April 16, 2026

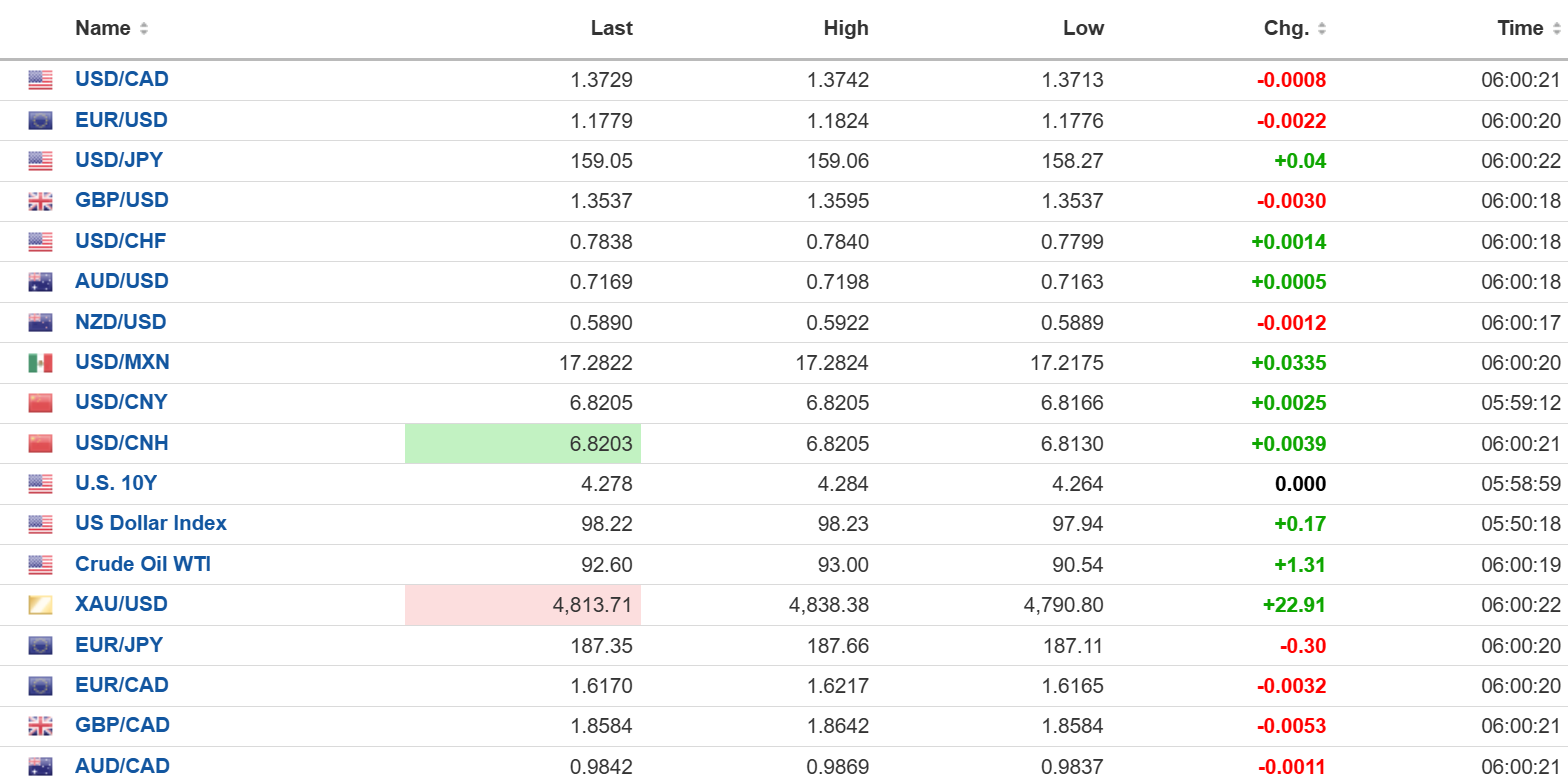

USDCAD open: 1.3729, overnight range 1.3713-1.3742, close 1.3743

USDCAD drifted lower on improved global risk sentiment. Israel and Lebanon are meeting today to discuss a ceasefire, which Iran claims was already part of the US/Iran ceasefire agreement. USDCAD direction is at the mercy of broad US dollar moves and oil prices, not domestic issues. However, with Mark Carney securing a majority government, fiscal stimulus from previously announced spending plans may give the Canadian dollar some support.

WTI oil prices traded in a 90.54-93.00 range. Traders are awaiting fresh news from ceasefire talks between the US and Iran and Israel and Lebanon. Despite claims to the contrary, very few ships are making the transit through the Strait of Hormuz. A move below $86.00 suggests further losses to $70.00.

US weekly jobless claims dropped by 11,000 to 207,000 a fresh indication that there is no reason for the Fed to cut interest rates because of the US employment situation. while the Philadelphia Fed Manufacturing Survey surprised to the upside at 26.7 in April which was far better than the March reading of 18.1 and well above the forecast of 10.

Capacity utilization and Industrial Production are on tap.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish below 1.3790 and looking for a break below 1.3710 to target 1.3660. A move above 1.3790 opens the door to 1.3820. The RSI is near 38, suggesting weak momentum with scope for further downside, although nearing oversold territory, which may limit follow-through.

The medium-term USDCAD outlook is neutral to bearish following repeated failures ahead of the 1.4000–1.4030 area and the recent rejection from the upper Bollinger Band (1.4032). USDCAD is trading below the 100 and 200-day moving averages at 1.3814–1.3819, which now act as resistance. The lower Bollinger Band at 1.3630 is the next key support, and a decisive break below that level would expose 1.3520.

For today, USDCAD support is at 1.3710 and 1.3670. Resistance is at 1.3770 and 1.3820.

Todays range 1.3690-1.3770

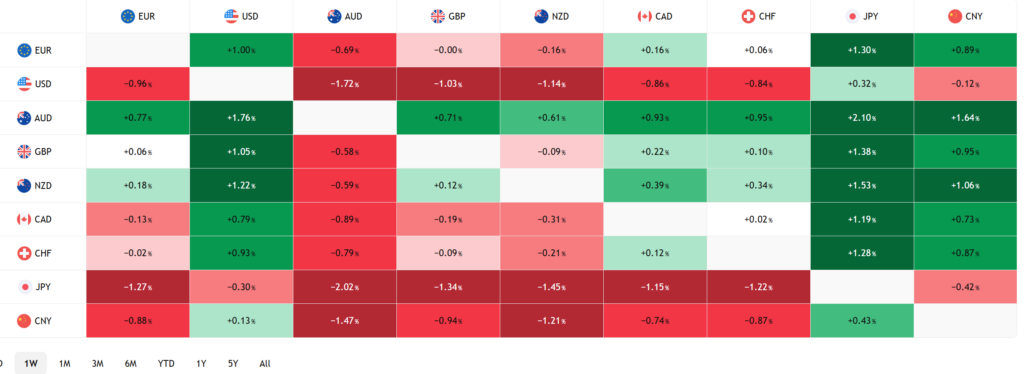

FX Heat Map (6:00 am) one week

FX open high low 6:00 am

Optimism is Prime

Global risk sentiment is positive on reports that the Israeli cabinet is discussing a ceasefire with Lebanon, and both sides are expected to meet today. Bloomberg reports that Iran and the US are discussing extending the ceasefire.

The war is over for everyone except the combatants. The S&P 500 and NASDAQ surged to new all-time highs yesterday, as did Japan’s Nikkei 225. The European bourses are shy of posting new record peaks but remain optimistic. Oil prices have receded from the March peak, but WTI is holding support above 90/b amid the number of ships transiting the Strait of Hormuz. FX traders are a tad more cautious. The US dollar index has recouped yesterday’s losses, although the trend is lower.

Taking Stock

Asian equities rallied, with Japan’s Topix gaining 1.17% and the Hong Kong Hang Seng rising 1.72%. Australia’s ASX 200 was the outlier, closing down 0.26%.

As of 5:30 am PT, European bourses are higher. The German DAX is up 0.63%, the French CAC 40 has gained 0.54% and UK FTSE 100 indice is up 0.62%. S&P 500 futures are up 0.13%, the 10-year Treasury yield is 4.273%, the DXY is 98.20, and gold (XAUUSD) is 4,814.27.

EURUSD

EURUSD is trading sideways in a 1.1775-1.1824 range. The single currency has recouped all its US/Iran war losses, but further gains may be difficult as expectations for the ECB to raise rates this month have evaporated. Eurozone inflation was a tad hotter than expected in March. HICP rose 2.6% y/y (forecast 2.5%) and 1.3% m/m (forecast 1.2%). The saving grace was that core HICP rose as expected and was unchanged from February. The EURUSD uptrend is intact while prices are above 1.1670.

GBPUSD

GBPUSD drifted in a 1.3533-1.3595 band, with prices above the pre-Iran/US war level. The currency did not get much support from UK GDP data, which rose 0.5% m/m in February, well above the forecast and the January result of 0.1% m/m, mainly because it was pre-war news. Higher than expected February Industrial Production (actual 0.5% m/m, forecast 0.2% m/m) was offset by weaker Manufacturing Production.

USDJPY

USDJPY traded in a 158.27-159.13 range and is at the top of the band in NY. The proximity to the 160.00 area has traders on alert for FX intervention, which could occur in concert with a BoJ rate hike on April 29, although that is a long shot. Elevated oil prices are supporting USDJPY.

AUDUSD

AUDUSD is consolidating yesterday’s gains in a 0.7163-0.7198 range. Prices are supported by better than expected Chinese data, hawkish expectations for the RBA, and fiscal stimulus after the government announced a boost to its defence spending.

USDMXN

USDMXN is trading defensively in a 17.2175-17.2874 band as prices head down to pre-US/Iran war levels due to broad-based US dollar weakness. US Treasury Secretary Bessent discussed the USMCA review with Mexican Finance Minister Edgar Zamora.

China

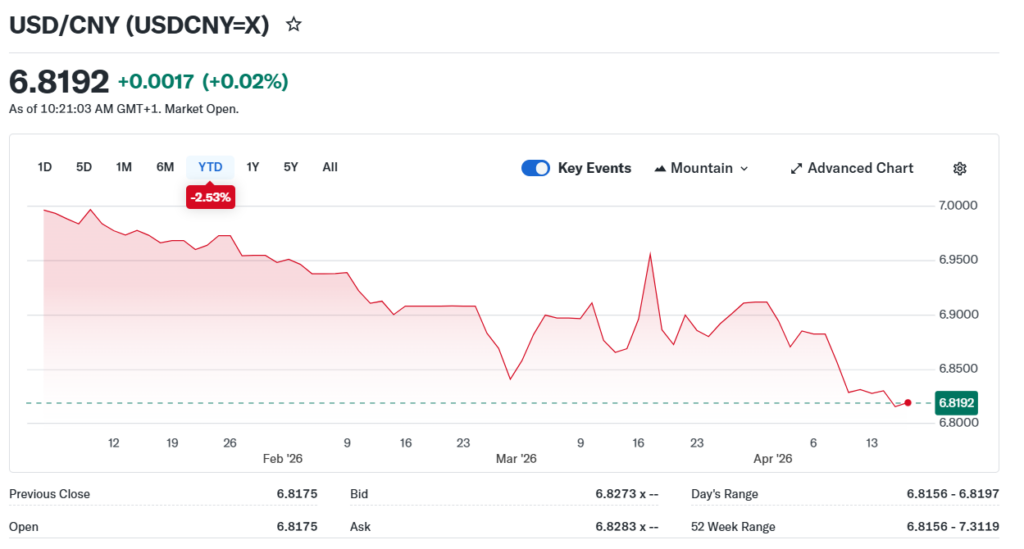

USDCNY Fix: 6.8616 vs exp. 6.8190 (Prev. 6.8582)

Shanghai Shenzhen CSI 300 rise 1.10% to 4,736.61

Annual Q1 GDP 5.0% y/y , forecast 4.8%, previous 4.5% y/y while Quarterly Q1 GDP 1.3% q/q as expected, previous 1.2%.

Retail Sales rose 1.7% y/y compared to the Jan/Feb reading of 2.8% which is what economists look at to minimize distortions from the Chinese New Year holidays.

Industrial Output rose 5.7% y/y in March, compared to the Jan/Feb gain

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview