By Michael O’Neill, Agility FX Senior Strategist

Tis the season to be spooked. Halloween is just around the corner and soon herds of ghoul’s, ghosts and goblins will haunt neighborhoods, demanding treats or threatening tricks.

Canadian’s got a preview of this year’s Halloween hijinks on October 19. That was when the Bank of Canada’s Stephen Poloz, clad in the costume of a central bank governor (and for him, not much creativity was involved) delivered both a treat and a trick.

The treat, for financial markets, was in the form of an interest rate statement that was mostly “as expected”. The Bank of Canada left interest rates unchanged and expressed optimism about a global economic recovery regaining momentum in the second half of this year and through 2017 and 2018. The optimism was tempered by acknowledging that the recent Federal government measures to restrain residential investment would act as a drag on economic growth.

The trick came at the quarterly Monetary Policy Report press conference.

Near the tail end of his opening statement, BoC Governor Poloz said “Given the downgrade to our outlook, Governing Council actively discussed the possibility of adding more monetary stimulus at this time, in order to speed up the return of the economy to full capacity.”

To traders actively selling USDCAD because of a steep oil price rally that occurred prior to the press conference, those words were as terrifying as seeing Pennywise the Clown emerging from your bath tub drain.

Source: ABC movie trailer, 1990

The Canadian dollar lost over one cent in value by the next day.

The thing about Halloween and Bank of Canada Monetary Policy Reports (MPR) is that they are not what they seem. One is by design and the other by default. Halloween is all about pretending to be something that you aren’t while an MPR report is pretending to predict the future.

The BoC readily admits to guesswork in the MPR. They make assumptions to five key inputs to their Base Case Projection. These are 1) Oil prices will remain near the recent average levels. 2) they assume that the Canadian dollar will remain close to its recent average of 76 cents. 3) they assume that the output gap is -1.5 percent. 4) they assume that Canadian potential output growth will be at the midpoint of the Banks estimated range. 5) they assume that the neutral policy rate in Canada is between 2.75 and 3.75%.

That’s a lot of assumptions.

A lay person can be forgiven for comparing the Bank’s qualifications of the MPR assumptions to playing a lottery. Pick five numbers from a previous LottoMax ticket, randomly select two others and hope it produces a winner.

Nevertheless, the MPR is a useful guide to understanding how the policy makers see the domestic economy proceeding in the coming months.

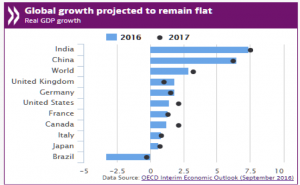

The Bank of Canada expects that the global economy will regain momentum in the second half of this year and through 2017 and 2018. That contradicts the Organization for Economic Cooperation and Development outlook. The OECD lowered their global outlook on September 21 due to downgrades in major advanced economies, notably the United Kingdom, offset by gradual improvement in major emerging market commodity producers. They noted that growth in the major advance economies would be subdued.

.

Source: OECD

The BoC has another conundrum. Near the end of March 2016, the Federal government announced a raft of stimulus spending measures designed to boost domestic economic growth. There was an unwanted side effect. Canadian dollar strength. The BoC says they do not target the exchange rate but Mr. Poloz, the former head of Canada’s Export Development Corporation, knows full well-the value that a weak currency has on exports.

The BoC is still waiting for the March stimulus measures to show up in the economic statistics and the recent changes to the mortgage rules threaten to put a dent into those stimulus package benefits.

Canada’s overnight rate is a mere 0.5%. It has been unchanged since July 2015 when it was cut by 0.25%. Do you remember the corresponding surge in the domestic economy? No? That’s because it didn’t happen.

The European Union and Japan have recently turned to negative interest rates. And coincidently, neither economy is any better off than they were before the moves.

Mr. Poloz and his colleagues are well aware of the European and Japanese economic performance in a low and negative interest rate environment. They are also aware of the damage that extremely low interest rates have on the retirement accounts of tax-payers, especially in economies with aging populations.

In addition, they weren’t eager to cut interest rates, in part, because a rate cut could embarrass the Federal government. If the BoC reduced the overnight rate it would signal to the world that the highly touted Liberal Party fiscal stimulus package was not getting the job done. You don’t mess with Mother Nature or the Liberal Party

Fortunately, it is close to Halloween. It is the time of year to “pretend”. That may have inspired Mr. Poloz to deliver a “pretend” interest rate cut.

The BoC was fully aware of market expectations for a modest downgrade in the Bank of Canada outlook and arguably, neither the interest rate statement or the MPR would have created much of a stir in financial markets. That was evident in the Canadian dollar reaction when they were released. The Canadian dollar continued to drift higher on the back of rising oil prices.

Seventy-five minutes after the rate announcement, Mr. Poloz began his MPR press conference. He milked his moment. It wasn’t until he was almost through reading his opening statement when he said that the Governing Council discussed cutting rates.

Boom! The Canadian dollar plunged. The TSX soared.

Those moves are exactly what would have occurred if the Bank of Canada had actually cut rates by 0.25%.

Mission Accomplished! A “stand pat” move with benefits. A ghost rate cut. Trick or Treat!

.