July 14, 2025

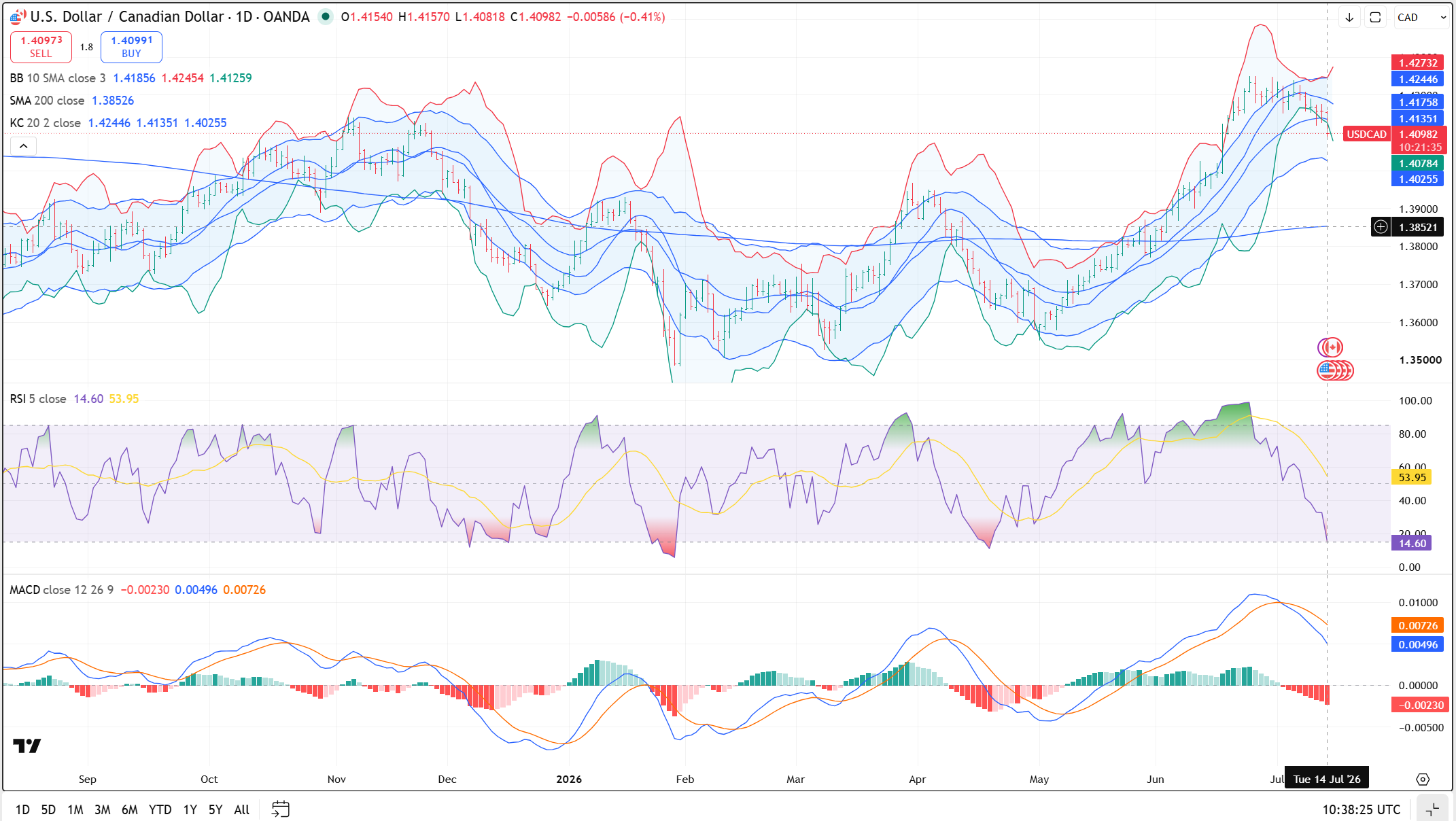

USDCAD open: 1.4086, overnight range 1.4055-1.4158, close 1.4159

USDCAD retreated overnight on the back of surging oil prices after Trump launched a fresh round of attacks on Iran after accusing the country of “breaking a deal.” USDCAD extended the sell-off following todays tame US inflation report. The overnight action was all due to geopolitics and the outlook for US inflation with Fed Chair Warsh’s Congressional testimony a key focus.

WTI rose 3.4% overnight, trading in a 77.91-81.27 range and is at 80.42 in NY.

The Canadian economic calendar is empty today but the BoC monetary policy decision and MPR report is on tap tomorrow.

USDCAD Technical Outlook

The intraday USDCAD technicals turned sharply bearish on the hourly chart after price broke below the S1 (first support) pivot at 1.4104, driving the pair through the lower Bollinger band near 1.4050. The hourly RSI still carries downside momentum. A decisive break below 1.4050 opens the door to 1.4020, while a recovery back above 1.4110 would put 1.4170 back in focus.

The longer-term outlook remains bullish above the 200-day moving average at 1.3850, which continues to underpin the advance that has carried price up from the base near 1.3850.

For today: USDCAD support is at 1.4040 and 1.4010. Resistance is at 1.4110 and 1.4150.

Today’s expected range is 1.4040-1.4110.

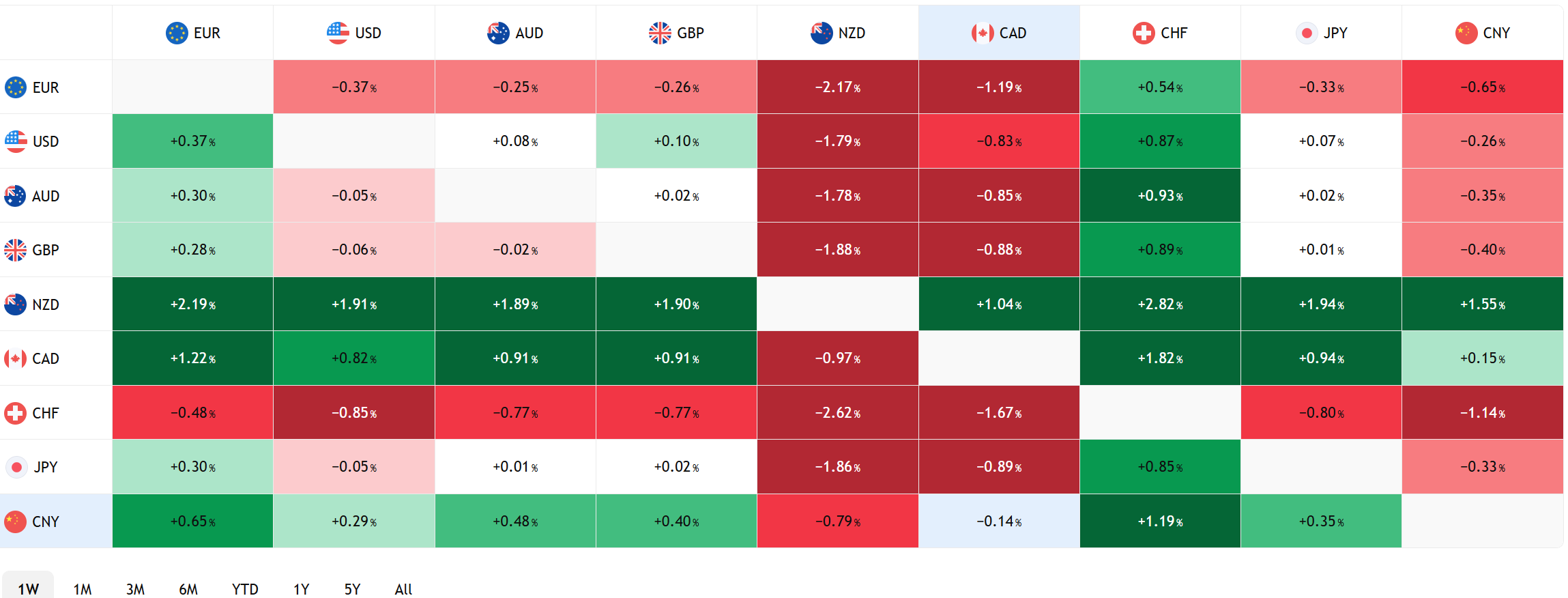

FX Heat Map

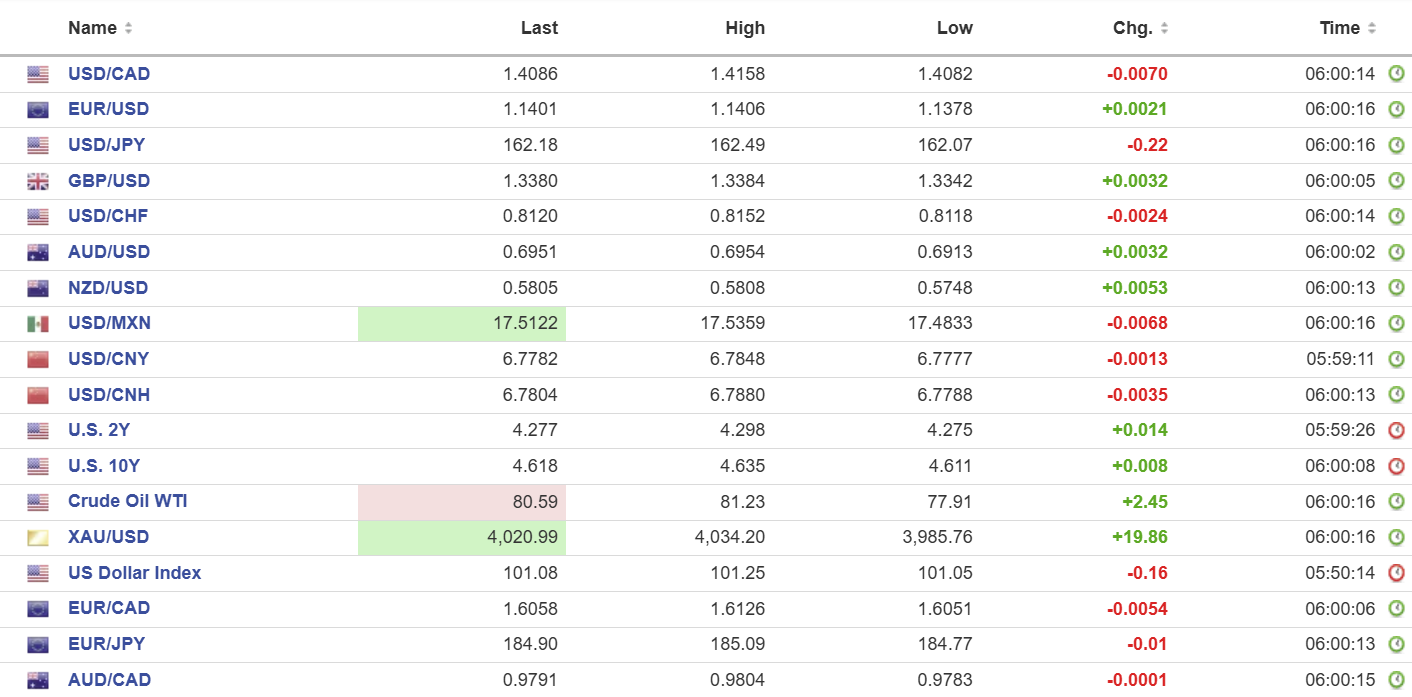

FX open high low 6:00 am

The Main Event(s)

Today’s US inflation data carried more weight than usual after Fed Governor Christopher Waller made some rather hawkish comments yesterday, which raised the odds for a Fed rate hike this month. He said “If we get another hot reading on core inflation this week, then the FOMC will need to consider tightening monetary policy in the near term.”

Today’s CPI result took any risk of a July hike off the table and into the garbage.

CPI forecast fell 0.4% m/m (forecast-0.1% m/m ) and rose 3.5% vs estimates for a 3.8% y/y increase. Core CPI was flat rather than the 0.2% m/m expected while the annual number rose 2.6% (forecast 2.8% y/y).

The US dollar index plunged to 100.67 from a pre-CPI level of 101.06, gol prices jumped to 4102.72 from 4029.40 and the 10-year Treasury yield dropped to 4.518 from 4.606.

Fed Chair Warsh may comment on the results when he testifies before Congress at 7:00 am PT.

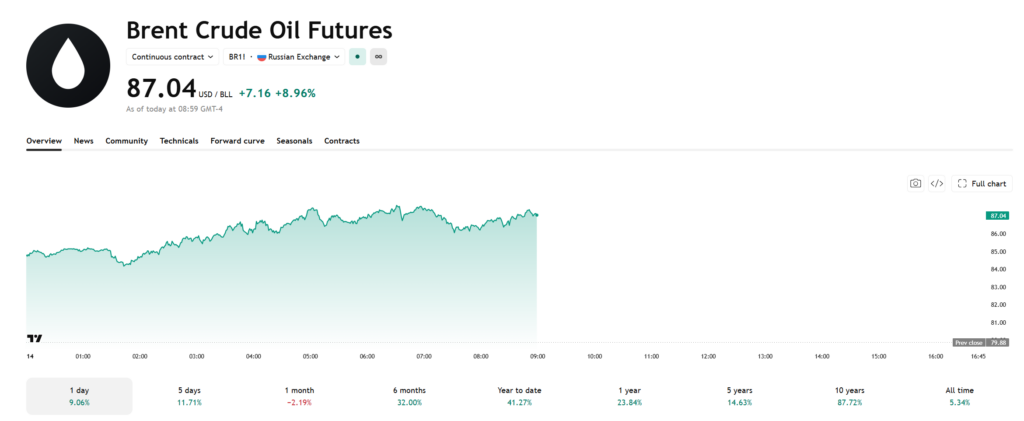

Oil Prices Soar

Europeans will be rather unhappy with the latest developments in the Middle East which sent Brent oil (the European benchmark) price soaring 8.96%.

The US launched more strikes on Iran and announced a new naval blockade of the country. Trump said that the Iran war is “going well” and repeated that Iran has “no air force, no navy, no military” The IRGC did not get the message and despite not having an air force, navy, or military, managed to launch a series of counterattacks at US military infrastructure in Bahrain, Kuwait and Jordan.

Taking Stock

Asian equity indexes closed mixed to higher. Japan’s Topix rose 0.74%, Hong Kong’s Hang Seng gained 0.52% and Australia’s ASX 200 closed flat.

As of 5:40 am PT, European bourses are digging themselves out of an overnight hole following today’s tame US CPI numbers. The French CAC 40 is down 0.36%, the German DAX is down 0.38% and the UK FTSE 100 is now flat and S&P 500 futures are 0.31%.

EURUSD | Range 1.1378-1.1463

EURUSD remained rangebound ahead of today’s US CPI data then spiked to 1.1463 from a pre-CPI level of 1.1414. EURUSD downside continues to be underpinned by expectations for two ECB rate hikes by year end.

GBPUSD | Range 1.3342-1.3444

GBPUSD rallied from 1.3388 to 1.3444 after todays US data but promptly dropped down to 1.3417. Traders are concerned that prolonged high oil prices will force the BoE to hike rates due to inflation risks.

USDJPY | Range 161.62-162.09

USDJPY dropped from 162.19 to 161.88 after tame US inflation data led to a sharp drop in US Treasury yields. Reuters reported that the government will add a footnote to its economic blueprint to stipulates the need for BoJ independence.

AUDUSD | Range 0.6913-0.6984

The Australian dollar is extended overnight gains after the US data and remains modestly bid following a 4.1% jump in Westpac’s consumer sentiment index to 83.9 from 80.6 in July. However, despite the jump, it is still one of the weakest readings in the survey’s 50-year history.

USDMXN | Range 17.3943-17.5359

USDMXN dropped from 17.4838 to the session low in the wake of falling US Treasury yields.

CHINA

- PBoC Fix: 6.7990 vs exp. 6.7927 (prev. 6.7972)

- Shanghai Shenzhen CSI 300 fell 2.15% to 4,796.50

China released blow-out trade numbers. Exports hit a record $412 billion, rising 27% in June (forecast 18.2%, May 19.4%) which helped boost its trade surplus to 125.6 billion

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics, Tradingview