July 16, 2025

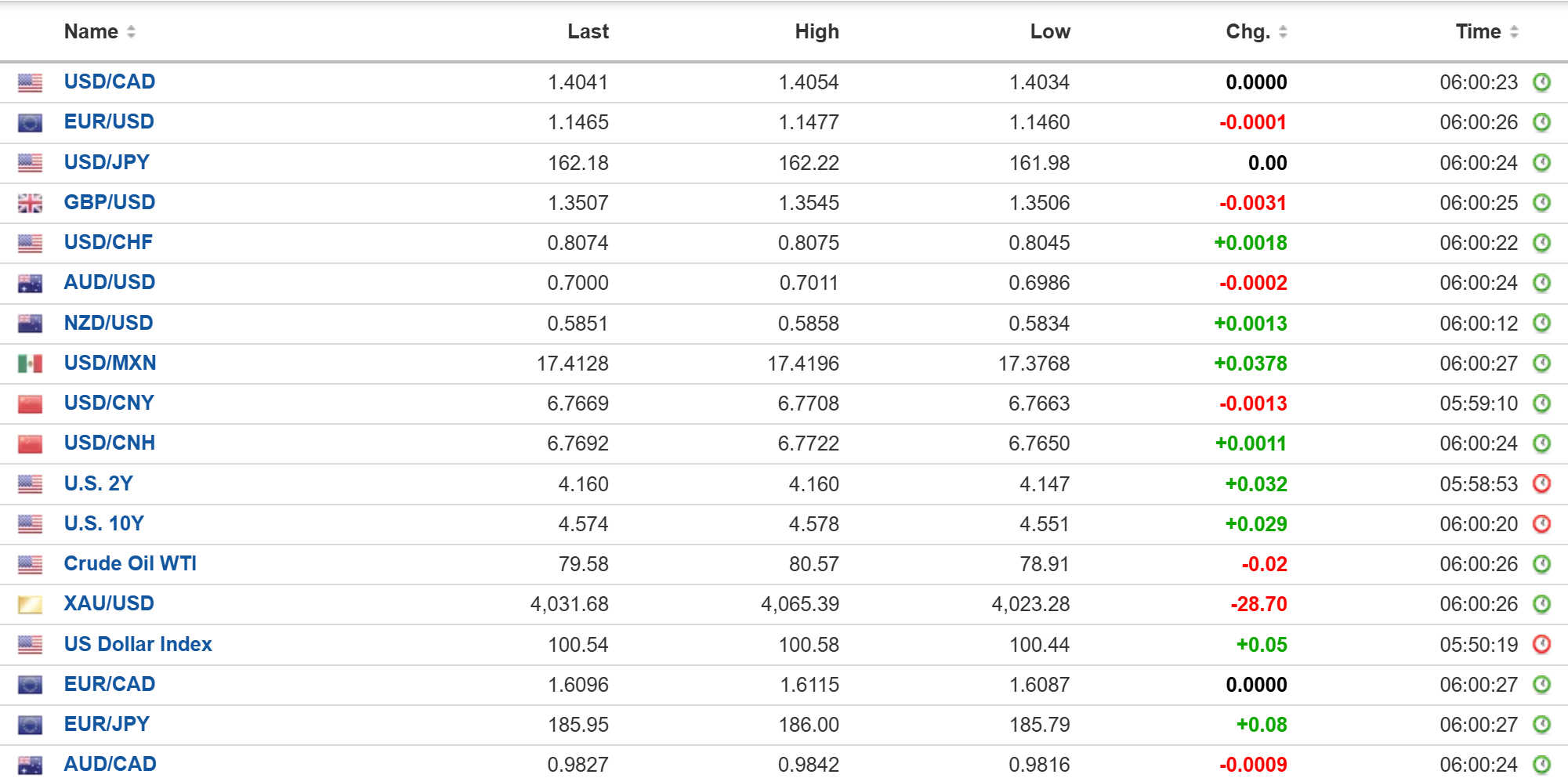

USDCAD open: 1.4041, overnight range 1.4021-1.4054, close 1.4042

USDCAD enjoyed another uneventful night with prices weighed down by the lingering impact from this week’s soft US inflation data and tame Bank of Canada monetary policy meeting.

Yesterday, the Bank of Canada left its policy rate unchanged at 2.25%, and its July Monetary Policy Report struck a more upbeat tone on the economy. Policymakers believe the ingredients for a sustained recovery are beginning to fall into place, with exports expected to lead growth and businesses increasing investment as they adjust to tariffs, diversify markets and strengthen supply chains.

WTI oil traded in a 78.91-80.57 range overnight. Prices are steady as traders are not convinced that the latest outbreak of hostilities between the US and Iran will lead to escalation and a more prolonged war.

The Canadian data calendar is empty.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish following the steady slide from the July 14 levels near 1.4150 that drove prices to a 1.4021 low today. A decisive break below 1.4020 targets 1.4000, then 1.3960 while a move back above 1.4070 would shift focus to 1.4210.

The longer-term outlook suggests the recent USDCAD weakness is merely a correction rather than a trend change. However, it is a correction that may have further to go. The move below 1.4080, targets the 38.2% level at 1.3984, which coincides with the lower daily Bollinger band at 1.3991. However, the daily RSI is at an extreme oversold level suggesting that the correction is stretched and vulnerable to a countertrend bounce before the downtrend extends.

For today: USDCAD support is at 1.4020 and 1.3990. Resistance is at 1.4070 and 1.4110.

Today’s expected range is 1.3990-1.4060

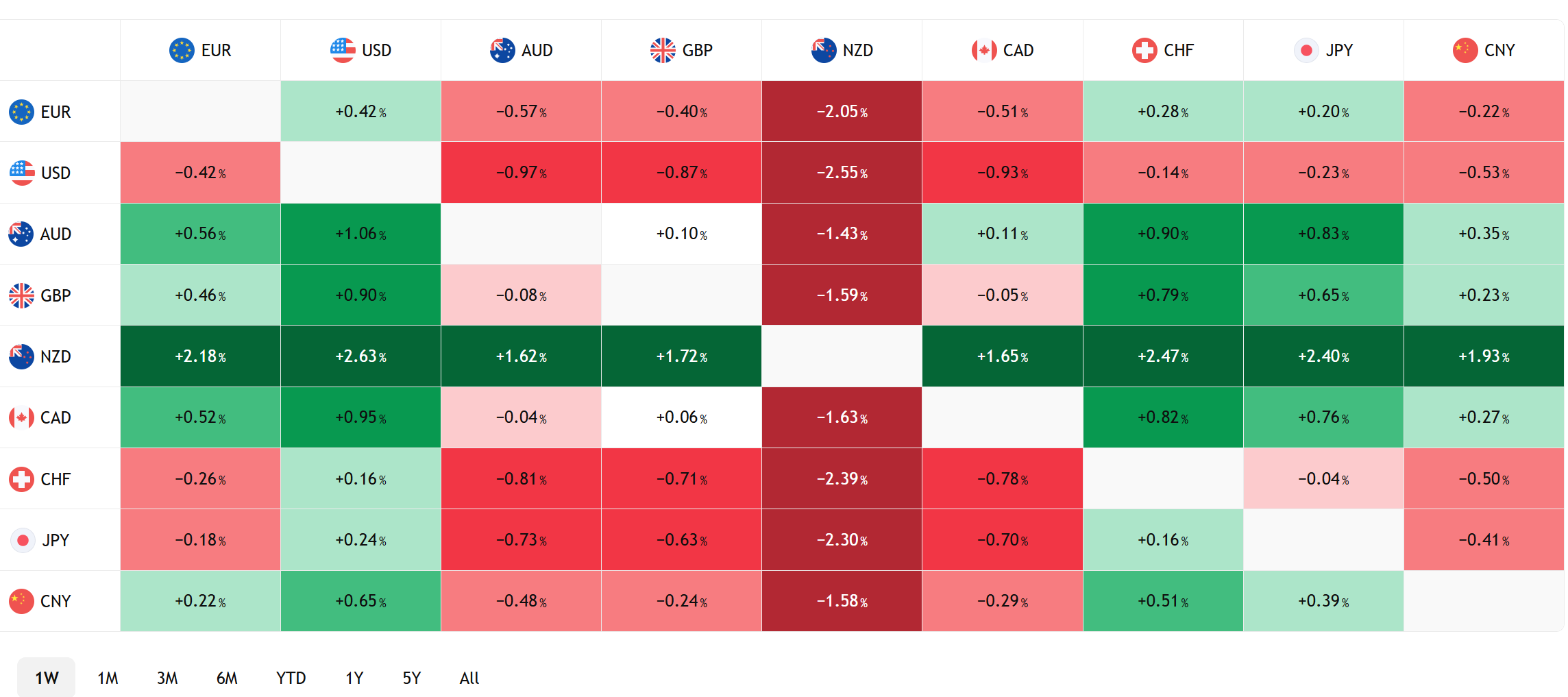

FX Heat Map

FX open high low 6:00 am

Managing Expectations

This week’s US inflation reports, CPI and PPI, were soft and better than expected. The news knocked Treasury yields lower, gave equities a boost and weighed on the greenback. Fed Chair Kevin Warsh and Governor Christopher Waller have pushed back on reading too much into one number and Warsh repeated that mantra on Day 2 of his Congressional testimony.

The only thing holding back a much bigger reaction to the data and comments were oil prices. They have remained steady and bid because Trump continues to threaten, disparage and bomb Iran while the IRGC remains defiant. White House officials claim Trump is considering expanding the war, which could include seizing Kharg Island, according to the WSJ.

American Economic Resilience

Today’s US data dump painted a picture of an economy that refuses to slow down. June retail sales rose 0.2% m/m, matching forecasts, but the details were far better than the headline.

The weakness was concentrated in gasoline stations, where receipts fell 5.3% because of lower pump prices, and sales excluding gas rose a solid 0.7% while the control group gained 0.5%. May was revised up to 1.0% from 0.9%.

Meanwhile, weekly jobless claims fell to 208,000 compared to the 217,000 forecast, continuing claims eased to 1.805 million, and the Philadelphia Fed Manufacturing Index exploded to 41.4, crushing the 13.0 consensus and June’s 10.3 reading.

The combination suggests the same falling energy prices that flattered this week’s inflation reports also flattered the retail sales headline, and once you look through the oil effect, consumers are still spending, factories are humming and the labour market shows no cracks. That gives the Fed every reason to be patient before cutting rates.

Taking Stock

Asian equity indexes closed on a mixed note. The Australian ASX 200 was unchanged while Hong Kong’s Hang Seng rose 1.33% and Japan’s Topix fell 1.45%.

As of 7:25 am European bourses are negative. The German DAX is down 0.77%, the French CAC 40 has lost 0.84% and the UK FTSE 100 is down 0.30%. S&P 500 futures are down 0.22%, the 10-year Treasury yield is 4.574%, the DXY is 100.56 and gold is 4,024.79.

EURUSD | Range 1.1460-1.1477

EURUSD hung around yesterday’s 1.1462 NY closing rate as upside momentum has stalled. Elevated crude prices and the risk of a wider US and Iran conflict are acting as a drag on gains. Warsh’s refusal to declare victory on inflation Tuesday and again yesterday gave euro bulls little fresh ammunition, and traders are wary of headline risk from the Gulf ahead of US retail sales.

GBPUSD | Range 1.3503-1.3545

GBPUSD is the weakest major currency against the US dollar overnight, probably due to bruised egos after Argentina ended England’s 2026 FIFA World Cup dream. English football fans in the US needed to sell yards of sterling to buy enough beer to drown their sorrows.

If not that, GBPUSD weakness may be explained by mixed to disappointing data. May GDP rose 0.1% m/m as expected, recovering from April’s 0.1% contraction, while the goods trade deficit narrowed sharply to £18.66 billion from £24.58 billion. That good news was more than offset by Industrial Production, which fell 0.5% m/m, well below the -0.1% forecast.

USDJPY | Range 161.98-162.22

USDJPY bounced from its Asian low after the US renewed attacks on Iran. The risk of further escalation in the war driving crude prices higher overshadowed the lingering threat of intervention.

AUDUSD | Range 0.6986-0.7011

The Australian dollar poked above 0.7000 for the first time since June 22 due to the residual impact of US inflation numbers suggesting the Fed may find it difficult to raise rates, while the RBA has no such constraints. Consumer inflation expectations cooled to 4.7% compared to 5.5% previously.

USDMXN | Range 17.3768-17.4196

USDMXN continues to consolidate its recent losses following tame US inflation data. However, renewed US and Iran hostilities limited the downside.

CHINA

- PBoC Fix: 6.7909 vs exp. 6.7577 (prev. 6.7910)

- Shanghai Shenzhen CSI 300 fell 1.5% to 4,698.44

Sources: Investing.com, Bloomberg, Reuters, Yahoo Finance, US Census Bureau, Trading Economics, Tradingview