By Michael O’Neill

Donald Trump campaigned on ending the North American Free Trade Agreement. (NAFTA). He described it as “the worst deal ever.”

What is the “worst trade deal ever”? In a nutshell, it is a tri-lateral deal between the United States, Canada, and Mexico, in effect since January 1994, to encourage the free flow of goods between countries by eliminating tariff barriers to agriculture, manufacturing, and services.

On April 26, rumors were rife that President Trump would fulfil his promise and terminate the trade deal.

He was going to but he didn’t. The very next day, he said he had a change of heart after speaking with the Mexico’s President Enrique Pena Nieto and Canadian Prime Minister Justin Trudeau. He said “I decided rather than terminating NAFTA, which would be a pretty big, you know, shock to the system, we will renegotiate.”

On July 17, the Office of the United States Trade Representative released the “Summary of Objectives for the NAFTA Renegotiation.” (SONR) It certainly lacked the anticipation given to Season 7 of Game of Thrones, but for the lawyers billing $700/hour, it was the next best thing.

The American aim is to “Improve the U.S. trade balance and reduce the trade deficit with the NAFTA countries.” That’s not a bad thing.

Reading the 18 page SONR is a cure for hardcore insomnia. There is also a bit of “Donald Trump-esque hyperbole” scattered throughout the document. For example, who does this sound like?

“For years, politicians promising to renegotiate the deal gave American workers hope that they would stop the bleeding. But none followed up.” The only thing missing is redundant superlatives.

The American’s want the new NAFTA to break down barriers to American exports. This includes the elimination of unfair subsidies (read Canadian softwood lumber, beef, and dairy products). They also want the elimination of market distorting practices by state owned enterprises

That appears to be reasonable. The devil, as usual, is in the details.

The American’s want to “increase opportunities for U.S. firms to sell U.S. products and services into the NAFTA countries while simultaneously reducing access of NAFTA countries to the US.

Specifically, “Buy American.” They want to exempt state and local governments from the commitments being negotiated.

Adding insult to injury, the Americans want to get rid of the existing dispute resolution process, probably because it has ruled against them in the past.

The expression “you can’t have your cake and eat it, too, means that if you eat your cake, obviously, it is gone. The SONR document suggests that the American’s don’t believe that to be the case.

At first glance, the USA appears to hold the upper hand in the negotiations. World Bank 2016 data shows US GDP at $18.5 trillion dollars while Canada’s and Mexico’s GDP was a combined $3.0 trillion.

They are the 800-pound gorilla and will negotiate that way. President Trump tweeted “if we do not reach a fair deal for all, we will then terminate NAFTA.” It’s kind of an ultimatum like “It’s my way or the highway.”

However, this gorilla is wearing carefully dyed hair plugs in hopes of masking his infirmities.

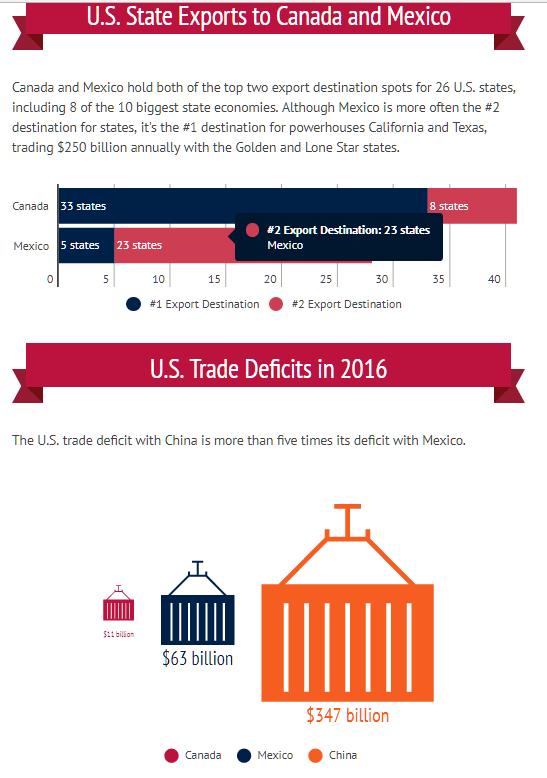

Canada and Mexico are very important to the majority of American states. The American Society/Council of the America’s warned that if President Trump pulled the US out of NAFTA, it would be a disaster; risking $1.0 trillion in trilateral trade with immediate repercussions.

The following chart is from their website.

Source: as-coa.org

Foreign Exchange traders do not appear to be overly concerned about NAFTA negotiations having a negative impact on the Canadian dollar. The currency has strengthened since the SONR document was released.

However, that has far more to do with the hawkish shift by the Bank of Canada and expectations of three rate increases by early 2018.

And that’s not all. The US dollar has been under steady pressure against the major currencies. That has nothing to do with free trade agreements.

It is largely because of a growing perception that the pace of Fed rate hikes will slow dramatically. At the same time, other G-7 central banks are drifting into a rate hike cycle. The evidence is in EURUSD.

The single currency has climbed from 1.0570 in April to 1.1657 on July 20. There are several factors behind the rally but the main driver has been rising expectations that the European Central Bank (ECB) will be ending its easy money policies.

That was clear by the reaction to the July 20 ECB policy statement and President Mario Draghi’s press conference. EURUSD soared despite Mr. Draghi’s best efforts to downplay the details and timing of the next move. Trader’s ignored his doveish remarks and focused on the rosy outlook for the Eurozone economy.

President Trump and Mario Draghi are learning that even though they are at the helm of the ship, they cannot control the ocean currents. Mario Draghi’s clumsy attempt at micro-managing the impact of a growing economy has unleashed a herd of EURUSD bulls. Mr. Trump may be on the cusp of discovering that the “worst deal ever” is the “worst deal-never,”