By Michael O’Neill

The 2018 Vernal Equinox occurred on March 20th, heralding the arrival of spring. Vernal simply means “relating or occurring in the spring,” according to the Merriam-Webster dictionary. In days of yore, the Vernal Equinox was a big deal. It was a time for migration, celebration, and sacrifice. Today, not so much.

Federal Open Market Committee Chairman Jerome Powell may have marked the day in his way, albeit belatedly. He raised the “target range for the federal funds rate to 1 ½ to 1 ¾ %. With that news, some traders made money (celebrated), some lost money (sacrifice), others got fired (migration) The US dollar tanked.

Actually, the precipitous plunge in the US dollar had nothing to do with the rate increase and everything to do with the interest rate outlook for the rest of 2018.

Markets have been keying in on the Summary of Economic Projections that accompany a monetary policy statement, quarterly. Of particular interest is a “dot-plot” graph that depicts each member of the Committees forecast for interest rates for the balance of the current year, the next two years and then the “longer run.” In December, the “dots predicted three rate increases in 2018. The Fed has made the point,ad nauseam,” that future policy actions are “data dependent.” A slew of strong US economic reports and hawkish sounding comments from various FOMC members over the past few months fueled speculation that the March dot-plot forecast would predict four rate hikes in 2018.

It didn’t happen. The “dot plot” forecast for 2018 was unchanged. FX traders reacted by selling US dollars. They may regret that.

The statement and Summary of Projections were a long way from ‘dovish.” The FOMC raised interest rates. They upgraded GDP growth. They lowered the unemployment rate forecast. Furthermore, they raised rate hike forecasts for 2019 (from 2 to 3) and 2020 (from 1 ½ hikes to 2)

More than likely, the post-FOMC US dollar sell-off was due to a quick unwind of short term, long US dollar positions. Many traders expected easy profits if the dot-plot forecast predicted four increases this year. It didn’t happen. They bailed.

The FOMC is not dovish, merely cautious. The statement said “The economic outlook has strengthened in recent months. The Committee expects that, with further gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace in the medium term and labour market conditions will remain strong.”

Caution is warranted in the face of a possible trade war. The Trump Administration is preparing to levy upwards of $50 billion in new tariffs against China, as early as March 22. China is not impressed. Beijing said that “China will certainly take all necessary measures to resolutely defend its legitimate rights and interests,” One of those measures could be cutting imports of US soybeans. According to China, it wouldn’t have any major impact on them, but it would certainly hurt American farmers.

Even as the American’s are inflaming trade tensions with China and the Eurozone, there are signs that they are cooling their demands in NAFTA negotiations. On March 20, the Globe and Mail reported a break-through in the NAFTA talks. Quoting “sources with knowledge of the talks,” they said the US had taken its 50% auto content demand off the table.

That bodes well for the agreement. However, one has to wonder, that in the world of “give and take” negotiations, what will Canada have to concede? Supply Management boards, the dispute resolution mechanism or both.

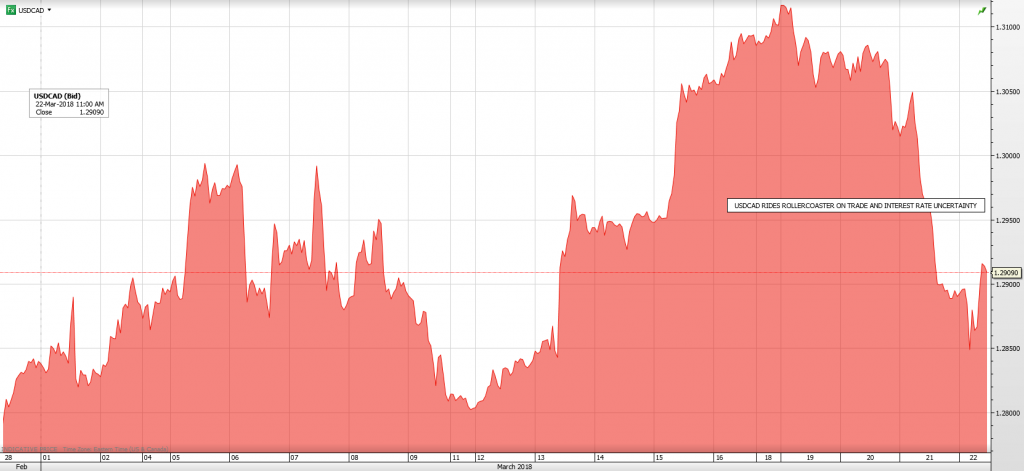

Chart USDCAD trading range since February

Source: Saxo Bank

The Canadian dollar was a huge beneficiary of the improved trade rhetoric and US interest rate outlook. USDCAD was flirting with the March peak of 1.3125 (76.20 cents) when the Globe and Mail story broke. Prices dropped to 1.2950 on the news and then fell another 0.0130 points to 1.2830 after the FOMC meeting. A move below 1.2790 may extend losses to 1.2500. (80.00 cents)

The prediction is not farfetched. Prices were at that level on Valentine’s Day. The catalyst for such a move would be a successful completion of NAFTA. It is very possible. The US appears motivated to close a deal before Ontario and Mexico elections and well ahead of the US mid-term elections in November.

A NAFTA agreement would go a long way in wiping the fog of the Bank of Canada’s crystal ball. The BoC cited trade policy developments as a “growing source of uncertainty for the global and Canadian outlooks.” An agreement would allow the BoC to refocus on the strength of the domestic economy and tighten policy.

The Vernal Equinox signaled the start of spring, but the prospect of interest rate uncertainty and fresh trade wars suggests Old Man Winter still has global markets in his cold, icy grasp.