The Fed left rates unchanged. No one expected otherwise. For the statement, it was a different story. There were more than few market participants expecting that the statement following Wednesday’s Federal Open Market Committee meeting (FOMC) would contain a couple or more breadcrumbs that left a trail to a June rate hike. There were breadcrumbs but the trail they left went in circles.

The statement gave a nod to the hawkish camp with comments like “labour market conditions have risen further” and “real incomes have risen at a solid rate; consumer sentiment remains high”. Those two quotes are a tad more optimistic than what the FOMC wrote in March. The most hawkish change from the March statement was the removal of the line; “global economic and financial developments continue to pose risks”.

The statement gave a nod to the hawkish camp with comments like “labour market conditions have risen further” and “real incomes have risen at a solid rate; consumer sentiment remains high”. Those two quotes are a tad more optimistic than what the FOMC wrote in March. The most hawkish change from the March statement was the removal of the line; “global economic and financial developments continue to pose risks”.

But the doves were not to be denied. The statement noted that “growth in economic activity appears to have slowed, business and net exports have been soft. More telling was in the March statement; “Inflation picked up in recent months, however it has continued to run below the Committee’s 2% long run objective. Today’s statement said nothing about inflation picking up, just that it was running below the objective.

If you want to believe that an June rate hike is a possibility there is nothing in the statement that would dissuade you from that view. Conversely, if you think that the Fed will remain on the sidelines for longer, this statement won’t change your mind either.

The uncertainty surrounding the Fed rate hike debate will also impact the Canadian dollar. US economic data and comments from various Fed officials have contributed to short term USDCAD volatility for the past few months and today’s inconclusive FOMC statement will ensure that the pattern continues.

And if you are looking for relief from the Bank of Canada you may be out of luck. Stephen Poloz said yesterday, in New York, that Canadian rates weren’t going down, barring a “shock of some significance” and last week, in his testimony to the House of Commons Finance Committee implied that interest rates weren’t going up either. That puts the BoC on the shelf as a catalyst for the Canadian dollar, at least for the short term.

It also takes USDCAD direction out of the hands of the Fed and the BoC and puts it back into the hands of the market, particularly oil traders. And if recent oil price movements can be used as a guide, the Loonie may be in for a rough ride.

Oil prices rose on Wednesday in defiance of the Energy Information Administration’s report of another increase in Crude Stocks. Part of the move was attributed to general US dollar weakness because the Fed is on hold. What will happen to oil prices if the Fed turns hawkish?

Oil prices also rallied last week following the failure of the Doha, Qatar, Opec meeting to ratify a plan to cap or freeze production. Saudi Arabia wants no part of production freeze that doesn’t include arch rival, Iran. Iran, wants no part of an agreement that caps their production below pre-sanction levels.

Reuters reported on April 27, that Saudi Aramco made a rare sale of spot crude to an independent Chinese refinery which in the past, were typical Russian clients. The prospect of Russia, Iran and Saudi Arabia aggressively targeting each others markets doesn’t bode well for price increases especially if the OECD and IMF are correct and the global economy shrinks.

Opec engineered the oil market rebalancing initiative in November 2014 with the tacit goal of crippling US shale production. They have put a dent in that market but so far have only bruised the producers and according to Goldman Sachs analysts, the decline in US production is not enough to offset the supply growth from Iran.

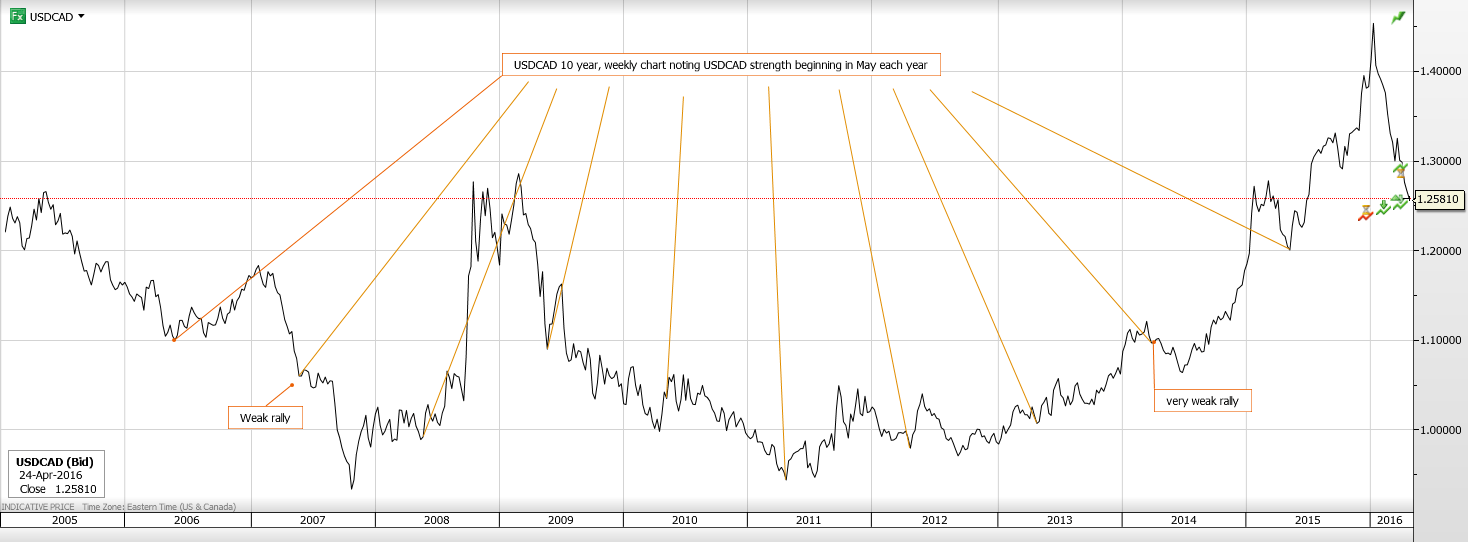

The Canadian dollar also has to contend with seasonal issues. USDCAD has rallied beginning in May since 2005 (although May 2007 and May2014 were very tiny moves). There is no reason to expect any different this May even though there isn’t any clear rationale for the moves.

The Seasonal effect should not be ignored- -USDCAD tends to rally beginning in May. Chart Source: Saxo Bank

The FOMC statement is consistent with what Janet Yellen has being saying all along. US interest rate increases are data dependent and although the data is improving steadily, it is not quite there yet. The March “dot-plot” still reflects the FOMC expectation of two rate hikes in 2016 which is will below what is priced in by the market.

The risk that renewed oversupply/lower demand oil price dynamics depress oil prices combined with a shift to hawkish rate hike expectations from outperforming US data and the Canadian dollar seasonal effect may drive USDCAD back to 1.3000 in the coming month.