February 6, 2026

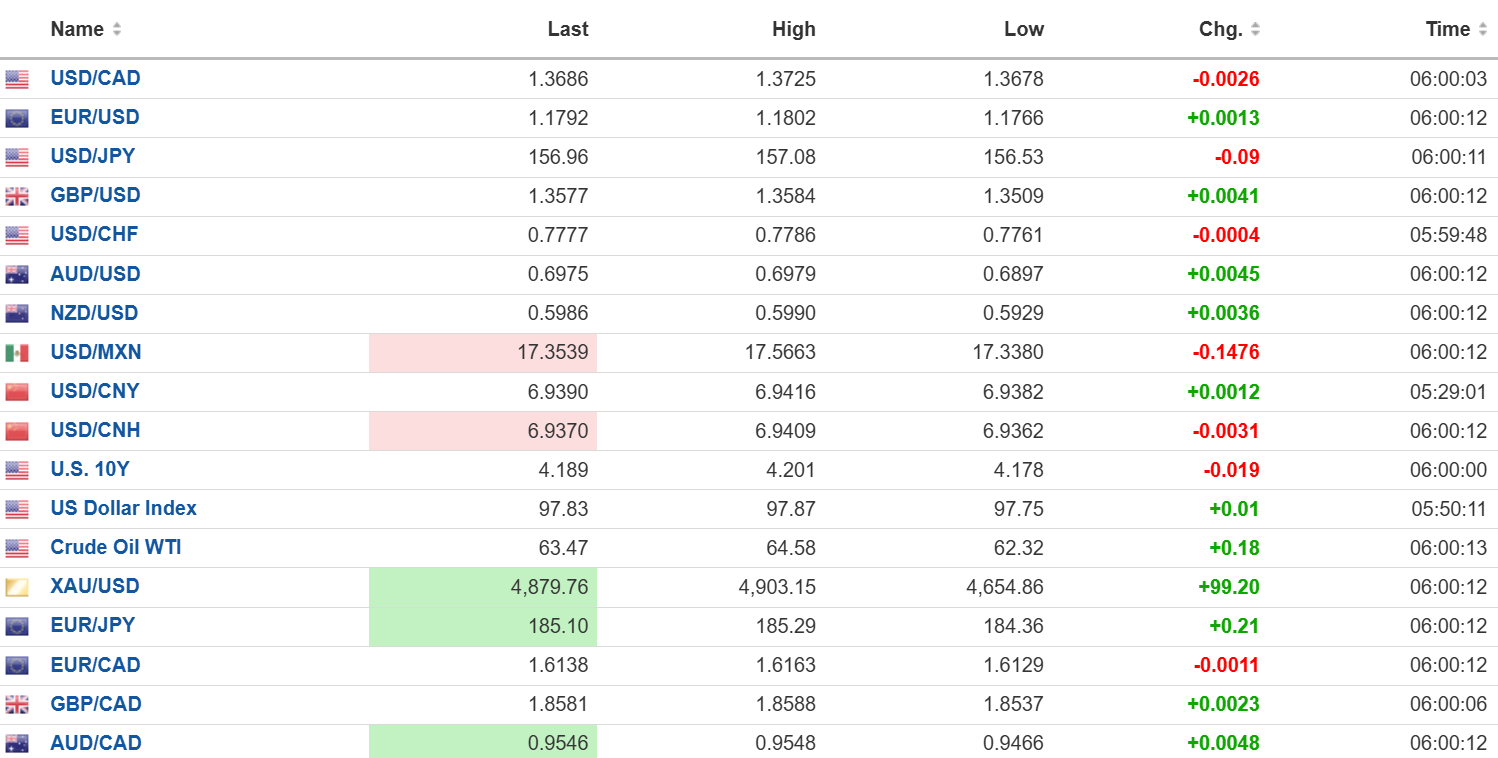

USDCAD open: 1.3686, overnight range 1.3649-1.3725, close 1.3713

USDCAD retreated from its session peak on the heels of general US dollar selling pressure against the majors.

Canada shed 25,000 jobs in January and the unemployment rate fell to 6.5% from 6.8%. StatsCanada said the employment rate decline was due to fewer people looking for work. If you recall, the January weather was rather nasty for a large swathe of the country and that is sure to have played a role in the job weakness. The private sector lost 52,000 jobs.

USDCAD dropped from 1.3674 to 1.3649 on the news but if the move is because the employment report increases the odds for a Bank of Canada rate cut, think again.

Governor Tiff Macklem was clear that domestic rates would be unchanged for a long while. Yesterday, he warned that Canada is not facing a normal cyclical downturn but a structural transition. U.S. protectionism, slower population growth, and the rise of artificial intelligence are permanently reshaping growth, trade, and jobs. Economic expansion will be modest, labour market outcomes uneven, and productivity gains slow to arrive. And monetary policy cannot fix it: it’s a job for the Feds.

WTI oil is trading softer in a 62.32-64.58 range in hopes that the US and Iran resolve some difference. The countries are meeting in Oman today.

US Michigan Consumer Sentiment is expected to tick down to 55 from 56.4, and Canada’s Ivey PMI index is expected at 49.7 (previous 51.9).

USDCAD Technical Outlook

The intraday USDCAD technicals are slightly bearish while prices are below 1.3700 and looking to test support in the 1.3640–60 zone. A move above 1.3700 shifts the focus to 1.3740.

The medium-term technicals suggest that the recent rally is a correction and, while prices are below 1.3770, a break below 1.3640 targets 1.3480.

For today, USDCAD support is at 1.3660 and 1.3620. Resistance is at 1.3720 and 1.3760.

Today’s Range: 1.3660–1.3740

US Job Market Weakening.

Thursday’s US jobs data showed a sharply higher increase in weekly jobless claims and a drop in job openings, clear evidence of a cooling job market. It may get even cooler. Amazon announced it was cutting 40,000 jobs while investing $200 billion to expand AI capabilities. US companies announced 108,000 layoffs in January.

That should incentivize the Fed to cut rates, but Atlanta Fed President Raphael is more concerned about inflation. Yesterday he said, “For me, inflation has been too high for too long. It’s important that our policy stay at a moderately restrictive posture, because that is a posture that increases the likelihood that we will get inflation back to our 2% target.”

The greenback gave back some of yesterday’s gains overnight, and many global stock markets halted their slide.

Taking Stock

Asian equities closed mixed, with Australia’s ASX 200 losing 2.03% due to fallout from the global tech stock plunge and soft commodity prices. Japan’s Topix rallied 1.28% in anticipation of new stimulus following Sunday’s election. Hong Kong’s Hang Seng lost 1.21% due to the fallout from the tech stock rout.

As of 5:30 am PT, European bourses are clawing back yesterday’s losses. The German DAX has climbed 0.53%, the UK FTSE 100 is up 0.16% and the French CAC 40 is flat. S&P 500 futures are up 0.59%, the US Dollar Index is 97.74, the 10-year Treasury yield is 4.201% and gold (XAUUSD) is at 4,930.77

EURUSD

EURUSD traded firmer in a 1.1766–1.1806 range due to broad US dollar weakness following yesterday’s weak American data and a very content-sounding European Central Bank. President Christine Lagarde said that the impact of the exchange rate gains is “incorporated into the baseline.”

German industrial production data was mixed, falling 1.9% m/m in December, while the year-over-year figure beat expectations, although it was still in negative territory (-0.6% y/y). ING analysts suggest it is only “temporary and that an industrial upswing is in the making.” EURUSD technicals are slightly bullish above 1.1750 and looking for a break above 1.1850 to target 1.1980.

GBPUSD

GBPUSD is at the top of its 1.3509–1.3596 range despite a somewhat dovish Bank of England policy meeting yesterday. The benchmark rate was left unchanged at 3.75% in a split decision and analysts are suggesting rates will be lowered in March. UK house prices rose 0.7% in January after dropping 0.5% in December. The prospect of a rate cut reinforces the GBPUSD downtrend, which is intact below 1.3680.

USDJPY

USDJPY traded higher in a 156.53–157.15 range due to caution ahead of the February 8 election and modest but broad-based US dollar weakness. USDJPY has traded higher all week mainly because of Prime Minister Sanae Takaichi’s prospects of winning a landslide victory, enabling her to drive her fiscal stimulus plans forward. If so, it hampers the ability of the BoJ to raise rates.

AUDUSD

AUDUSD rallied from 0.6897 to 0.6994 as it erased yesterday’s losses. The RBA Governor explained the rationale for its latest rate hike (from 3.60% to 3.85%) to parliament. She blamed the rise in inflation on low unemployment, higher incomes, lower interest rates, tax cuts and government spending. The intraday technicals are modestly bullish above 0.6910 and targeting 0.7050.

USDMXN

USDMXN traded lower in a 17.3380–17.5663 range, recouping all of yesterday’s losses. Banxico left its overnight rate unchanged at 7.0%. The move was expected because headline and core inflation rose. Policymakers predicted that inflation would get to its 3.0% target in H2 2027 rather than Q3 2026. The intraday technicals are bearish and looking for a break below 17.3400 to target 17.2300.

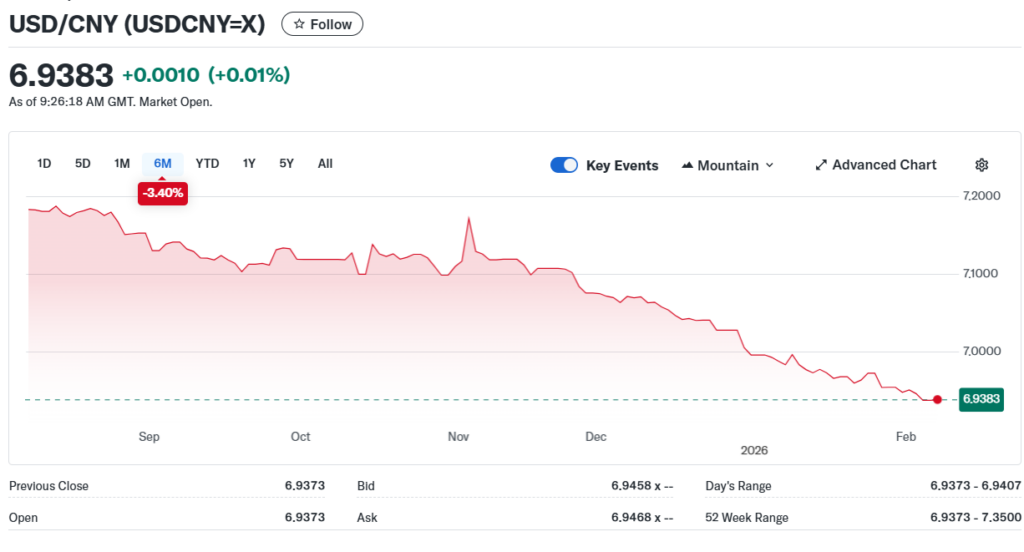

China

PBoC Fix: 6.9590 vs exp. 6.9517 (Prev. 6.9570)

Shanghai Shenzhen CSI 300 fell 0.57%% to 4643.60

FX open high low

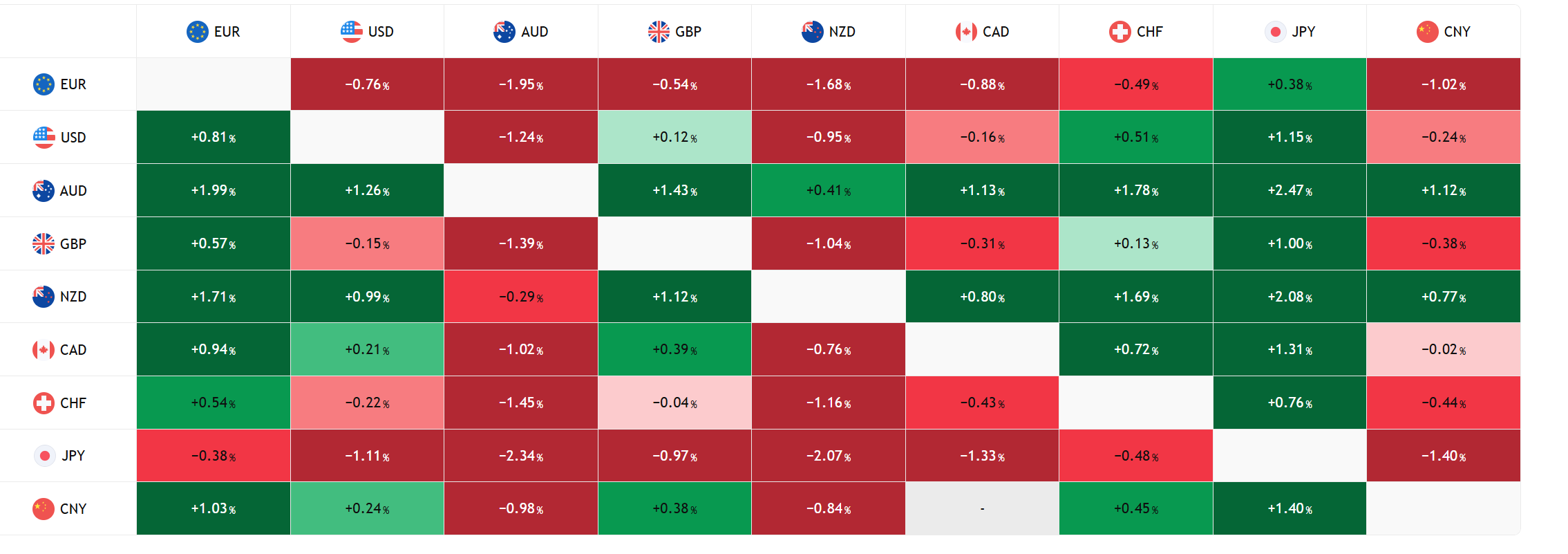

FX Heat Map (6:00 am) one week

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview