June 24, 2026

USDCAD open: 1.4233, overnight range 1.4205-1.4241, close 1.4212

USDCAD continued its march upward powered by broad-based US dollar demand because analysts believe the Fed will raise rates in September. The latest tech stock sell-off added fuel to the fire with investors fearing a “dotcom” style bubble and buying greenbacks.

Yesterday’s comments by BoC Governor Tiff Mackelm didn’t help sentiment. He warned that global economic imbalances were driving overinvestment into the US which creates global financial risks.

The lack of progress in USMCA trade talks and Trump’s open hostility towards Canada are other factors fueling the negative Canadian dollar bias.

WTI oil traded in a 71.56-73.17 range and is near the overnight low. Qatar aid its LNG shipments may return to normal in a few weeks. Meanwhile, 23 ships are making the transit through the Strait of Hormuz and 23 others have completed it, in the past 24 hours.

There are no Canadian economic reports on tap. The US releases New Homes Sales Change data fro May which is hardly a market mover.

USDCAD Technical Outlook

The intraday chart is bullish following the break above 1.4150, with USDCAD trading near 1.4230 and hugging the upper Bollinger Band on both the 1-hour and 4-hour charts. The 1-hour MACD and RSI confirm positive momentum. A sustained break above 1.4240 would target 1.4280 initially, followed by the major resistance zone at 1.4350.

In the short term, the rally from the May lows remains intact and has accelerated following the breakout through the 1.4000 and 1.4150 resistance zones. Prices are now testing levels last seen in early April 2025, with the next major upside target located near 1.4280 and then 1.4350.

The daily MACD continues to strengthen and confirms the underlying uptrend. However, the daily RSI is at an exceptionally overbought reading that is rarely sustained for long periods.

For today: USDCAD support is at 1.4190 and 1.4130. Resistance is at 1.4280 and 1.4350. Today’s expected range is 1.4180-1.4270.

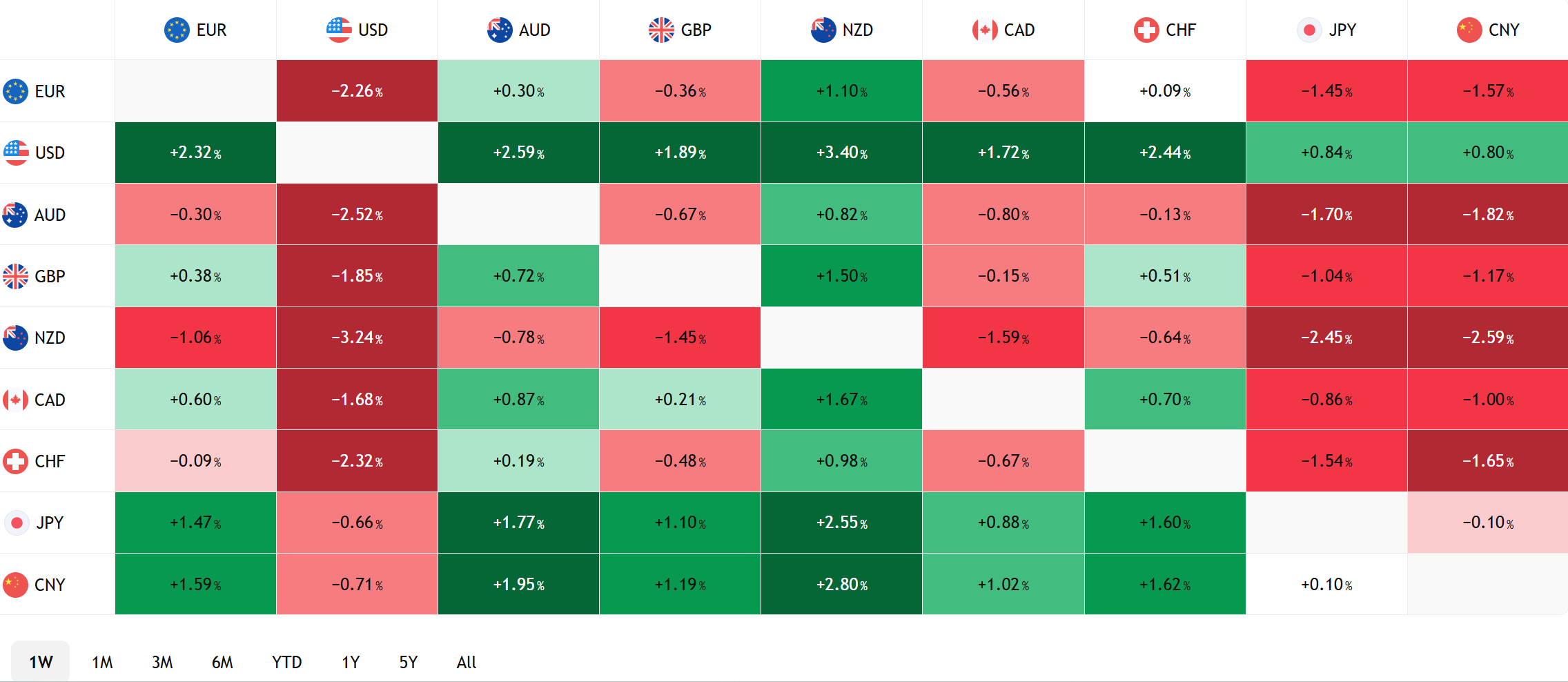

FX Heat Map

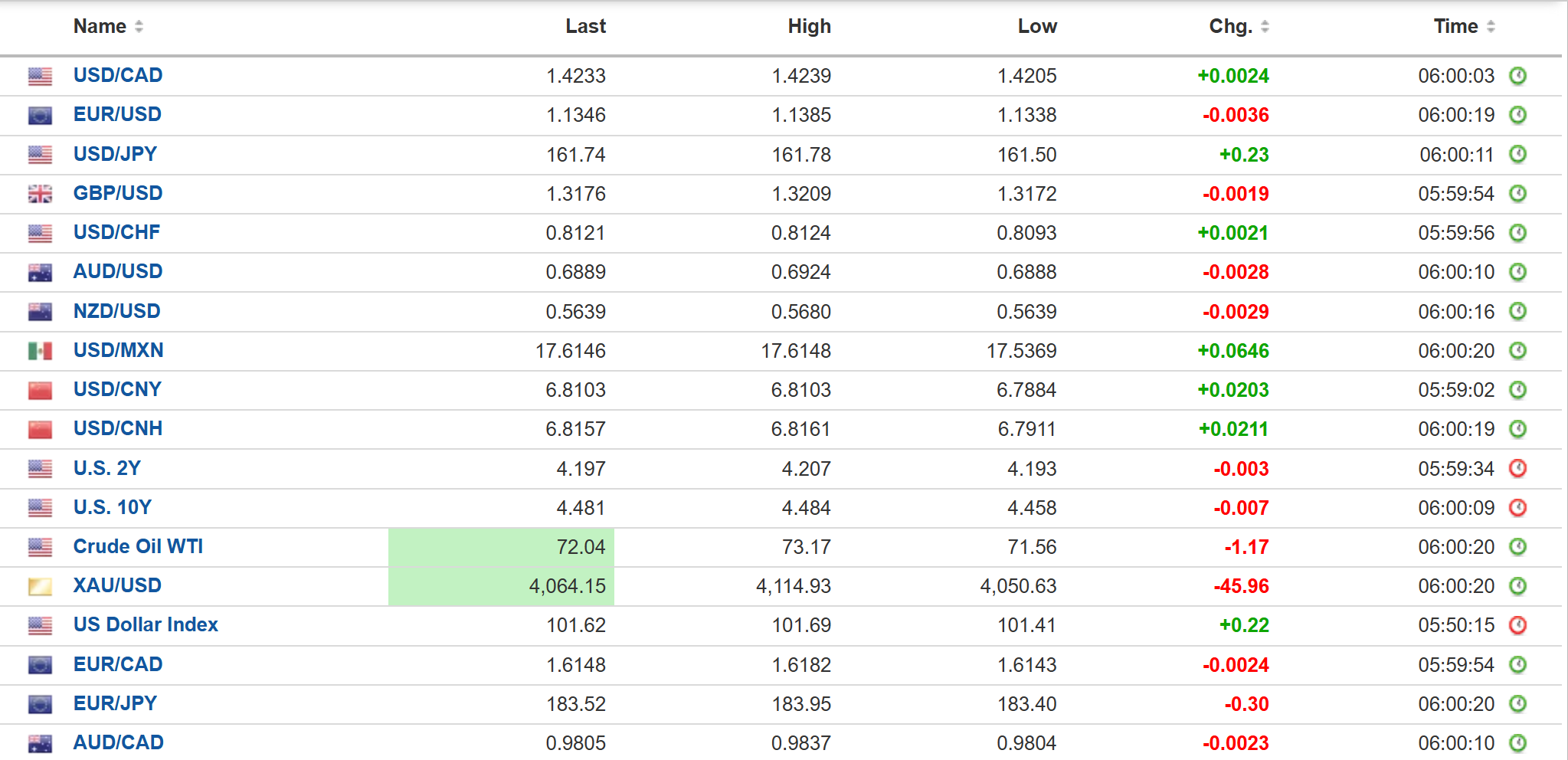

FX open high low 6:00 am

Equity Traders Declare Risk-off

Wall Street plunged yesterday and it dragged many overseas markets down with them. Tech stocks were hammered over fears that the recent massive AI gains may be overdone. Veteran equity traders were having flashbacks to the Dotcom bust when the NASDAQ lost 77% between March 10, 2000 and October 9, 2002, as the AI gains and Dotcom era shared similar characteristics.

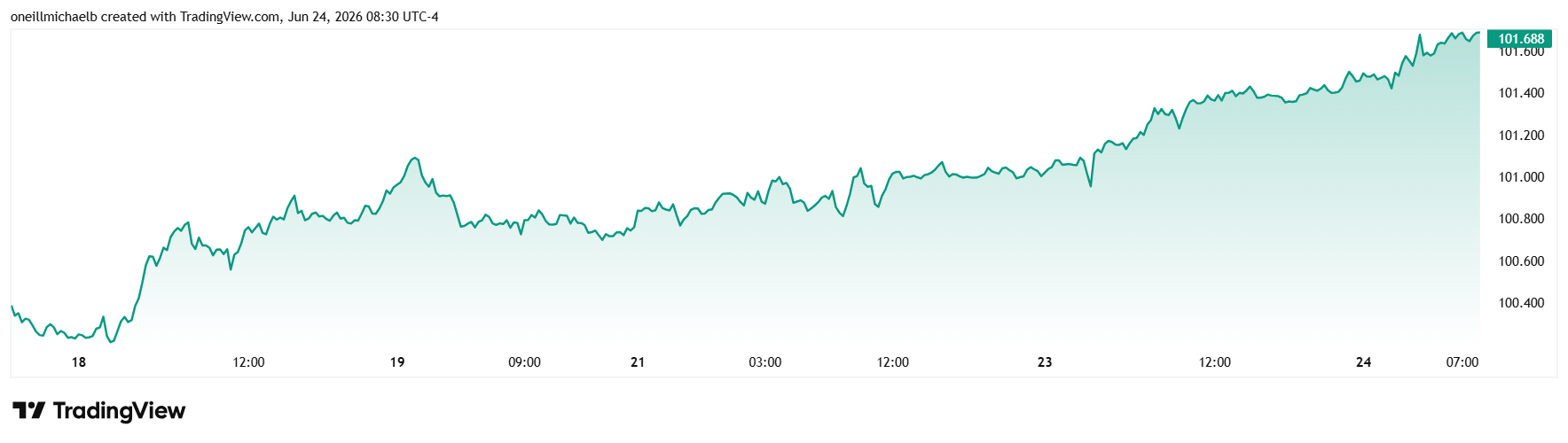

The equity rout combined with expectations that the Fed will hike rates in September, powered the US dollar index higher, rising 0.30% overnight and 0.87% in the past five days.

Iran and US Arguing About What Has Been Agreed

The US and Iran have agreed to end their war and, according to Trump, they are doing quite well regarding Iran while they are trying to work out a deal that is fair. Trump said there are scheduled IAEA nuclear inspections and Iran said “not so.” Trump got a rebuke when the US Senate passed a resolution (50-48) to halt the war in Iran unless Trump gets approval from Congress. The White House decided that the resolution is non-binding.

Taking Stock

Asian equities closed with Japan’s Topix falling 0.67%, while Australia’s ASX 200 rose 0.24% and Hong Kong’s Hang Seng Index gaining 0.33%.

As of 5:30 am PT, European bourses are flat to mixed. The German Dax has dropped 0.85%, the French CAC 40 is up 0.43% and the UK FTSE 100 has gained 0.14%. S&P 500 futures are up 0.36%, the 10-year Treasury yield is 4.443%, the DXY is 101.69, and gold (XAUUSD) is 4,018.89.

EURUSD | Range 1.1330-1.1385

EURUSD continued to slide due to equity market jitters fueling safe haven demand for US dollars while being undermined by bearish technicals. The break below 1.1370, last seen in April 2025 targets further losses to 1.1210. Yesterday’s hawkish comments from ECB Chief Economist Philip Lane suggesting inflation would be above 2.0% for some time, had little effect.

GBPUSD | Range 1.3148-1.3209

GBPUSD is suffering from the double whammy of political uncertainty, yesterday’s disappointing services and composite PMI data and broad-based demand for US dollars. The drop could have been worse but GBP rose against the euro. The technicals warn that a decisive move below 1.3150 would extend losses to 1.3050.

USDJPY | Range 161.50-161.78

USDJPY traded sideways and steady US Treasury yields and broad-based US dollar demand were largely offset by the release of rather hawkish BoJ minutes from the June 16 meeting. The BoJ hiked rates to 1.0% at that meeting and one member argued for a rate increase every few months.

AUDUSD | Range 0.6824-0.6924

Aussie is trading at its overnight session low in NY due to the global equity market sell-off and following a mixed inflation report. Headline CPI rose 4.0% y/y in June, below the 4.4% expected and 4.2% in May. However, trimmed mean CPI rose 3.6%. The results should keep the RBA sidelined for the near term.

USDMXN | Range 17.5369-17.6530

USDMXN continues to climb in the wake of expectations for the Fed to raise rates in September and the rally is exacerbated by safe-haven demand for greenbacks due to the tech stock sell-off. USDMXN is seeing lingering support from the ongoing USMCA talks and from expectations for Banxico to leave rates unchanged at tomorrow’s meeting.

CHINA

- PBoC Fix: 6.8195 vs exp. 6.7913 (prev. 6.8171)).

- Shanghai Shenzhen CSI 300 FELL 2.77% to 4,919.39

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics Tradingview