Agility Forex Daily

March 18, 2026

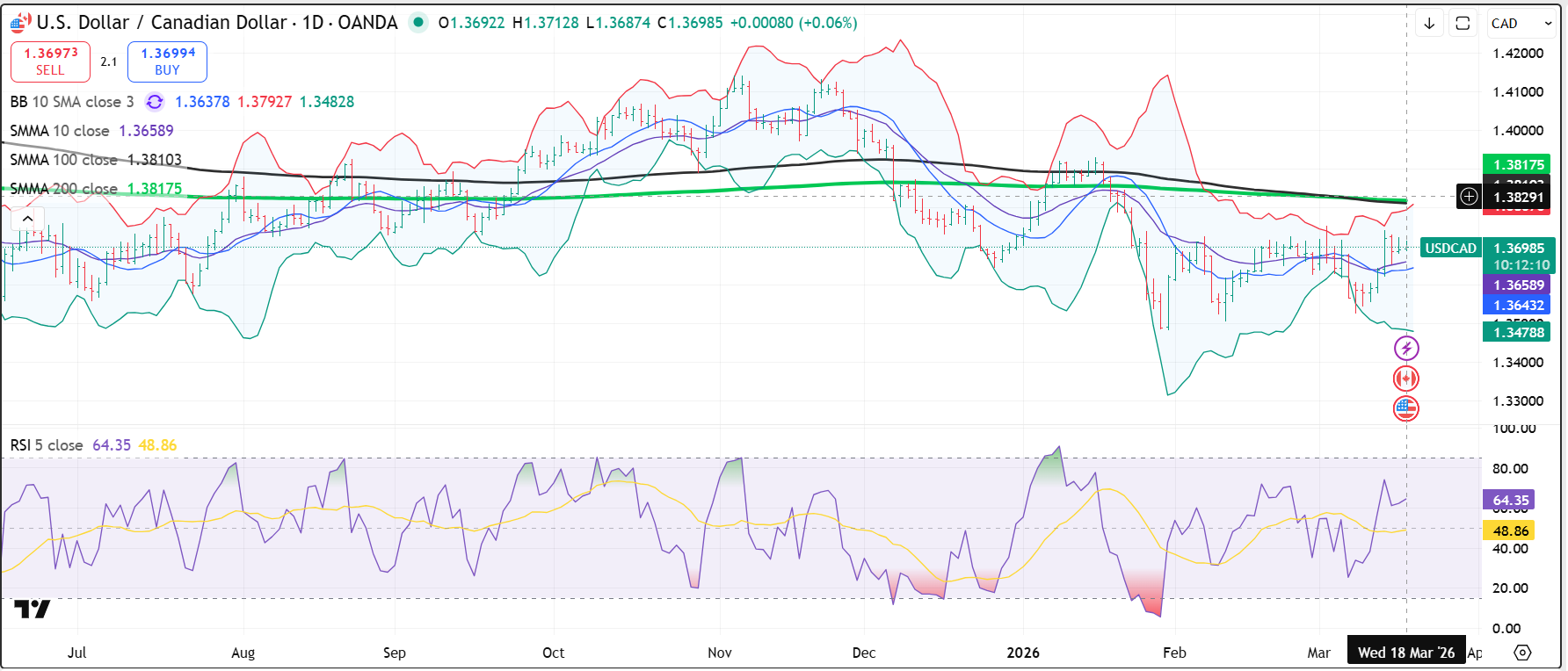

USDCAD open: 1.3698, overnight range 1.3687-1.3713, close 1.3691

USDCAD is steady ahead of the BoC and FOMC monetary policy meetings today.

The BoC is expected to leave rates unchanged and will add Trump’s Iran war to the list of reasons it uses to justify the stance. The most important reason is Governor Tiff Maclem’s claim from October 29, when he said that monetary policy had done all it can to stimulate growth, shifting the onus to the Federal government. Macklem noted that Trump’s tariff war meant that the economy was undergoing a long-term restructuring which cannot be addressed by monetary policy.

WTI oil traded in a 91.49-995.64 range with the low seen in Asia following the API report that US crude inventories rose by 6.6 million barrels last week. Additional selling pressure came after news that Iraq and Kurdistan reached a deal to restart an oil pipeline. However, it only adds 250,000b/d to the mix, which is a drop in the bucket for global supply. Ninety ships have transited the Strait of Hormuz since Trumps attack on Iran. It’s only closed to America and American allies shipping.

Today’s US data includes PPI and Factory orders.

USDCAD Technical Outlook

The intraday USDCAD technicals are mildly bullish while the short-term uptrend line near 1.3660 holds, with price bouncing off that area and pushing back toward the middle of the recent range. A move above 1.3730 would reopen a test of 1.3760. A break below 1.3660 would shift focus back to 1.3620 support.

The medium-term technicals suggest USDCAD remains modestly bid within the well-defined 1.3520–1.3760 range that has contained price action since late February. Momentum indicators are stabilizing, with RSI drifting higher, supporting a slight upside bias. A break above 1.3760 targets 1.3850, while a move below 1.3520 would expose 1.3460.

For today, USDCAD support is at 1.3660 and 1.3620. Resistance is at 1.3730 and 1.3760.

Today’s Range: 1.3650–1.3740

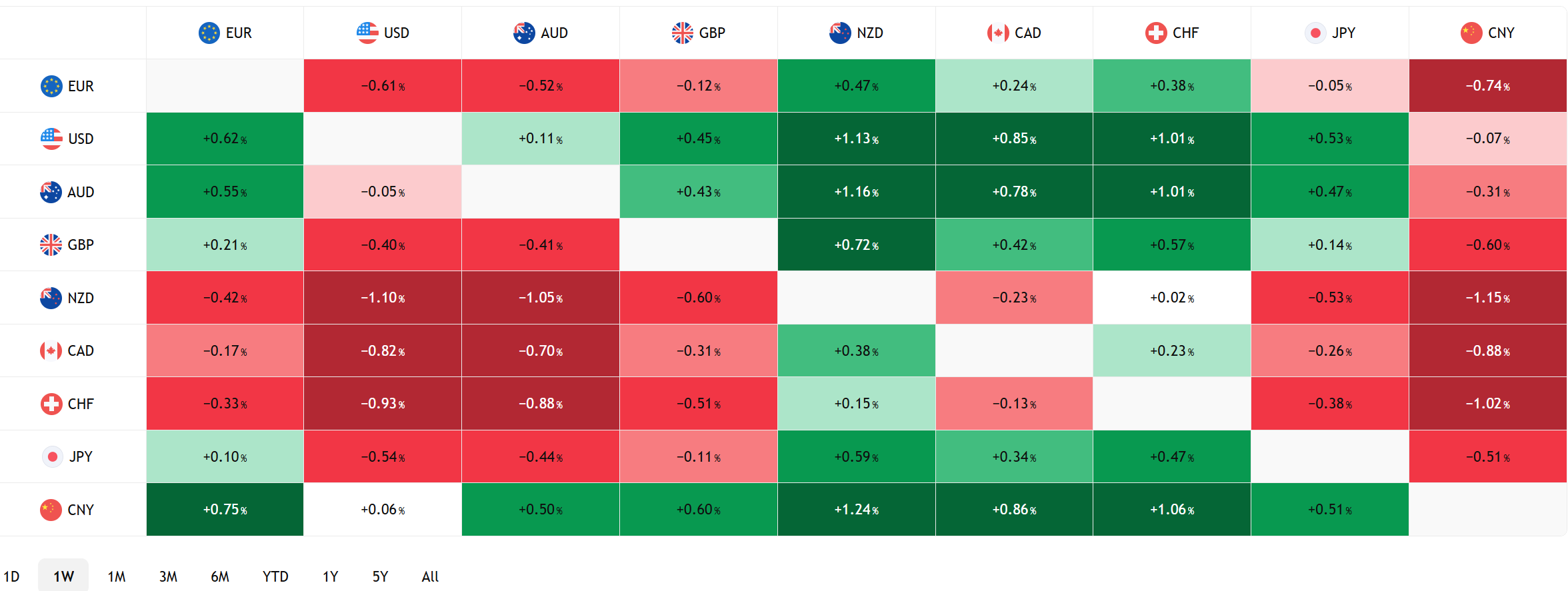

FX Heat Map (6:00 am) one week

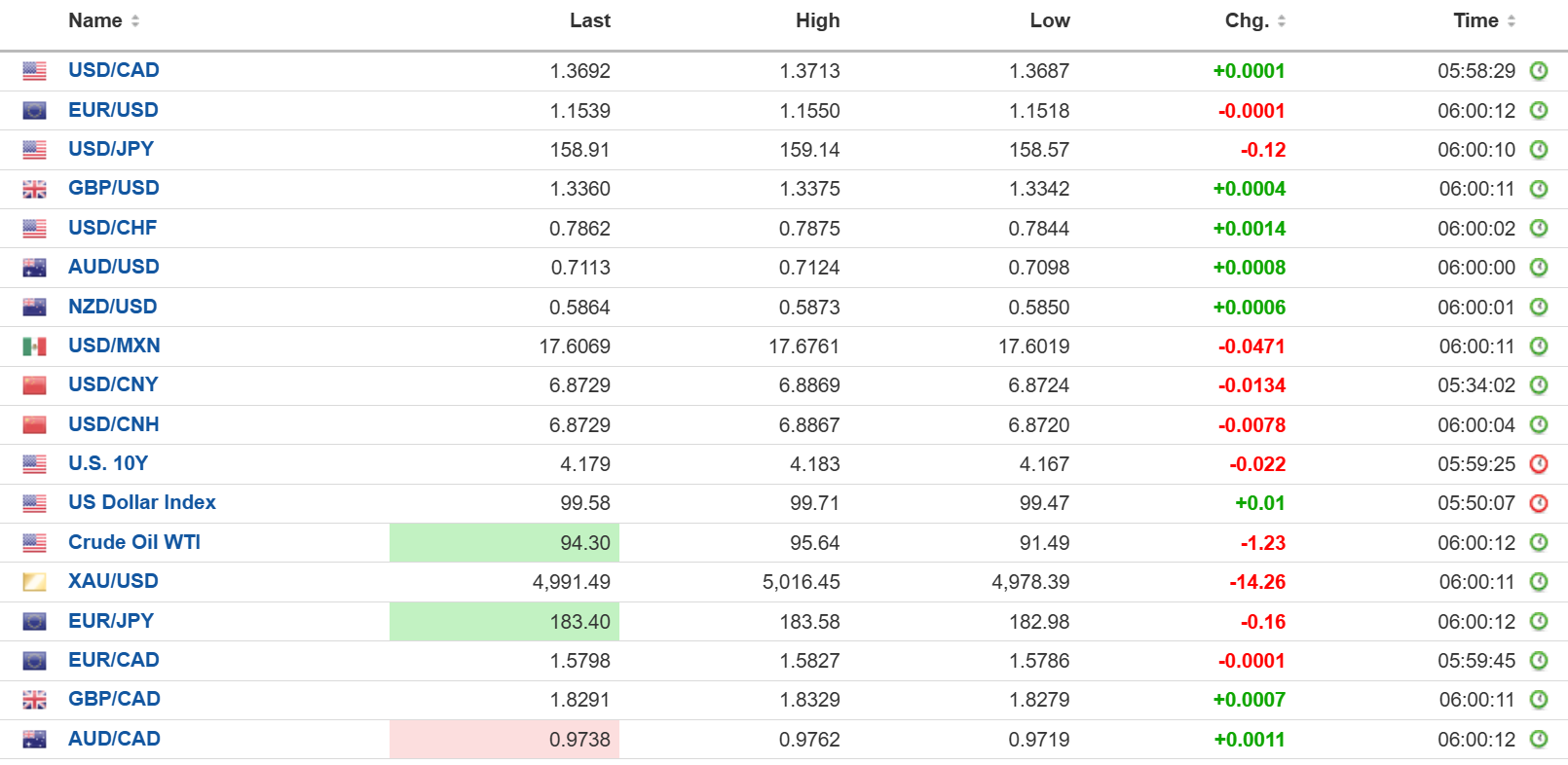

FX open high low 6:00 am

Fed Day

Trump’s attack on Iran blew away any sense of drama to today’s FOMC meeting. It’s not like there was much to blow away. The FOMC was universally expected to leave rates unchanged even before Trump unleashed his dogs of war. Since then, the oil price spike and supply chain disruptions have created global economic uncertainty, which gives policymakers an even better excuse to do nothing.

The risk from the FOMC meeting is if traders deem the statement and Powell’s press conference hawkish. If so, the greenback and Treasuries would rally, and stocks will come under pressure.

With a Little Help from My Friends

Trump sent out a call, then a demand for American allies to come to his aid to help open the Strait of Hormuz. They all wanted to help, except some were washing their hair, some were babysitting pets, while many others were rearranging sock drawers.

Trump was incensed, then boasted America didn’t need or desire any help, boasting that the “war was way ahead of schedule.” That was just before the Director of the National Counterterrorism Center, Joe Kent, resigned, saying “Iran posed no imminent threat to our nation, and it is clear that we started this war due to pressure from Israel and its powerful American lobby.”

White House Press Secretary Karoline Leavitt snapped, “It was Biden’s fault!” Actually, she said, “There are many false claims in this letter, but let me address one specifically: that ‘Iran posed no imminent threat to our nation.’ This is the same false claim that Democrats and some in the liberal media have been repeating over and over.”

Taking Stock

Asian equity traders followed Wall Street’s lead and bought stocks. Japan’s Topix surged 2.49% after getting an added lift from robust trade data. Australia’s ASX 200 rose 0.31%, and Hong Kong’s Hang Seng rose 0.61%.

As of 5:30 am PT, European bourses have flipped to negative from positive except for the French CAC 40 which is up 0.41%. The German DAX has fallen from 0.86% to -0.5%, and the UK FTSE 100 dropped to -0.14% from 0.31%. S&P 500 futures are flat, the US dollar index is 99.75%, the 10-year Treasury yield is 4.204%, and gold (XAUUSD) is $4,887.10.

EURUSD

EURUSD drifted sideways in a 1.1515-1.1550 range higher in a quiet session ahead of the FOMC meeting and tomorrow’s ECB meeting. The risk of a surge in Euro area inflation from spiking energy costs suggests the tone of the ECB statement will be neutral to hawkish. Harmonized Index of Consumer Prices (HICP) trickled down 0.1% m/m in February to 0.6% m/m but remained unchanged at 1.9% y/y.

GBPUSD

GBPUSD inched higher in a 1.3325-1.3375 band range, with prices supported by a dip in crude prices. UK pub-goers are facing higher prices. An insolvency expert warned that higher oil prices mean Brits will pay more when visiting their “local,” because breweries face higher production and distribution costs, and pub owners will pay more day-to-day expenses.

USDJPY

USDJPY bounced in a 158.57-159.29 band, with the low seen after Japan posted better-than-expected trade surplus numbers, helped by a 4.2% rise in exports in February. USDJPY was also pressured by lower oil prices. The BoJ is expected to leave rates unchanged tomorrow.

AUDUSD

AUDUSD traded sideways in a 0.7075-0.7124 range, with prices still underpinned by yesterday’s RBA rate hike (0.25% to 4.10%) and by its hawkish outlook.

USDMXN

USDMXN inched lower in a 17.6019-17.6761 range, with prices weighed down by modestly improved risk sentiment from lower oil prices. The peso is also underpinned by expectations that Banxico will continue to pause its easing cycle,

China

USDCNY Fix: 6.8909 vs exp. 6.8798 (Prev. 6.8961)

Shanghai Shenzhen CSI 300 rose 0.45% to 4,658.33

PBoC expected to leave monetary policy and rates unchanged at March 19 meeting.

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview