By Michael O’Neill

It was the best of times, (if you were a Canadian rate dove) and it was the worst of times. (if you were a Euro rate hawk.) And if you aren’t Charles Dickens, that opening line is plagiarism.

Many traders spent the past two month’s eagerly awaiting the September 7 European Central Bank(ECB) policy statement and press conference. And justifiably so.

ECB President Mario Draghi gave a speech in Sintra, Portugal on June 27 that opened the door to a quantitative easing tapering announcement as early as September. Mr Draghi said that as the economy recovers and inflation firms, he could remove unconventional measures, without tightening policy.

At his July 20 press conference, Mr Draghi contradicted a dovish policy statement by talking about rising inflation and the need to discuss the ECB’s QE program at the September meeting.

It was those kinds of comments from Mr Draghi and other ECB officials that led traders to anticipate an informative ECB policy statement with the press conference providing clarity.

It didn’t happen. Traders were tricked.

The ECB left policy unchanged and essentially delayed all decisions until the October 26 meeting.

In Ottawa, Bank of Canada (BoC) Governor Stephen Poloz came across as a confident, decisive central banker.

On September 6, the BoC announced it was raising its target for the overnight rate to 1.00%, a 0.25 basis point increase. The move caught many traders and economists by surprise. A Reuters survey conducted on September 1 showed that 24 of 33 economists surveyed expected rates to remain unchanged. A major reason for the

stand-pat” forecast was that there wasn’t a press conference scheduled for the September 6 meeting.

The BoC did not need a press conference to explain themselves. The Q2 GDP report on September 1 did all the talking necessary. The 4.5% growth rate and the jump in consumer confidence fulfilled the Bank’s requirement stated in the July statement that “future adjustments will be guided by incoming data.” The data delivered, and so did the Bank.

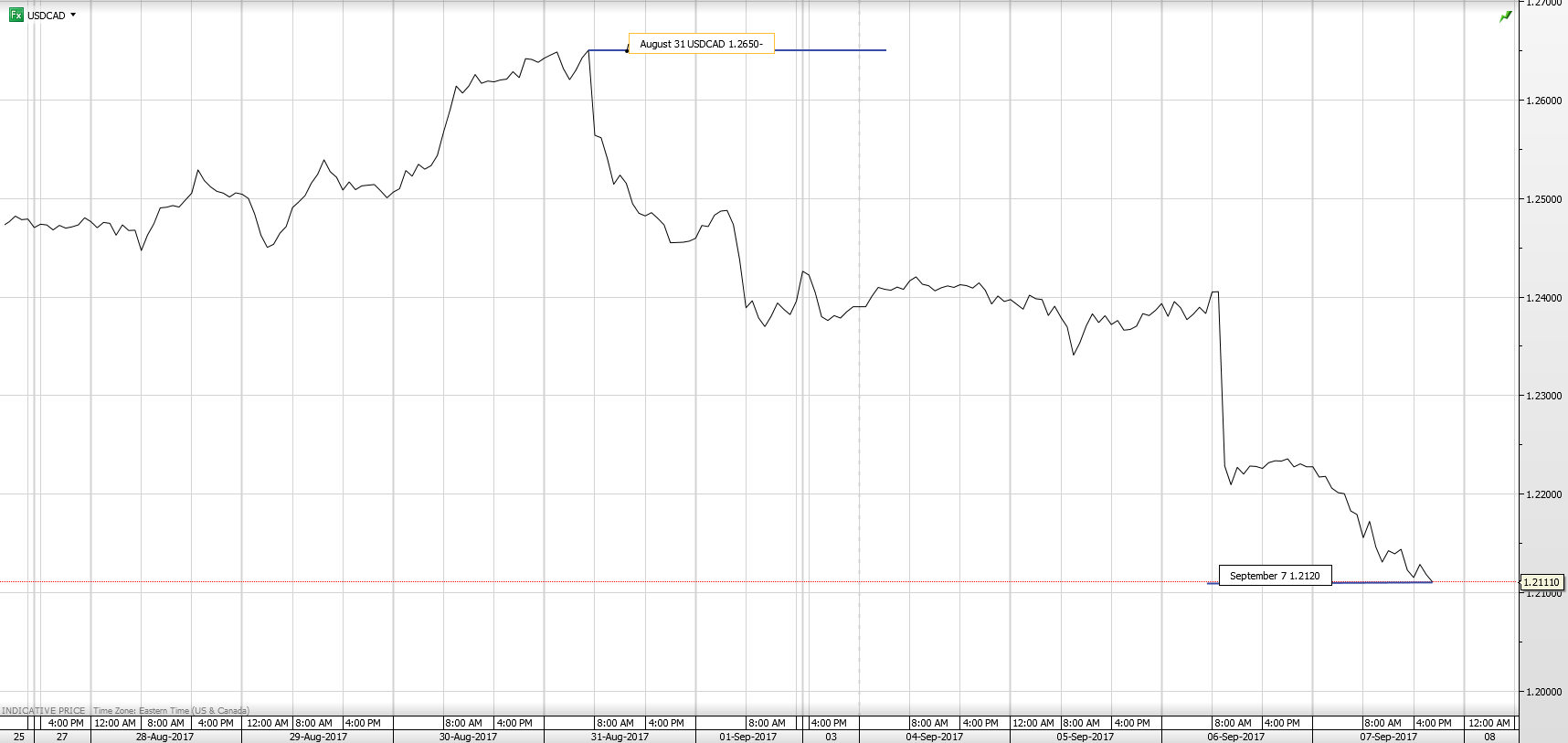

The Canadian dollar rallied ahead of and after the news, gaining 4.25% since the August 31. That is a very large move for a mere ¼ point hike in interest rates which raises questions about how sustainable the move is.

One camp believes that not only is the move sustainable, there is still a lot of upside. They note that the two recent rate increases just remove the stimulus put in place in response to the 2015 oil price collapse and subsequent deflation risks. Those issues have disappeared. Now, the concern is that if the Bank wants to avoid overheating the economy more rate hikes are needed. That thinking has increased the odds for a third interest rate hike, in October.

The Canadian dollar is also benefitting from broad US dollar weakness because US rate increases have stalled. The CME Fedwatch tool puts the odds for a US rate hike in December at only 31%. A lot of that is because markets seem to have dismissed hopes of a jump in US economic growth from President Trump’s tax cut and infrastructure spending promises. He hasn’t been able to get anything done.

Oil price stability has provided another layer of support to the Loonie. West Texas Intermediate has stayed within a $42.00-$55.00 range all year. If that keeps up, oil price movements will be less of a factor Canadian dollar moves.

FX exchange price moves are rarely one-way, and that will be the case for the Loonie as well.

There are headwinds, and one of those headwinds, the North American Free Trade Agreement renegotiation (NAFTA) could grow to Hurricane Irma proportions.

As John Heywood wrote in 1546, “it’s an ill wind that blows nobody any good”. In NAFTA negotiations the ill wind is President Trump. He has threatened to rip up NAFTA in the past and continues to do so. His latest threat was on August 27th, even as the negotiations were going on.

He tweeted “We are in the NAFTA (worst trade deal ever made) renegotiation process with Mexico & Canada. Both being very difficult, may have to terminate?” That wouldn’t be good for the Canadian dollar.

Mr Trump’s bullying taunts and tweets have inflamed tensions with North Korea. In turn, FX markets are keeping one finger on the “safe-haven” trade switch. The Canadian dollar tends to under perform during periods of risk aversion.

The Fed is a wild card. Depending on its direction, it could boost or crush the Canadian dollar.

Minneapolis Fed President Neel Kashkari said on September 5th, “ It’s very possible that our rate hikes over the past 18 months are leading to slower job growth, leaving more people on the sidelines, leading to lower wage growth, and leading to lower inflation and inflation expectations.“ Another Fed Governor, Lael Brainard was urging caution about raising rates due to low inflation.

On September 7, Cleveland Fed President Loretta Mester said the Fed needs to raise rate now because waiting too long would have economic consequences.

That discord has led markets to concluded that US rates aren’t going anywhere until sometime in 2018

But all that could change in a hurry. On September 6, Fed Vice Chair Stanley Fisher resigned, effective mid-October. His departure leaves four of the seven seats on the Fed board vacant. Fed Chair Janet Yellen’s term as chair is up in February.

President Trump appoints the governors, and there are a lot of vacancies.

Mario Draghi and Stephen Poloz are two birdies with one thing in common. They are rate hawks(or fledgelings) while a cote of doves resides at the Fed. That’s good news for the Canadian dollar.