By Michael O’Neill

It seems that every day, since January 20, 2017, world leaders, politicians and average citizens have awakened to a new stress. Ground zero for the stress is the Oval Office. It is called PTSD; President Trump Stress Disorder.

The stress arises from threats and bombast. ie: construction of a Wall between Mexico and the US border, rumours of Republican Party/Russia collusion, shredding of Trade agreements, the repeal of healthcare benefits for millions of Americans, anti-immigrant vitriol, and even a threat to “totally destroy” North Korea.

The stress gauge nearly broke on September 25. Kim Jong-un, North Korea’s ruler, decided that Trump’s UN speech amounted to a declaration of war.

FX traders got spooked. The thought of nuclear war unnerved them, and they scrambled to buy safe-haven assets. Gold, Swiss francs and Japanese yen were in heavy demand.

President Trump may have spooked himself. Perhaps he realised that his mouth was no different than the gun that took out Archduke Ferdinand in 1914. The archduke’s death led to a domino effect of opposing national alliances that eventually involved 32 countries and four years of war. Whatever, the reason, Mr Trump turned his tweets to the NFL. Safe-haven trades were unwound.

Trump may have been the biggest cause of stress in FX markets, but he wasn’t the only one.

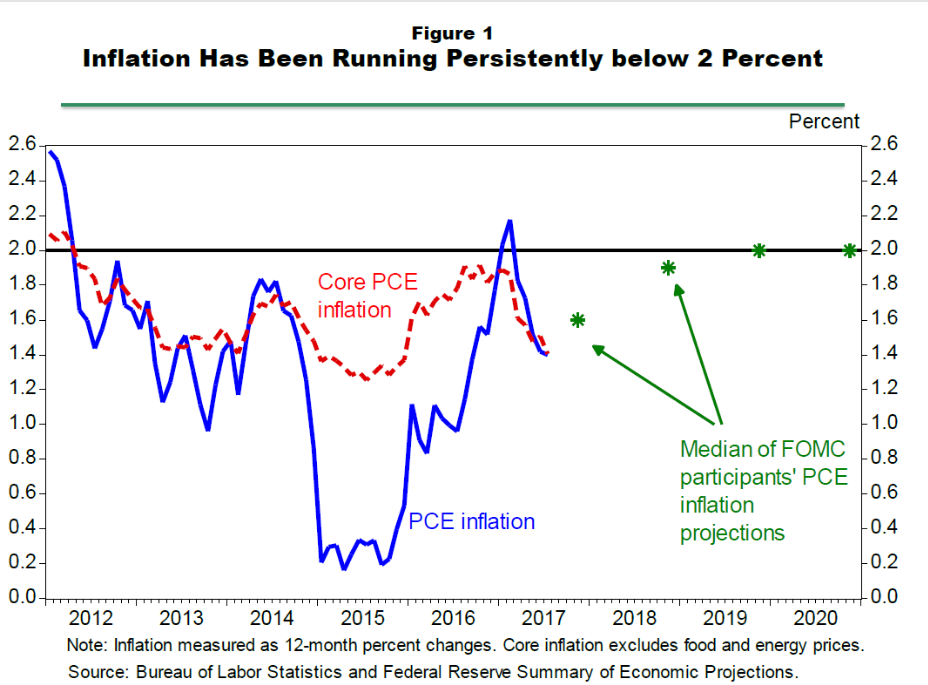

Expectations were low ahead of Fed Chair Janet Yellen’s speech to the National Association for Business Economics on September 26. After all, it was less than a week after her Federal Open Market Committee (FOMC) press conference, and not much had happened in the interval.

Ms Yellen warned, “persistently easy monetary policy might lead to increased leverage and other developments with adverse implications for financial stability.” She added, “For these reasons, and given that monetary policy affects economic activity and inflation with a substantial lag, it would be imprudent to keep monetary policy on hold until inflation is back to 2 percent.”

The dove sounded like a hawk.

FX traders reacted by buying US dollars across the board and pricing in a 76.4% chance of a rate hike in December. (CME FEDWatch)

Graph: US Inflation and FOMC members expectations

The Canadian dollar came under stress after Ms Yellens remarks. However, its losses were contained with the help of sharply rising oil prices. By mid-morning the next day, the Loonie was trading at pre-Yellen speech levels.

Then Bank of Canada (BoC) Governor Stephen Poloz added his “two-cents” worth. His two cents cost the Canadian dollar 1.3 cents.

The BoC hiked Canadian rates in September because of “stronger-than-expected economic performance” and “a slight increase in both total CPI and the Bank’s core measures of inflation.”

The monetary policy statement’s positive economic outlook led traders to expect another rate increase at the October policy meeting.

Mr Poloz dashed those expectations in a speech on September 27. The Governor echoed Janet Yellen’s remarks about the lag between monetary policy and inflation. He noted, “Any change in interest rates will not have its full impact on inflation for about a year and a half to two years.” He also said there is no predetermined path for interest rates” adding “Monetary policy will be particular data dependent”.

Those few words sent the Canadian dollar tumbling from 81.18 cents to 79.17.

The day got worse. US Secretary of Commerce Wilbur Ross imposed 220% countervailing duties on Bombardier CSeries aircraft, accusing Canada of subsidising the company. He has a point. Nevertheless, it is an overtly hostile move by the US government which is ostensibly renegotiating the North American Free Trade Agreement, in good faith. The US actions raise questions as to whether a deal is achievable and while those questions remain, Canadian dollar gains will be limited.

Fortunately for Canada (and the Canadian dollar), oil prices are providing a degree of stress relief.

West Texas Intermediate (WTI) prices have risen since the end of August, trading as high as $52.80 per barrel.

Chart: WTI oil

Price support is derived from many factors including Opec and International Energy Agency (IEA) information, indicating the oil market is rebalancing. Both agencies note that oil demand is stronger than expected while the global production is shrinking. The IEA said, “Based on recent bets made by investors, expectations are that markets are tightening and that prices will rise, albeit very modestly.”

President Trump Stress Disorder will derail FX markets as long as he is President and has access to Twitter. He can’t be ignored.

There is hope. The lasting impact of his words and actions on FX markets is slowly diminishing.That is due, in part, to the end of “summer markets” and the focus on fundamental economic data.