April 30, 2026

USDCAD open: 1.3663, overnight range 1.3647-1.3691, close 1.3686

USDCAD traded choppily overnight. Yesterday, the Bank of Canada left rates unchanged at 2.25% and policymakers stressed about the uncertainty around their outlook. Governor Tiff Macklem seemed resigned to leaving interest rates unchanged for the rest of the year with the press conference opening statement noting “if the economy evolves broadly in line with the base case, changes in the policy rate can be expected to be small.”

Meanwhile, the Fed adopted a hawkish bias with three policymakers dissenting because they wanted to remove the reference to “an easing bias.”

WTI oil prices surged to 110.90 from 105.94 but have since retreated to 106.04 in NY. The rally is all Trump’s doing. He has thoroughly bungled his attack on Iran and is now begging the international community to help open the Strait of Hormuz. He is also exploring escalating the conflict by authorizing “new powerful strikes” targeting infrastructure.

Treasury Secretary Bessent said the US is ready to impose secondary sanctions on Iran oil buyers which is rather amusing since the Americans removed sanctions on some Iran sea borne crude earlier.

Canada February GDP rose 0.2% as expected and the same result is anticipated for March. The Loonie ignored the news,

There is a lot of US data on tap including weekly jobless claims, PCE-price index and Chicago PMI.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish below 1.3710, with the 100- and 200-day moving averages at 1.3800-1.3810 adding another layer of resistance. The momentum indicators are neutral.

The longer-term USDCAD technicals remain bearish below the 100 and 200-day moving averages and looking for a test of support at 1.3600.

For today, USDCAD support is at 1.3640 and 1.3590. Resistance is at 1.3700 and 1.3720. Today’s range: 1.3600-1.3700.

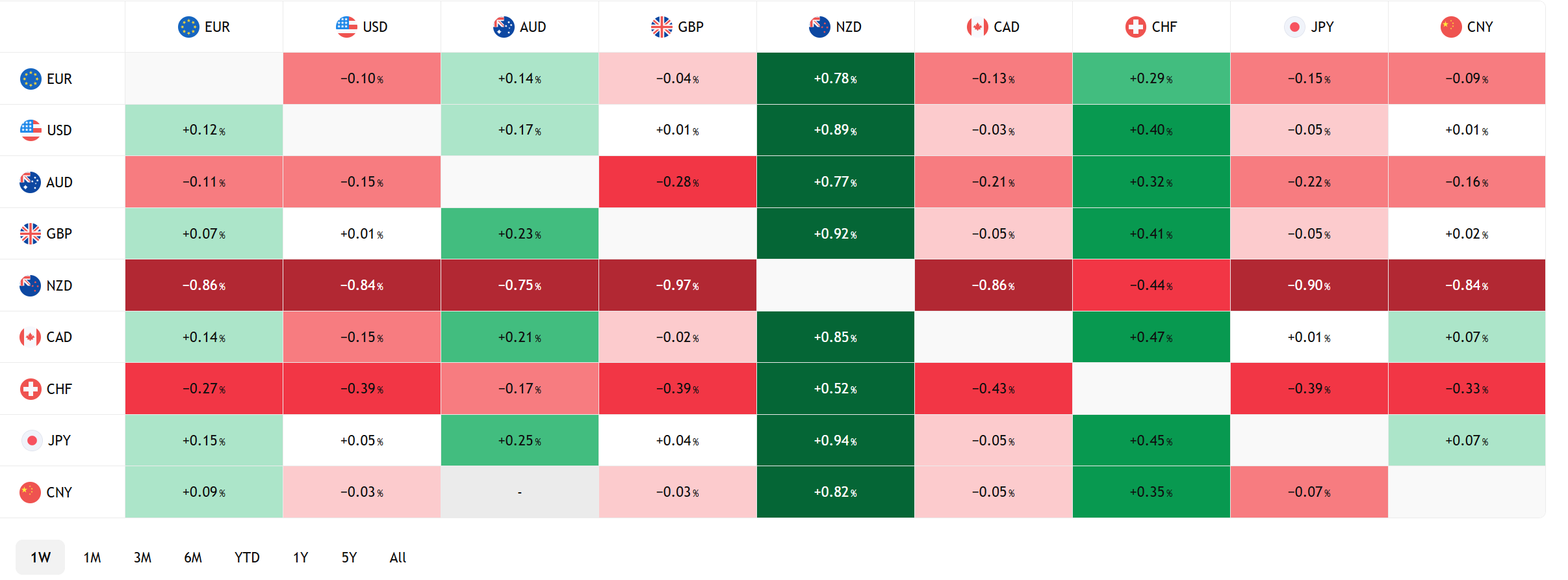

FX Heat Map (6:00 am) one week

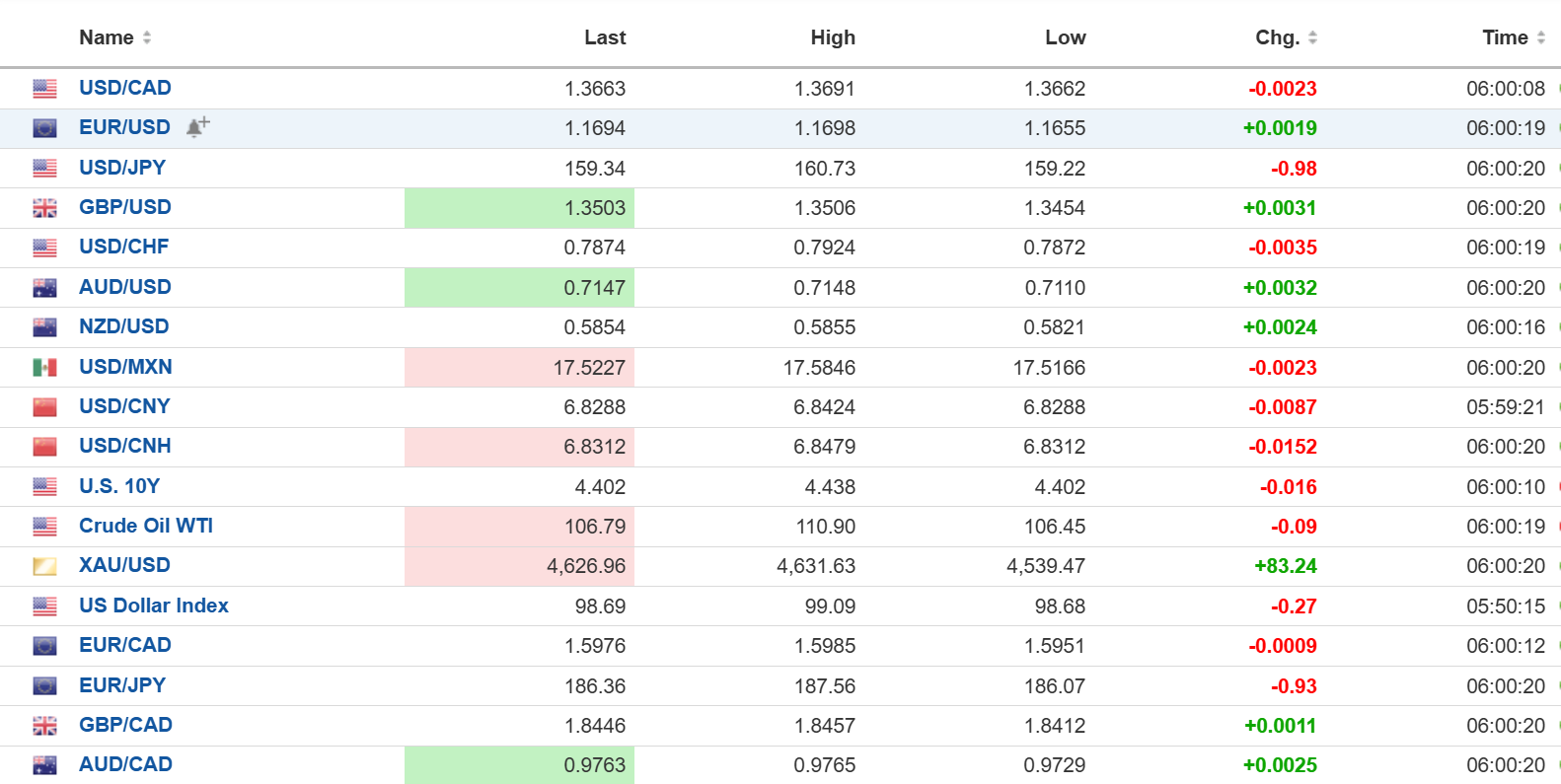

FX open high low 6:00 am

Robust Data Supports Fed

US weekly jobless claims rose just 189,000 compared to expectations for a 215,000 increase while the Employment Cost index rose 0.9% (forecast 0.8%). Meanwhile Core PCE Price index rose 3.2% as expected. US GDP rose 2.0% rather than the 2.3% predicted.

All in all, the data points to a healthy economy albeit one with rising price pressures which supports yesterdays FOMC decision to leave rates unchanged at 3.75%. It all appears to vinicate the three voting meembers who dissented because they want the statement to drop the language of an easing bias.

Taking Stock

Asian equities closed in the red. Australia’s ASX 200 fell 0.24%, Hong Kong’s Hang Seng fell 1.28% and Japan’s Topix fell 1.19%. All three indices finished April with gains led by a 6.56% rise in the Topix, a 4.05% jump in the Hang Seng and a 2.19% gain in the ASX 200.

As of 5:40 am PT, European bourses are rallying. The UK FTSE 100 has gained 1.59% while the German DAX is up 0.95% and the French CAC 40 has gained 0.10%. S&P 500 futures are up 0.46%, the 10-year Treasury yield is 4.40%, the DXY is 98.44, and gold (XAUUSD) is 4,629.72.

EURUSD | Range: 1.1655-1.1720

EURUSD traded poorly post-FOMC but it is rebounded to the peak after the ECB left rates unchanged then warned that the longer the Iran war lasted and the longer that energy prices remained elevated means a stronger impact on inflation and the economy is likely. The ECB is expected to hike rates three times before year end. Today, German Q1 GDP rose 0.3% q/q but that good news was offset by weak Eurozone GDP and higher inflation.

GBPUSD | Range: 1.3495-1.3535

GBPUSD mirrored EURUSD gains overnight an popped after the Bank of England left rates unchanged but warned of possible rate hiles later this year. Meanwhile UK politicians are stirring the pot. Manchester Mayor Andy Burnham, a rival to Prime Minister Starmer, opined about exempting defence spending from fiscal rules.

USDJPY | Range: 158.02-160.73

USDJPY plunged following a likely bout of Bank of Japan intervention which authorities have not confirmed. Even so, the time was ripe. The Fed is hawkish, the BoJ is on hold and short yen positions were extreme. Furthermore, officials have increased their warnings about such action this week. That does not mean it is safe to sell USDJPY — far from it. US and Japan interest rate spreads favour the US and oil prices have surged.

AUDUSD | Range: 0.7110-0.7158

AUDUSD is recouping yesterday’s FOMC losses following good PMI numbers from China and an expected RBA rate hike next week.

USDMXN | Range: 17.5150-17.5848

USDMXN rallied yesterday and consolidated the gains overnight. Contrasting central bank outlooks fuelled the gains. The Fed appears to have a hawkish bias while Banxico may cut rates by 25 bps to 6.45% next week. Mexican Q1 GDP is expected at 0.8% y/y compared to 1.8% previously.

China

USDCNY Fix: 6.8628 (Prev. 6.8608)

Shanghai Shenzhen CSI 300 rose 1.10% to 4,807.31

RatingDog April Manufacturing PMI52.2 (forecast 50.9, March 50.8) The expansion is the fastest since December 2020 and due to stronger output and rising new orders.

The NBS April Manufacturing PMI was 50.3 (forecast 50.2, April 50.4), Non-Manufacturing PMI 49.4 (forecast 49.9, April 50.1)

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview