January 22, 2026

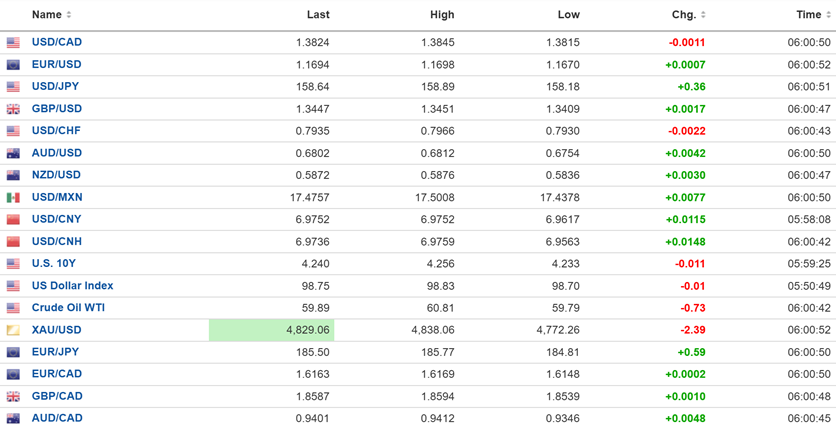

USDCAD open: 1.3824, overnight range 1.385-1.3845, close 1.3835

USDCAD dipped to its session low on the heels of another good weekly jobless claims report that improves the odds for Fed rate cuts. US GDP rose 4.4% q/q in Q3 (forecast 4.3%) while Personal Consumption Expenditures prices were unchanged at 2.8% q/q in Q3.

Trump’s Davos speech was a long-winded ode to himself supported by exaggerated, if not outright bogus claims of achievement. Later, he expressed his displeasure with Prime Minister Mark Carney after Carney’s Davos speech garnered a standing ovation (his didn’t). Trump said “ Canada gets a lot of freebies from us, by the way. They should be grateful, also, but they’re not. I watched your Prime Minister yesterday. He wasn’t so grateful.” Arguably the fall-out will be seen in tougher US/Canada trade talks this year.

WTI oil prices traded lower in a 59.49-60.81 range and are near the bottom of that band in NY. API reported that crude inventories rose by 3.04 million barrels last week which contributed to the selling pressure. In addition, Reuters reported that two American companies, Valero and Phillips 66 bought cargos of Venezuelan crude stolen by Trump at heavily discounted prices.

FX markets could get choppy with the release of today’s US data which includes, weekly jobless claims, and core PCE price index

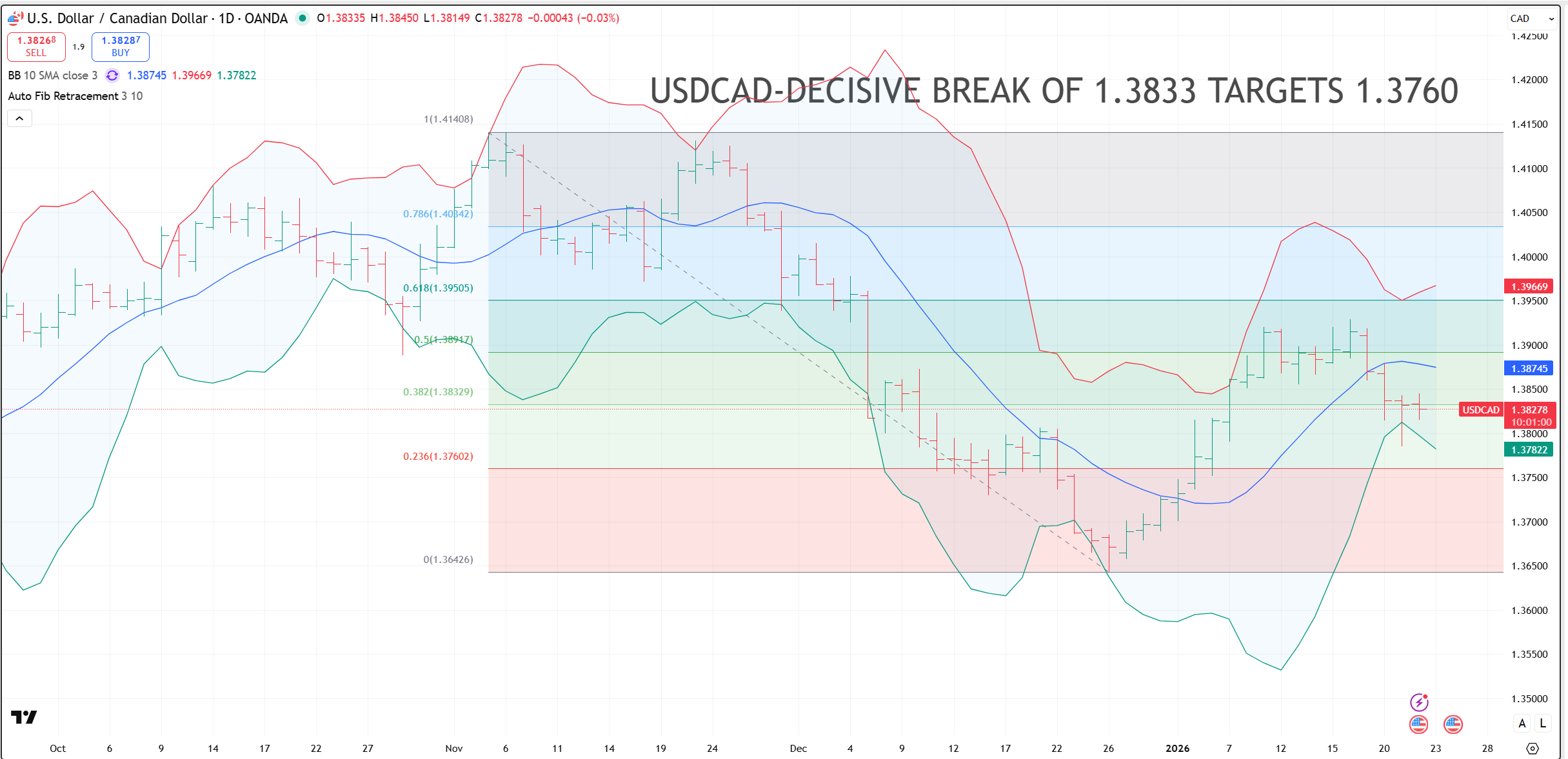

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish below 1.3850 and looking for a retest of support at 1.3780. A downside break targets 1.3740, then 1.3650 while a move above 1.3850 points to further 1.3780-1.3910 consolidation

The medium-term technicals are bearish below 1.3850 and are looking for a break of support at 1.3740 to extend losses to 1.3650.

For today, USDCAD support is at 1.3780 and 1.3740. Resistance is at 1.3850 and 1.3870.

Today’s Range: 1.3750-1.3840

One Door Closes and Another Door Opens

The US dollar is trading lower compared to yesterday’s close, gold prices have retreated (but remain above $4800.00), and Treasury yields have eased after the Trump Davos circus moved on. Markets have turned their attention to horse racing, specifically, what horse will the Fed Chair back in the Derby.

Trump’s (and it most certainly had to be Trump’s) decision to have the Justice Department subpoena Jerome Powell for a criminal investigation into Fed building renovation cost overruns blew up in his face.

Many pundits are reporting that Trump will lose the Supreme Court case about his ability to fire Governor Lisa Cook. Polymarket odds suggest Kevin Warsh is the leading candidate.

Greenland is for Greenlanders

Trump flip-flopped on Greenland. A few hours after telling a Davos audience he wanted “title and ownership,” he announced he was ruling out using military force and now had a “framework of a deal.” No details were available.

He ruled out using military force and then announced a framework of a deal, but apparently Greenland wasn’t involved in the talks.

Taking Stock

Asian equity markets bounced after the Davos drama fizzled. Australia’s ASX 200 rose 0.75%, Japan’s Topix rose 0.74%, and the Hong Kong Hang Seng gained 0.1%.

As of 5:30 am PT, European bourses are higher but still below the best levels seen earlier this week. The German DAX is up 1.00%, the French CAC-40 has gained 99%, and the UK FTSE 100 is up 0.38%. S&P 500 futures have risen by 0.59%, the US Dollar Index is 98.63, the 10-year Treasury yield is 4.258%, and gold (XAUUSD) is 4821.21

EURUSD

EURUSD traded sideways in a 1.1670–1.1698 range and then pooped to 1.1719 after the US data. Trump scrapped tariff plans for the eight countries that showed support for Greenland when he announced his “framework of a deal.” The intraday technicals are neutral inside a 1.1670-1.1750 range.

GBPUSD

GBPUSD is firmer inside a 1.3402-1.3453 with the peak seen, post US data. The focus has shifted from geopolitics to economic data and, of course, the Fed. GBPUSD is modestly bid while prices are above 1.3400 and looking for a break above 1.3460 to extend gains to 1.3510.

USDJPY

USDJPY rallied from 158.18 to 158.89 as long-yen, safe-haven trades were unwound due to Trump’s retreat from using the military to annex Greenland. Japanese exports rose 5.1% y/y, but that was below the 6.1% expected.

AUDUSD

AUDUSD continued this week’s rally as it traded in a 0.6754–0.6816 range. The peak hasn’t been seen since October 2024. Prices got an added boost after a better-than-expected employment report. Australian employment rose by 65,200 jobs in December, while the unemployment rate dropped to 4.1% from 4.4%. That data raised the odds for an RBA rate hike as soon as next month.

USDMXN

USDMXN is consolidating its recent losses in a 17.4378–17.5008 range due to broad US dollar weakness and downgraded global tariff risks. Mexican core inflation rose 0.43% in first half of January forecast 0.39%.

China

PBoC Fix: 7.0019 vs exp. 6.9697 (prev. 7.0014)

Shanghai Shenzhen CSI 300 rose 0.01% to 4723.71

National Bureau of Statistics claims jobless rate for those 16-24, excluding students fell to 16.5%, from 16.9% in December.

Former PBoC deputy governor Zhu Min told a Davos audience that consumption growth should be stronger than GDP

FX open high low

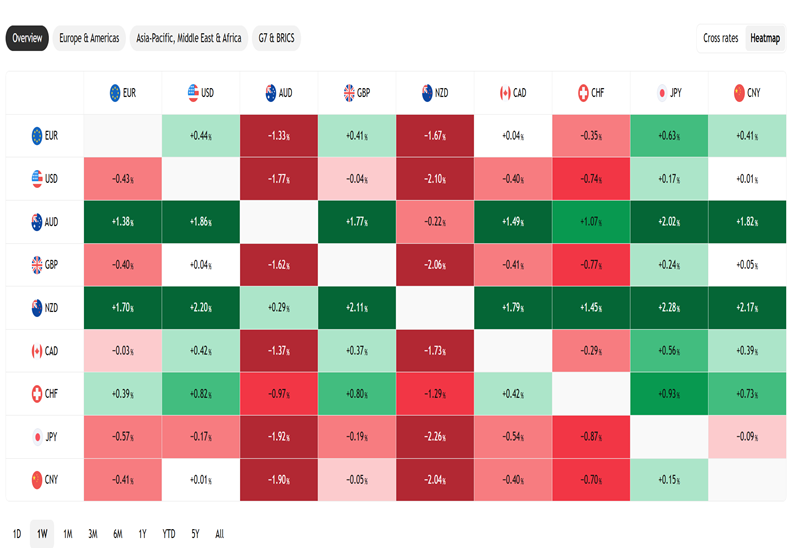

FX Heat Map (6:00 am) -one week

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview