January 14, 2026

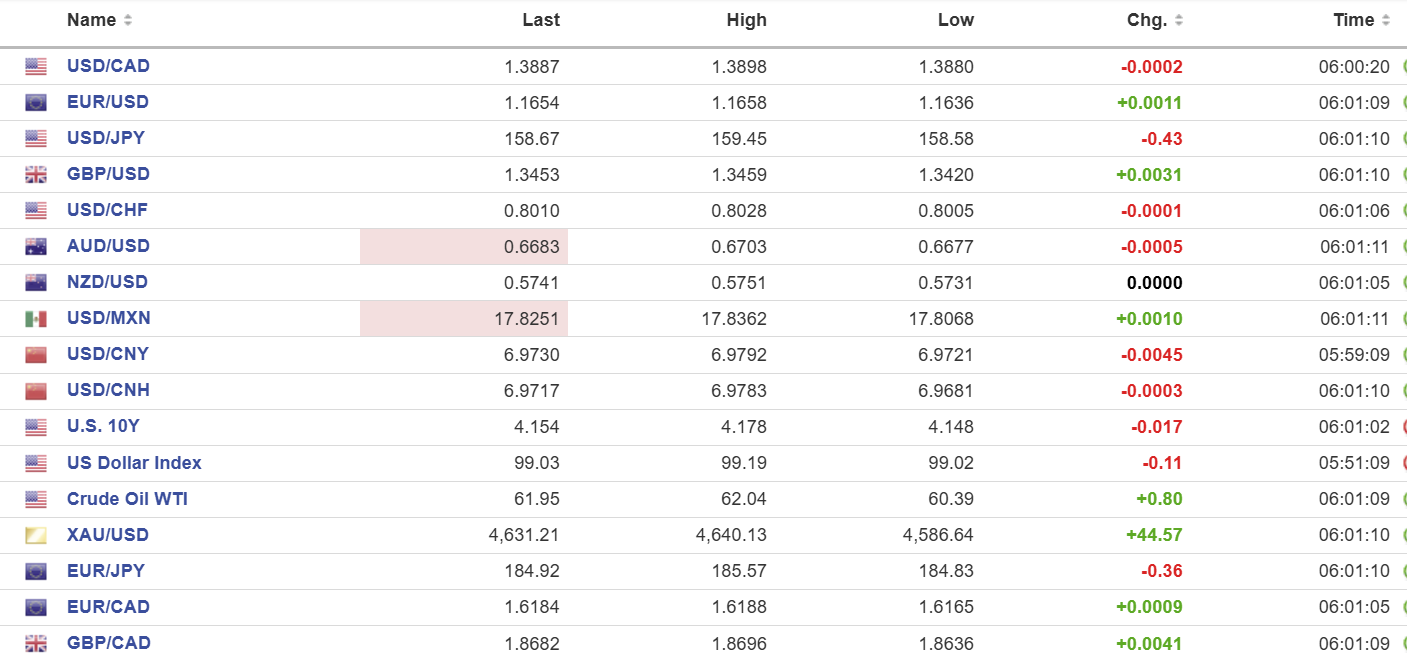

USDCAD open: 1.3888, overnight range 1.3871-1.3898, close 1.3893

USDCAD was sidelined overnight despite firmer oil and gold prices and narrowing CAD/US 10-year interest rate differentials.

USDCAD may be getting a bit of support after Trump said that the Canada-US-Mexico Agreement (CUSMA) on trade was irrelevant, claiming Canada wants and needs it. Those comments set the stage for a rather testy renegotiation and possibly an outright scrapping of the tri-lateral deal.

Prime Minister Carney is in China hoping to reset the fractured relationship, get agricultural tariffs removed and reopen the door to increased trade. Improving the relationship with Beijing risks further antagonizing Trump.

WTI oil is trading at levels last seen in October due to Trump’s threat of intervening in Iran. Traders fear that US action would have a negative impact on Iran’s 3.3 million barrels/day crude output. However, gains are capped after API reported a 5.27 million barrel increase in US crude inventories for last week.

A number of Fed officials are speaking today (Bostic, Kashkari, Miran, Williams) and other than Stephen Miran, could use the opportunity to defend Fed independence.

USDCAD Technical Outlook

The intraday USDCAD technicals are unchanged from yesterday. They are cautiously bullish while prices hold above 1.3840 and looking for a move above 1.3900 to extend gains to 1.3940. A move below 1.3840 puts 1.3800 in play,

The medium-term outlook is bullish after the November downtrend line was decisively broken, shifting the bias back toward consolidation-to-higher. Prices remain supported above 1.3780, a level that now marks the lower boundary of the post-December recovery zone. The broader uptrend will require confirmation via a sustained break and close above the 100-day moving average at 1.3905, which would place the 1.40–1.4065 resistance band back into focus.

For today, USDCAD support is at 1.3840 and 1.3810. Resistance is at 1.3920 and 1.3960.

Todays Range 1.3850-1.3920

Data Dismissal

There was a time back in September when the release of US inflation numbers would ignite a new flurry of Fed interest rate forecasts. That wasn’t the case yesterday. December Core CPI was lower than expected (actual 2.6%, forecast 2.7%, November 2.6% y/y), and the results were essentially ignored. That’s because traders and analysts do not trust the data, which is still sketchy because of the government shutdown.

Today’s US PPI and Retail Sales results suffered the same fate. Core Producer Prices rose 3.0% in November, compared to 2.6% in September (there were no October numbers). The Retail Sales Control Group rose 0.4% in November compared to 0.6% in September. So far, FX markets and equity futures barely budged.

Taking Stock

Asian equity markets finished higher. Japan’s Topix climbed 1.26%, Hong Kong’s Hang Seng Index rose 0.56%, while Australia’s ASX 200 climbed by 0.14%.

As of 5:30 am PT, European bourses are mixed. The UK FTSE 100 is up 0.38%, and the French CAC 40 is flat, while the German DAX is down 0.44%. S&P 500 futures are down 0.35%, the US Dollar Index is 99.08, the US 10-year Treasury yield is 4.154%, and gold (XAUUSD) is 4631.72

EURUSD

EURUSD drifted in a 1.1636–1.1658 range and is at the top of that band in early NY. Traders are looking for fresh catalysts, and the latest US economic data is not doing it for them. Geopolitics continue to be a distraction, but even talk that the US would use military force to seize Greenland is considered more of a Game of Thrones fantasy than an actual threat.

GBPUSD

GBPUSD is directionless in a 1.3420–1.3459 range. The failure to extend gains above 1.3570, and expectations for additional Bank of England rate cuts, warn that a break below 1.3420 would extend losses to 1.3270.

USDJPY

USDJPY retreated from its overnight peak of 159.45, mainly because of Bank of Japan intervention concerns. The Nikkei reports that Prime Minister Sanae Takaichi apparently told her senior ministers of her plan to dissolve parliament as early as January 23 and to call an election in February. The plan is to increase the number of LDP seats, which would enhance her ability to drive her fiscal stimulus initiative.

AUDUSD

AUDUSD traded defensively in a 0.6677–0.6703 range due to modest US dollar demand against the majors. The topside remains capped for now as traders downgrade risks that the RBA will raise interest rates any time soon, while the Fed will leave rates unchanged.

USDMXN

USDMXN consolidated yesterday’s losses in a 17.8068–17.8362 range. This downside pressure is due to a mix of ongoing Fed independence questions and Banxico’s earlier suggestion of being in no hurry to ease monetary policy further.

China

PBoC Fix: 7.0120 (Prev. 7.0103)

Shanghai Shenzhen CSI 300 fell 0.40% to 4741.93

December trade surplus rises to $114.1 billion (forecast $113.6 billion, previous $111.68 billion). China’s trade surplus rose to nearly $1.2 trillion in 2025, despite the US share of Chinese exports falling to just 11.0%, a historic low. Analysts suggest that global demand for China’s goods and the competitiveness of its exports will likely keep foreign shipments on the rise in 2026, especially if the trade ceasefire with the US holds.

FX High, Low, Open

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics