December 19, 2025

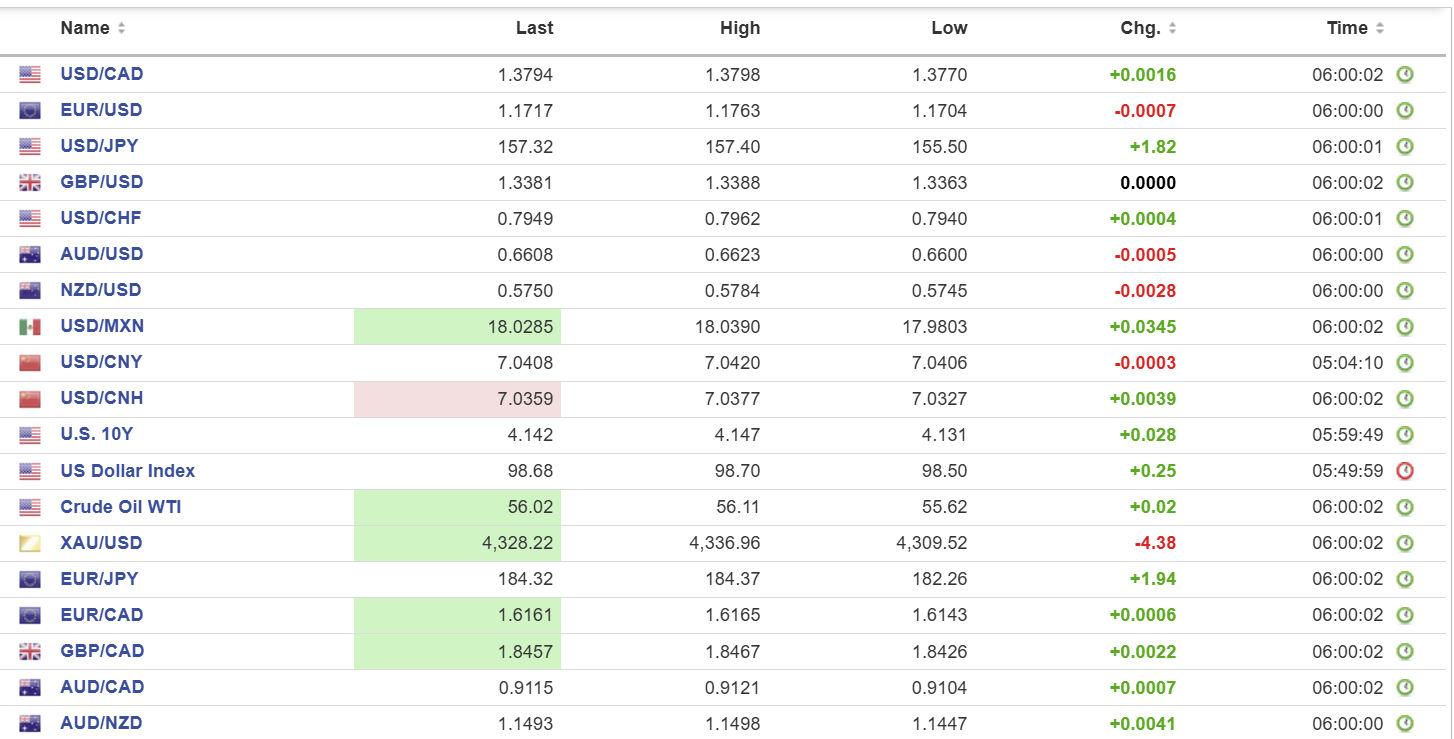

USDCAD open: 1.3794, overnight range 1.3770-1.3701, close 1.3780

USDCAD is ticking higher in quiet, holiday markets. The annual North American ritual of trains, planes and automobiles is in full swing as Canadian’s and American’s travel to meet with loved, and not-so-loved relatives, family and friends.

But not the employees at Statistics Canada. They were beavering away to deliver the October Retail Sales data. The report was a bit of a downer with headline Retail Sales falling 0.2% while Core retail sales were even weaker, dropping to -0.6%. StatsCanada expects retail sales to rebound and rise 1.2% in November

WTI oil prices trade in a 55.62-56.25 band, with gains capped by ongoing oversupply fears. While Trump’s plans to steal Venezuelan crude are limiting the downside.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish while prices are above 1.3740 and looking to break above 1.3810 to target 1.3880. Failure to break above 1.3810 argues for another test of support.

The medium-term technicals are bearish while prices are below the 100 and 200 day moving averages but for now are trapped in a 1.3740-1.3880 range.

For today, USDCAD support is at 1.3760 and 1.3740. Resistance is at 1.3810 and 1.3850

Todays Range 1.3740-1.3840

Inflation Fantasy

US inflation cooled in November, with the headline number at 2.7% (forecast 3.1%) and Core CPI rising 2.6% (forecast 3.0%). For a brief moment, markets reacted like the numbers were irrefutable evidence that US inflation was cooling and the Fed had a clear path to cut rates. Except the numbers are garbage. There was no data from October, and the November numbers were incomplete. The reality is, markets did not learn anything new about the state of inflation in America.

President Trump said that the “affordability” crisis in America is fake news and described the word “affordability” as a con job by Democrats. His delusion will be in the spotlight today when the Michigan Consumer Sentiment Index is released. The index has plunged from 71.1 when he took office to 53.3 in November.

Taking Stock

Asian equity markets ended the week optimistically. Japan’s Topix rose 0.80%, Hong Kong’s Hang Seng gained 0.76%, and Australia’s ASX 200 rose 0.39%.

As of 5:30 am PT, European bourses and S&P 500 futures are dancing around flat. The US Dollar Index is 98.66, the US 10 year Treasury yield is 4.151%, and gold (XAUUSD) is 4332.08.

EURUSD

EURUSD traded softer in a 1.1704–1.1763 range, with the currency pair giving back all of its post ECB gains. To no one’s surprise, the ECB left rates unchanged but upwardly revised its growth and inflation projections. That has led many analysts to predict that the ECB’s easing cycle is over and the next move, albeit a long way down the road, will be a hike. President Christine Lagarde declined to offer any forward guidance due to “the degree of uncertainty that we are facing.” German producer prices fell 2.3% y/y in November compared to -1.8% in October.

GBPUSD

GBPUSD flatlined in a 1.3357–1.3388 range, with traders ignoring an increase in GfK consumer confidence (actual -17, November -19), simply because it still means consumers have a pessimistic view of the economy. Retail sales numbers were a non event. The BoE cut rates to 3.75% from 4.0% yesterday, but the outlook for further cuts is unclear as the board is split.

USDJPY

USDJPY soared from the pre BoJ decision level of 155.50 to 157.40, where it is in New York, after the Bank of Japan raised its benchmark rate to 0.75% as expected. The rally suggests that the hike was fully priced in, but not the dovish implications from the statement. The statement noted that consumer inflation was expected to fall below 2.0% next year, and analysts are suggesting further rate hikes may not occur for at least six months. The statement did not make any mention of FX concerns either.

AUDUSD

AUDUSD traded quietly in a 0.6600–0.6623 range, with traders content to drift into the holidays. AUDUSD continues to be underpinned by this week’s consumer inflation expectations data, which suggests the RBA’s next move could be a hike.

USDMXN

USDMXN rose choppily in a 17.9803–18.0390 range after the Bank of Mexico trimmed its benchmark rate to 7.0% from 7.25%, as expected. Banxico signaled that it may take a breather from further rate cuts after saying it would “carefully assess the impact on inflation from tax and tariff increases.”

China

PBoC Fix: 7.0550 vs exp. 7.0378 (prev. 7.0583)

Shanghai Shenzhen CSI 300 rose 0.34% to 4568.18

China’s holdings of US Treasuries have fallen by nearly half from their 2013 peak, according to the SCMP. Total US national debt is currently estimated to be at an all time high of $36–38 trillion in gross federal debt. If China, and other wealthy nations, avoid US debt, who will fund America’s lifestyle?

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics