May 22, 2026

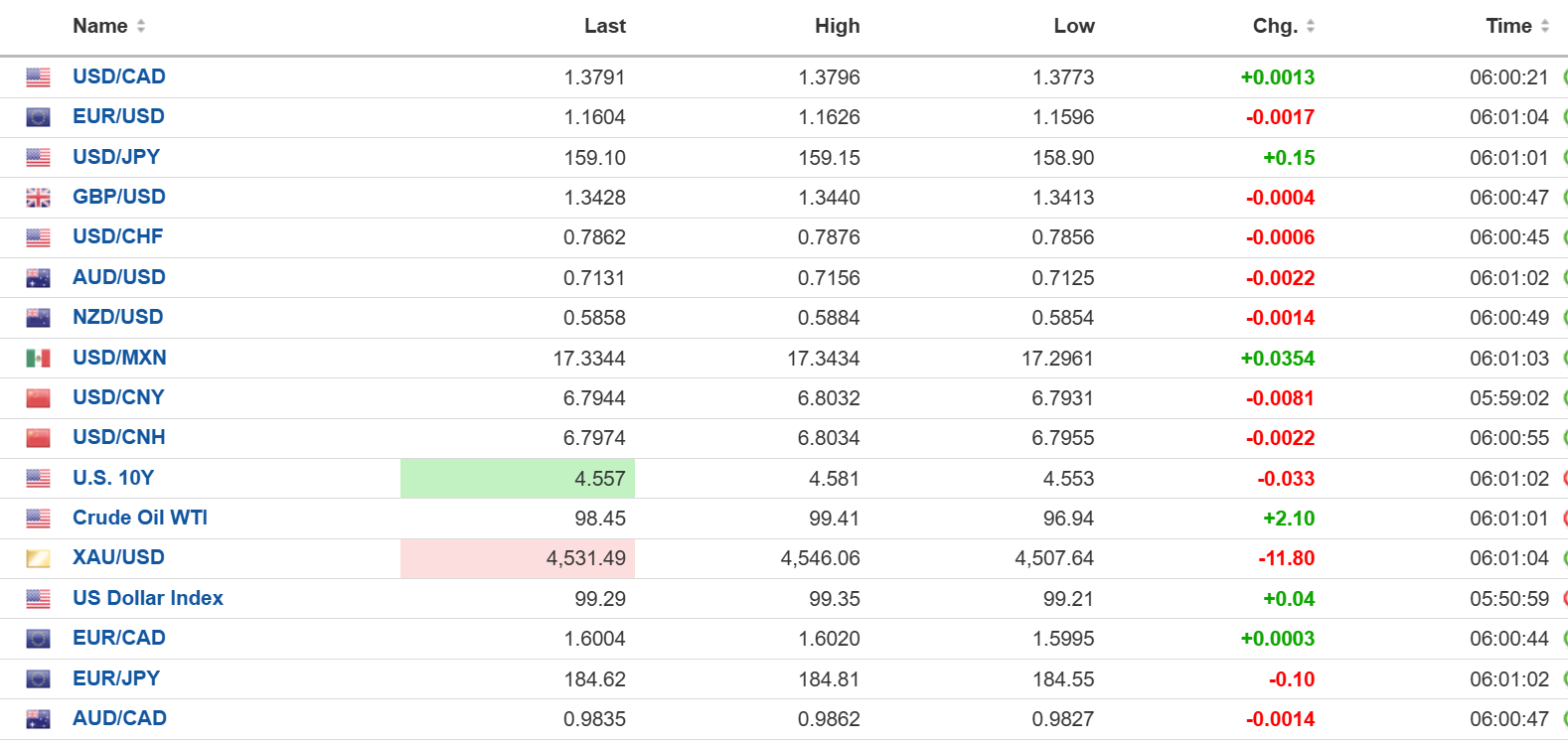

USDCAD open: 1.3791, overnight range 1.3773-1.3807, close 1.3780

NOTE: There will not be an Agility Forex Daily on Monday due to the US and UK holidays.

USDCAD is drifting higher on the back of broad-based US dollar demand ahead of the US and UK long weekends on concerns that renewed US/Iran hostilities could resurface. It is a greenback driven move and supported by the lingering impact of the hawkishly biased-FOMC minutes. However, USDCAD is also flirting with a significant resistance zone and the RSI suggests it is extremely overbought, which suggests prices will struggle to rally above 1.3820, today.

Canada’s March retail sales headline gain of 0.9% masked a much weaker underlying picture. The entire increase was driven by gasoline stations and fuel vendors, which surged 12.4% on Middle East supply disruptions. Excluding fuel, core retail sales slipped 0.1%, while sales volumes fell 0.7%, highlighting that Canadians are paying more but buying less. Weakness in building materials, general merchandise, and motor vehicles points to a consumer under growing pressure.

Meanwhile, inflation pressures continue to intensify. Canada’s Industrial Product Price Index rose 11.4% y/y in April while the Raw Materials Price Index jumped 31.6%, fuelled by soaring energy costs linked to disruptions in the Strait of Hormuz. Chemical prices posted their biggest monthly increase since 1981, while grain and oilseed prices hit record gains. The combination of weakening consumption and rising inflation suggests stagflation risks are no longer theoretical, complicating the Bank of Canada’s policy outlook and limiting support for the Canadian dollar.

WTI oil prices dropped from 102.82 yesterday to 95.74 on optimism that Iran and the US would reach a deal. Oil traded in a 95.74-99.41 range overnight. At the moment the sticking point is Iran’s enriched-uranium stockpile. The US wants it and Iran says no.

US Michigan Consumer Sentiment is expected to be 48.2, unchanged from last month.

USDCAD Technical Outlook

The intraday technicals are bullish while above 1.3770 and looking to break above 1.3810 to test resistance in the 1.3840 area. A failure to hold 1.3770 targets 1.3710. However, the short term RSI is at extreme overbought levels which suggests gains above 1.3810 will be hard to sustain and prices will retest support in the 1.3760 area.

The daily technicals are bullish above the 100 SMA at 1.3724, but the 200 SMA at 1.3814 is capping the upside. Daily RSI at 89.79 is well above the extreme overbought threshold of 85 and is warning that USDCAD is stretched. The MACD is positive but the histogram is turning negative, suggesting the bullish momentum is fading.

For today, USDCAD support is at 1.3770 and 1.3740. Resistance is at 1.3820 and 1.3850. Today’s range: 1.3760-1.3820.

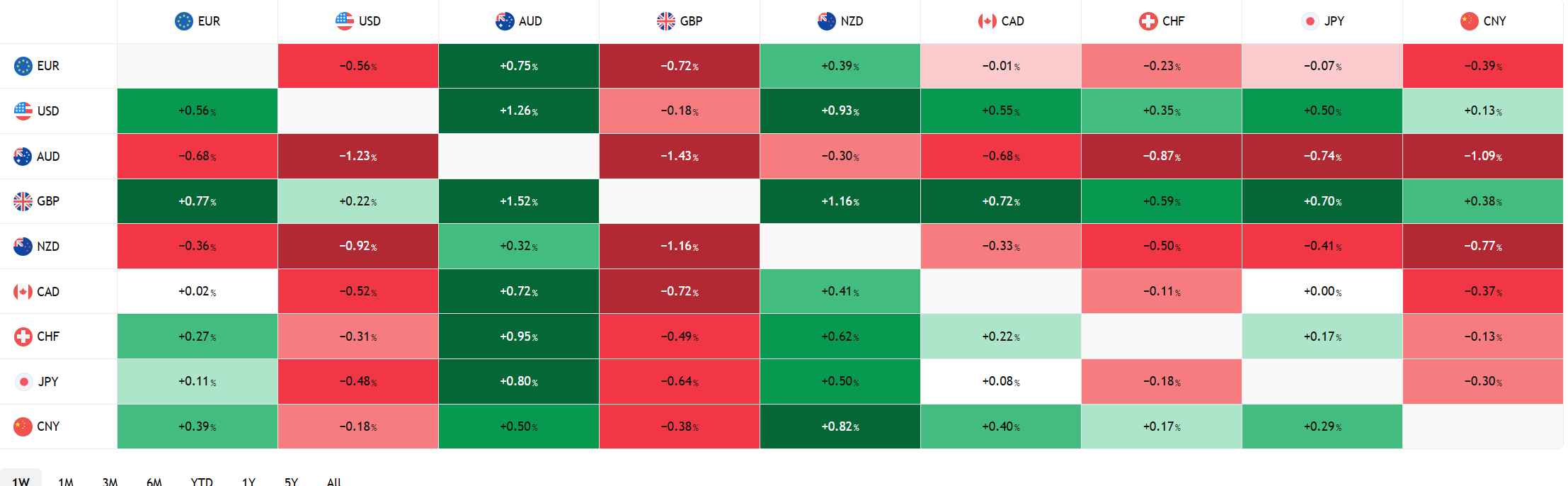

FX Heat FX open high low 6:00 am

FX open high low 6:00 am

Long weekend looming for US and UK

US and UK markets are closed Monday for holidays, and that is setting the tone for today’s trading session as many investors look to get an early start on the long weekend. In addition, ongoing caution surrounding the US-Iran conflict, fuelled by a barrage of contradictory statements from various officials, is likely to keep traders on the sidelines.

Kevin Warsh is being sworn in as Fed Chair today. Trump selected him in the hope of lower US interest rates, but many FOMC members continue to warn that tariffs and geopolitical tensions tied to the Iran conflict risk adding fresh inflation pressures. Yesterday, Chicago Fed President Austan Goolsbee said, “We have a pretty significant inflation problem developing.”

Last week, Trump ordered the withdrawal of 5,000 US troops from Poland in what many viewed as a tacit swipe at NATO. Yesterday, he reversed course and ordered 5,000 troops deployed to Poland following the election of Trump ally Karol Nawrocki. Bipoland or bipolar?

Taking Stock

Asian equities indexes closed higher on hopes for a US/Iran peace deal. Japan’s Topix rallied 1.00%, Australia’s ASX 200 climbed by 0.41% and Hong Kong’s Hang Seng rose 0.86%.

As of 5:40 am PT, the German DAX is up 1.09%, the French CAC 40 has gained 0.70% and the UK FTSE 100 has risen 0.32%. S&P 500 futures are up 0.38%, the 10-year Treasury yield is 4.551%, DXY is 99.33 and gold (XAUUSD) is 4,51800

EURUSD | Range: 1.1596-1.1626

EURUSD drifted lower in an uneventful session, with modestly better German Q1 GDP and Ifo data failing to move the needle. The recent run of soft Eurozone PMI data, coupled with firmer inflation, has fuelled stagflation concerns that could hamper the ECB’s ability to raise interest rates. EURUSD technicals remain bearish below 1.1770, with additional resistance at 1.1670. A break beneath 1.1570 would put 1.1500 in play.

GBPUSD | Range: 1.3413-1.3440

GBPUSD drifted quietly, with traders largely ignoring a modest improvement in the GfK consumer confidence index, which came in at -23 compared with expectations of -28 and the previous month’s -25 reading. Retail sales rose 1.1%, missing forecasts for a 1.5% gain, underscoring the underlying weakness in the economy and weighing on the currency.

USDJPY | Range: 158.90-159.15

USDJPY spent another session moribund as firm US treasury yields and the threat of intervention trapped the currency pair in a tight band. Japanese inflation, ex fresh food rose 1.4% rather than the 1.7% expected and 1.8% seen in March. The data reduces the urgency for the BoJ to raise rates.

AUDUSD | Range: 0.7125-0.7158

AUDUSD traded defensively in a tight range but the this week’s uptrend remains intact. The hawkish tilt to the FOMC minutes and the belief that the RBA is pausing it tightening cycle is capping the upside for now.

USDMXN | Range: 17.2961-17.3439

USDMXN traded sideways, with price action closely tracking shifts in risk sentiment surrounding the US-Iran conflict. Mexican Q1 GDP was -0.6% q/q a tad better than the -0.8% expected. Inflation fell 0.16% in the first half of May. The results justify the minutes from the May 7 Banxico policy meeting noting the rate-cutting cycle is over, with policymakers noting that “it will be appropriate to maintain the reference rate at its current level” for the foreseeable future. That sentence suggests that todays Mexican CPI numbers will be ignored.

CHINA

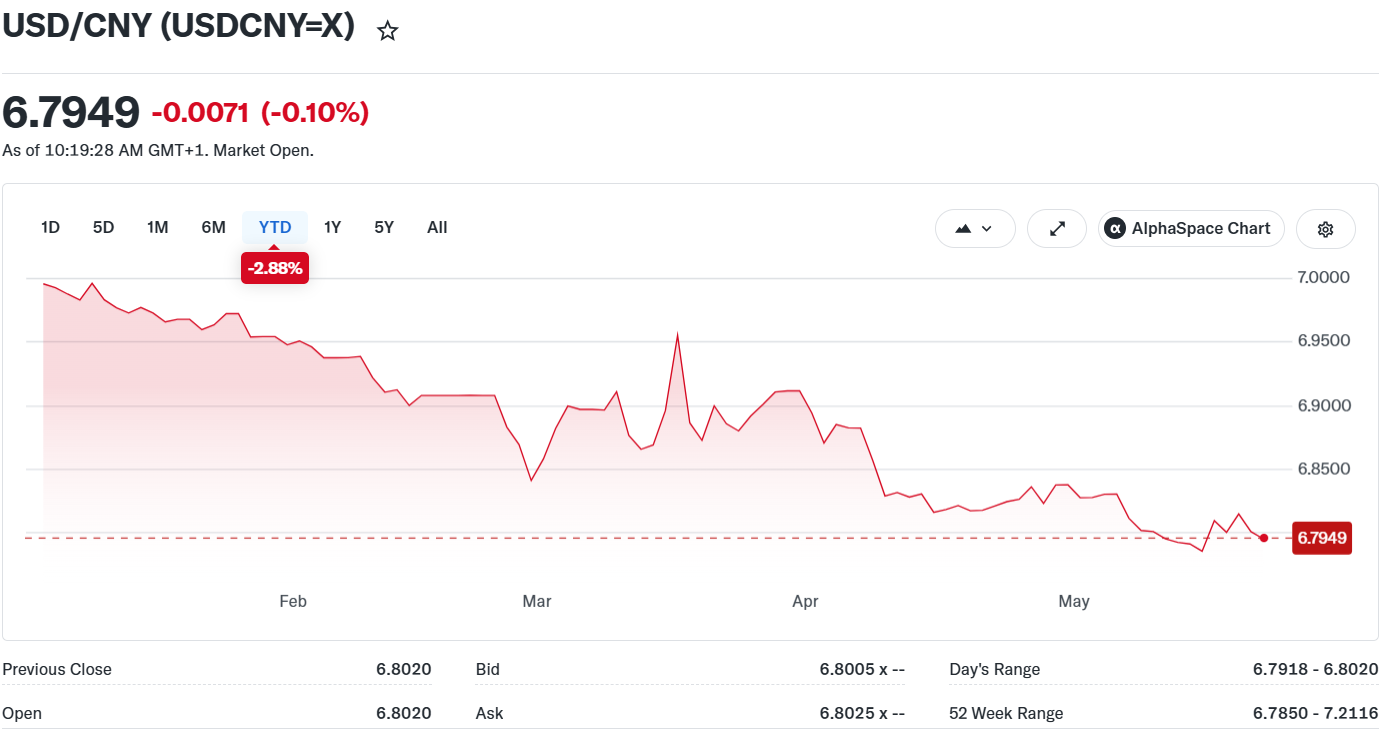

- USDCNY Fix: 6.8373 vs exp. 6.7922 (prev. 6.8349)

- Shanghai Shenzhen CSI 300 rose 1.30% to 4,845.10

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview