By Michael O’Neill

Did the Bank of Canada (BoC) gift-wrap the Loonie, and hand it to FX traders? It sure looks that way. The BoC monetary policy statement of December 4 didn’t just announce unchanged interest rates, it may have hinted at plans to scrap lower rates altogether, or until late in the second quarter of 2020. At least that is how it seemed to traders. USDCAD plunged from 1.3275 to 1.3220 immediately afterwards and finished the day at 1.3200.

The December 4 policy statement was almost effervescent. Policymakers were pleased with their October projections for global economic growth. They also had an “eggnog glass-half-full outlook for the future, noting “nascent evidence that the global economy is stabilizing, with growth still expected to edge higher over the next couple of years.”

Photo: The spruce eats

The BoC noted that Canadian inflation is at target with “measures of core inflation around 2 percent, consistent with an economy operating near capacity.” Officials expect a temporary increase in inflation in the coming months, which suggests interest rates will remain unchanged.

The latest policy statement was in sharp contrast to the October 30 statement. It read a tad negatively as policymakers were concerned about “uncertainty associated with trade conflicts, continuing adjustment in the energy sector, and the unwinding of temporary factors that boosted growth in the second quarter.” They also expected that business investment would contract. Those concerns, like Mike Babcock’s coaching career, have been put on the shelf.

The statement did note that ongoing trade conflicts are the most significant source of risk to the outlook.

Equity markets rise and fall with every trade story or Trump tweet, but FX markets have, for the most part, avoided the distraction. AUDUSD traded in a 0.6755-0.6865 range for the past three weeks, and only managed to get back to the top of the range, December 4. That move had more to due with soft US data sparking US dollar sales on fears that US economic growth was slowing. NZDUSD gains were due to a less dovish than expected Reserve Bank of New Zealand policy stance and slowing US economic growth.

The Canadian dollar’s post-BoC policy statement rally entirely erased all the losses incurred after Deputy Governor Carolyn Wilkins speech in Montreal on November 19. Her address raised rate cut fears. She highlighted that the trade war caused a global slowdown and warned it created a “perfect storm.” Although she was emphasizing the resilience of the domestic economy, her remarks, had similar concerns as did the October 30, Monetary Policy Report, (MPR) which underscored downside risks to the economy. The Canadian dollar sank. Two days later, BoC Governor Stephen Poloz touted a rosier outlook, and the currency recouped some of its losses.

The latest Canadian dollar rally may run out of steam reasonably soon, and a US/China trade deal could be the catalyst. The Canadian dollar is the best performing G-10 currency, year-to-date, with a gain of 3.2%, and that occurred throughout the US/China trade drama. Its commodity currency bloc cousins, the Australian and New Zealand dollars, have lost 2.2% and 2.5% respectively. Which currency pairs are poised to derive the most substantial benefit from a resolution of the US/China trade war?

Canada is not in China’s good books. The new Chinese Ambassador Cong Peiwu said Canada’s arrest of Huawei Vice President Meng Wanzhou was arbitrary detention. He threatened that “very bad” damage” to Canada/China relations if Canadian politicians followed the US lead of sanctioning Chinese officials for human rights violations. China has demonstrated how they react when irked. They banned imports of Canadian canola and just recently lifted a ban on beef and pork imports. A US/China trade deal may lead to China increasing US agricultural imports at the expense of Canada. A trade deal is far better news for the Antipodean currencies than it is for the Loonie.

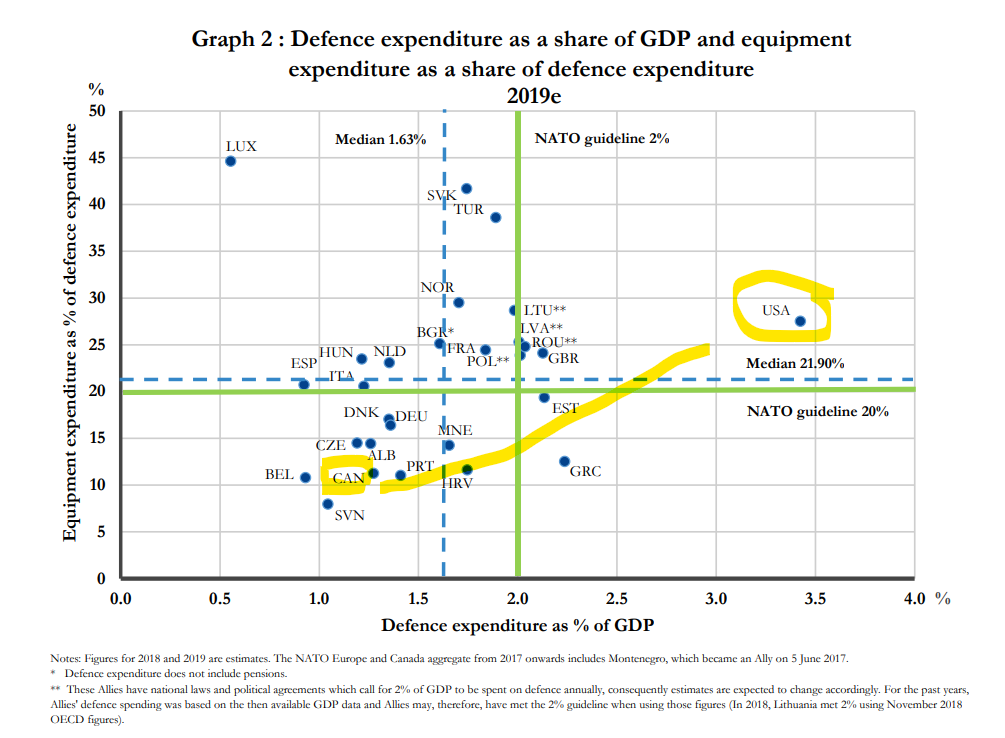

Canada may also have serious issues with the US. Prime Justin Trudeau just finished dodging a “black-face controversy, and he now finds himself accused of being “two-faced” by President Trump. The President was unhappy with video of Trudeau, French President Macron, and others, apparently mocking him during cocktail hour at Buckingham Palace. He was also annoyed by Canada’s failure to pay 2% of GDP to NATO. Trump is right. Canada consistently underpays. It is not a stretch to imagine the President using the weight of his office, to force Canada to pay NATO what they owe, especially after Trudeau embarrassed him. Tariffs anyone?

Graph: Canada and US NATO contributions highlighted

Source: NATO

West Texas Intermediate oil rose to $58.40/barrel December 4, two months after bottoming out at $51.15/barrel. Traders are hoping that a China/US trade deal will spur demand while expecting Opec to announce deeper and extended production cuts on December 5.

However, Canadian dollar gains have been marginal in part because of the $21.60/b discount between Western Canada Select and WTI.

The robust outperformance of the Canadian dollar in 2019, compared to the major G-10 currencies, suggests it may underperform at the beginning of 2020.

If the BoC did gift-wrap the Loonie, it may turn out to be for the benefit of Canadian dollar bears, not bulls.