By Michael O’Neill

March Madness is synonymous with the NCAA men’s basketball tournament. It wasn’t always that way. The term was rather obscure until 1982, when CBS sportscaster Brent Musburger revived it during network coverage. Since then, March Madness has come to define bracket-busting chaos.

That is, until Operation Epic Fury.

The combined US and Israeli attack on Iran may have started at 1:15 am on February 28, but the madness did not end there. It has spilled into March with no buzzer-beater in sight. Instead of Cinderella stories, markets are dealing with shifting deadlines, contradictory headlines, and a geopolitical playbook that changes by the hour.

If the NCAA version is unpredictable, the Middle East version is untradeable in any conventional sense.

Safe Haven Fail

Operation Epic Fury may have been top secret, but there were plenty of signs that trouble was brewing. The US deployed a couple of aircraft carrier strike groups to the region as American officials were suddenly warning about increased nuclear risks and missiles that could strike America.

Traders got the message and scrambled into gold, taking the price from $4,526.50 at the beginning of February to $5,408.50 the day the attack was announced. But it didn’t last.

Gold prices plunged as central banks, fearing an inflation spike, turned hawkish. Traders did the math. If you hold a 10-year Treasury note in March 2026, you are locking in a yield of approximately 4.30%. If you hold gold, your yield is 0%.

Oil Barrels of Fun

Every day delivers a new twist. One moment, the US is threatening overwhelming force. The next, it is floating a 15-point peace plan. Iran denies talks even exist while continuing to strike targets. Washington deploys more troops while talking de-escalation. It is the geopolitical equivalent of betting the farm on the No. 1 seed Florida Gators and watching them get bounced by the second. The resulting market volatility is putting traders in neck braces.

Nowhere is that more obvious than in oil.

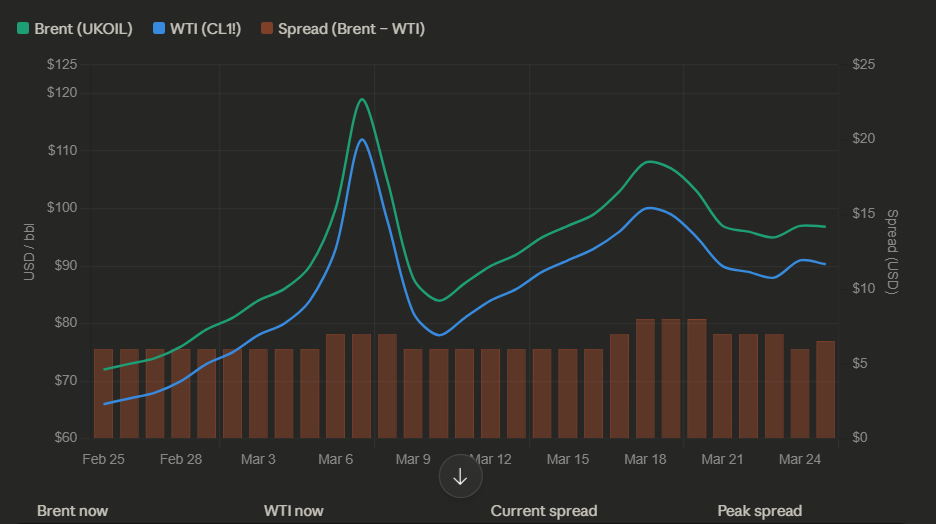

Brent, the global benchmark and the contract most exposed to Middle East supply, has been swinging like a screen door in a hurricane, trading in a $76.30–$118.27 range since the war began. WTI has been no calmer. Prices exploded from $67.03 to $119.48, triggered by strikes on Iranian energy infrastructure and retaliation targeting a Qatari LNG facility.

Then came the cavalry.

The International Energy Agency opened the taps, announcing a 400 million barrel emergency release. That headline alone knocked the froth off the rally, dragging WTI back toward the low $80s almost as quickly as it went up. At the same time, Washington even removed sanctions on Iranian oil already at sea (about 140 million barrels), allowing those barrels to flow back into the market and handing Iran a windfall in the process.

So here we are. Oil is now caught between two opposing forces. On one side, geopolitical risk is keeping a firm bid under prices. On the other, high interest rates and a strong US dollar are leaning against it, limiting how far the rally can extend. The Canadian dollar is caught in the middle.

Loonie on the Brink

The Iran war and the March surge in crude prices should have led to a surge in Canadian dollar demand. It didn’t.

A decade of aggressive anti-energy government policies left Canada sitting on $15.3 trillion (at $90/b) without the infrastructure to get it to market. The Canadian dollar may still get a bit of support from oil, but it’s Uncle Sam that derives the bigger benefit. Canada is shipping Western Canada Select at a 17% discount.

Canadian dollar gains are also hampered because the days of buying the Loonie as a proxy for the greenback are fading. Back in the day, periods of geopolitical strife had foreigners buying Canadian dollars instead of just US dollars because of Canada’s proximity to the US and its tightly linked trade relationship. No longer. President Trump’s aggressive trade policies have fractured the global and Canadian economies.

The Canada-US-Mexico Agreement renegotiations have begun, and even if the deal survives Trump, the odds are that Canada will be in a less favourable position.

The Canadian economy is struggling, unemployment is rising, and global risk aversion is fuelling US dollar demand. In this Middle East March Madness tournament, nobody wins, especially the Canadian dollar.