Whenever President Trump interacts with Prime Minister Trudeau, Mr. Trump’s smarmy smile suggests that Metallica’s Master of Puppets, is playing in his head. And there is no question about who the “master” and who the “puppet” are.

At the beginning of the year, Stephen Schwarzman, a senior business advisor to President Trump, told the Prime Minister that the Trump administration’s trade concerns didn’t apply to Canada. Those words were still ringing in Trudeau’s ears when he had a face to face meeting with the President in Washington on Valentine’s Day. Justin didn’t bring a dozen roses and chocolates but he did keep his concerns about US policies on Immigration, the US travel ban, Climate Change, and NAFTA to himself. After all, Justin and Donald were going to be “besties” so why poke the bear?

February faded into April and President Trump’s memory about NAFTA tweaks faded as well. On April 24, Trump blindsided Trudeau by announcing a 20 percent tariff on Canadian softwood lumber. The Canadian dollar sank.

Two days later, he upped the ante. The Washington Post reported that Trump was contemplating an Executive Order to withdraw from NAFTA.

That caused a kerfuffle. The Mexican peso and Canadian dollar got hammered.

The next day, President Trump had a change of heart. He chose not to terminate NAFTA but said he would merely renegotiate it.

Canada was under attack in what was shaping up to be a “Trade War”.

Prime Minster Trudeau reacted decisively. He took a page out of former President Obama’s playbook and made empty threats. (Remember, Obama telling Syria in 2012 about crossing a “red-line” by using chemical weapons)

On May 5, Mr. Trudeau decided to consider banning Thermal Coal exports to the US and would consider targeting Oregon industries. (Oregon is the home state of lumber hardliner.) Nothing has happened.

Trump’s NAFTA renegotiation plans became official on May 18. The Trump administration sent a letter to Congress that triggered a 90-day consultation prior to formal talks.

Canada “considers” while NAFTA burns.

NAFTA isn’t the only concern for USDCAD traders. There are a lot of potential risks on the short-term horizon as well.

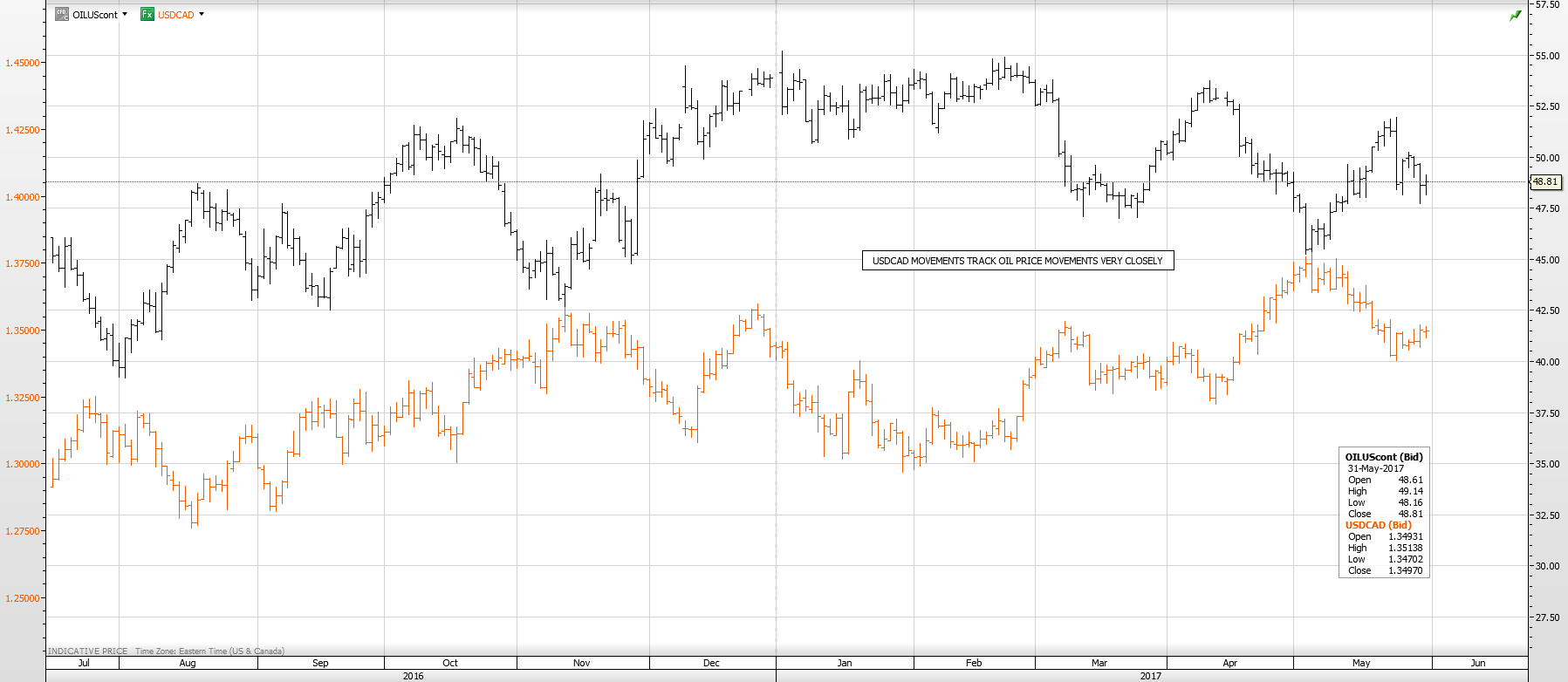

Oil prices play an outsized role, especially when markets lack top-tier economic data and official policy guidance to provide trade direction.

WTI oil prices have slid rather dramatically since May 25 when Opec announced a nine-month extension to the production cut agreement.

A lot of the move can be explained by profit-taking. WTI prices had risen strongly since the beginning of May when the possibly of a production cut extension started to gain traction. The sell-off was exacerbated by fears of rising supply from Libya, US shale producers and stubbornly high US crude inventories.

Prices recovered somewhat, on June 1, when the Energy Information Administration reported a 6.4 million barrel decline in US crude inventories. The Canadian dollar will garner some support if prices remain above $46.00/barrel.

The US economic recovery is well established although recent economic reports have been uneven. The ISM Manufacturing Purchasing Managers Index (PMI) ticked up to 54.9 in May from April’s 54.8 reading. The result should keep US GDP growth forecasts intact and do nothing to dissuade the Federal Open Market Committee from raising US interest rates at least twice more in 2017. A 0.25 percent rate increase is fully priced into current exchange rates with a 95.8% probability of a hike, according to the CME FedWatch tool.

At 4.4 percent, the US has achieved “full employment” according to many economists. On June 2, that number will be refreshed when the nonfarm payrolls report is released. The US is expected to have added another 185,000 jobs in May. An upside surprise to the job gains coupled with a jump in average hourly earnings, would boost the US dollar immediately and raise questions as to whether just two more rate increases in 201, would be enough. If so, the Canadian dollar would come under pressure.

Economic and currency developments in China have implications for the Canadian dollar as well. On June 1, the Caixin PMI dipped below 50.0 and came in at 49.6. (A level above 50 indicates economic expansion, while a level below 50 indicates economic contraction). This is a volatile data series so a few more results are need to conclude the China economy is shrinking. Additional concerns about the health of the Chinese economy may be raised on June 8 when China releases Trade data. A weak Chinese economy undermines global growth and for Canada suggests reduced exports.

The European Central Bank (ECB) meeting on June 8 could result in Canadian dollar weakness resulting from EURCAD demand.

EURUSD has been in an uptrend since the middle of February and the move became more intense following Emmanuel Macron’s win in the French election. His win put an end to fears of a right wing, anti-Euro France. It also meant that the European Central Bank could consider ending their stimulus program, at least to German Bundesbank officials.

If ECB President Mario Draghi provides forward guidance hinting at an earlier end to stimulus, EURUSD would soar and EURCAD would go along for the ride.

The UK election is June 8. It pits Prime Minister Theresa May’s Conservative government against Jeremy Corbyn’s Labour party.

Expectations that Ms. May was sure to win and with with an expanded majority have taken a turn for the worse. On June 1, a YouGov poll for the Evening Standard put Mr. Corbyn as the favoured candidate with a 17 point lead over the Conservatives. Labour is reportedly more open to working with the EU as opposed to the Conservative’s “hard-Brexit” position. Whatever the result, the reaction in EURGBP will spill over into GBPCAD.

President Trump may be the puppet master when it comes to dealings with Prime Minister Trudeau, but in the short-term, he is just one of the players pulling the strings to make the Canadian dollar dance.