By Michael O’Neill

Forget about galaxy’s far, far away, this Bizarre War is just outside the door. At first, it was a localized skirmish between Canada, Mexico, and the US. It is now threatening to explode in a global conflagration of tit-for tat-tariffs involving the European Union, China, and other exporting nations.

It all started when President Trump demanded (and got) a renegotiation of the North American Free Trade Agreement (NAFTA). The trilateral talks began a year ago, round seven just ended and round eight begins in April. They do not appear to be progressing well.

The President is not on the US renegotiating committee, but it did not stop him from interjecting himself into the discussion. He often expressed his distaste for the existing agreement and lobbed hand grenades into the meetings by levying countervailing duties on Canadian soft-wood lumber and Bombardier aircraft. (US courts voided the Bombardier charge)

Then he upped the ante. On March 2, from the Presidential podium on Twitter, he proclaimed, in capital letters no less; “IF YOU DON’T HAVE STEEL, YOU DON’T HAVE A COUNTRY!.

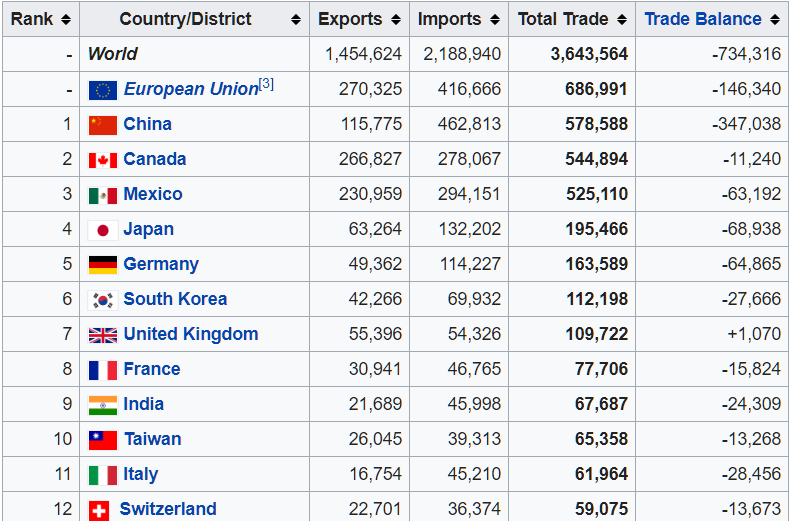

Those words put China in the cross-hairs. The next day, he added the European Union to the mix. He accused the EU of using massive tariffs and barriers against US companies doing business there, specifically naming cars, and threatened to tax European vehicle imports. President Trump is focused on shrinking the United States “$800 billion deficit.” (his words) by targeting those nations with a trade surplus vis-a-vis the US.

Chart: Nations the US has a trade deficit with

Source: Wikipedia

The skirmish risks becoming a full-scale war.

Financial markets reacted violently to news of the steel tariffs but had calmed down somewhat by Monday. Two things happened. The first was news that North Korea would consider scrapping their nuclear program which launched demand for “risky” assets. The second was Trump’s Economic Adviser Gary Cohn was said to be pushing back against tariffs. That was the calm before the storm.

The storm started with Round Seven of NAFTA negotiations concluding on a sour note. US Trade Representative Robert Lighthizer complained that “time was running short.” He said, “I fear that the longer we proceed, the more political headwinds we will feel.”

The storm worsened on March 6 when Mr Cohn resigned. Markets saw that as confirmation that implementation of the tariffs would go ahead. They may be right. There is a rumour that a Presidential proclamation on steel and aluminium tariffs will occur on March 8.

The tariff’s and the elevated risk that NAFTA gets cancelled was most certainly a hot topic of discussion at the March 7, Bank of Canada (BoC) policy meeting. In fact, they as much as admitted it. The fourth line of the statement said “trade policy developments are an important and growing source of uncertainty for the global and Canadian outlooks.”

If there is one certainty about the Bank of Canada (or any central Bank), it is that they abhor uncertainty. NAFTA, trade wars and tariff’s fit the bill.

The BoC left interest rates unchanged and issued a “cautious” statement as was expected. They closed by saying that “while the economic outlook is expected to warrant higher interest rates over time, some continued monetary policy accommodation will likely be needed to keep the economy operating close to potential and inflation on target.” The statement was cautious enough that it downgrades the risk for a rate increase in April and has a few economists pushing out forecasts for the next rate increase until the second half of the year.

The statement was very neutral for the Canadian dollar. The nod to needing “higher interest rates over time” meant it was not considered overly cautious and prevented a wholesale sell-off of the currency. It may not be enough.

The Canadian dollar is on the brink of an abyss. It has been flirting with 77 cents (to the US dollar) and a trade war could send it freefalling to 73.00 cents.

It will get some help from a slowing domestic economy. The BoC acknowledged in the policy statement that Q4 GDP growth was slower than expected. Export volumes, a barometer of growth, have been disappointing for several months. They got worse on March 7, when StatsCanada reported a drop of 4.0% in January.

Infrastructure issues have contributed to the widening discount for Western Canadian Crude oil, compared to the North American benchmark, West Texas Intermediate, which is trading at Canadian $33.66/barrel discount. That undercuts the benefit to the Loonie from rising WTI prices.

The recent rise in inflation may be illusionary due to the impact of minimum wage increases.

Christine Lagarde, Managing Director of the International Monetary Fund (IMF) said “In a so-called trade war, driven by reciprocal increases of import tariffs, nobody wins, one generally finds losers on both sides,”

The American’s are fully-aware of the negative implications of tariffs and are using national security issues to help Trump safe face. The White House said that Canada and Mexico may be exempted, late in the day on March 7.

Wise move. Full-blown economic sanctions would devastate global growth and have seriously negative repercussions for all involved, which makes the return of the tariff a truly Bizarre War.