and consumer confidence on life support. Even with inflation sitting around 2%, nobody felt particularly cheerful, and the jobless rate climbed to 6.9% by October.

The OECD expects GDP growth to grind up to 1.3% next year and 1.7% in 2027, boosted by a rebound in exports and a pickup in business investment. Consumers are expected to start spending while cheaper borrowing gives the housing market a lift. Inflation should stay close to target, with core drifting lower as wage pressures cool.

But that only happens without fresh trade drama from the US. The Canada-US-Mexico Agreement (CUSMA) is up for renewal next year, and President Trump will ensure the process is as smooth as tree bark.

December may fade quietly into the new year but things will get Loonie if there are FOMC fireworks.

.