By Michael O’Neill

Don Maclean started it. In 1971, he released a catchy tune titled American Pie, lamenting the “day the music died.” US Democrats attempted the first im-peach pie of the modern era when they started the process against President Richard Nixon in 1974. That pie was never baked. Nixon resigned before the House could vote. Republicans served Bill Clinton American im-peach pie on December 19, and he became the only American President impeached in the twentieth century. Mr Clinton was lucky. He was Impeached but not convicted. The Senate could not muster the 2/3’s majority vote needed to convict.

Will President Donald Trump be next? The process started on September 24 when Speaker Nancy Pelosi announced the House of Representatives would begin a formal impeachment inquiry into Mr Trump. She accused the President of violating the constitution alleging he used a foreign power to interfere with a political rival.

The news wasn’t a total shock to financial markets as there had been a lot of speculation ahead of the announcement. Still, Wall Street equity indices tanked, the US dollar plunged, and Treasury yields sank. Twenty-four hours later, to paraphrase Paul McCartney, “all those troubles seemed so far away. No one believes in yesterday.” Markets fully reversed the previous day’s moves.

US/China trade tensions may be starting to dissipate. President Trump deftly shifted market focus from the Democrat’s political maneuvering to prospects for improved global trade. He announced an initial trade agreement with Japan, saying it will open markets to $7.0 billion in US products. The Office of the US Trade Representative Fact Sheet noted “the agreement will eliminate or lower tariffs for certain US agricultural products. For other agricultural goods, Japan will provide preferential U.S.-specific quotas.”

Trump also hinted that a trade deal with China could happen “sooner than people think.” Both sides will meet in Washington in early October.

The FX market reaction to Trump’s trade comments demonstrates that volatility from negative US political headlines is short-lived. Traders prefer quantifiable economic data, central bank policy insight, and currently, verifiable US/China trade talk progress.

That is not the case in the UK. Data be damned. Politics and Brexit are the only game in town and with good reason. GBPUSD is vulnerable to a significant move, whatever the Brexit outcome. GBPUSD rallied on September 24, after the UK Supreme Court ruled that Boris Johnson’s proroguing of parliament was illegal. At the time, traders believed the ruling reduced the risk of the UK leaving the EU without a deal. MP’s have passed a bill which forces the government to seek an extension to the October 31 deadline. However, a “no-deal Brexit” is still a risk. The British need unanimous approval from the 27 EU nations for an extension and more than a few countries are tired of the drama. GBPUSD fully reversed the post-court ruling rally.

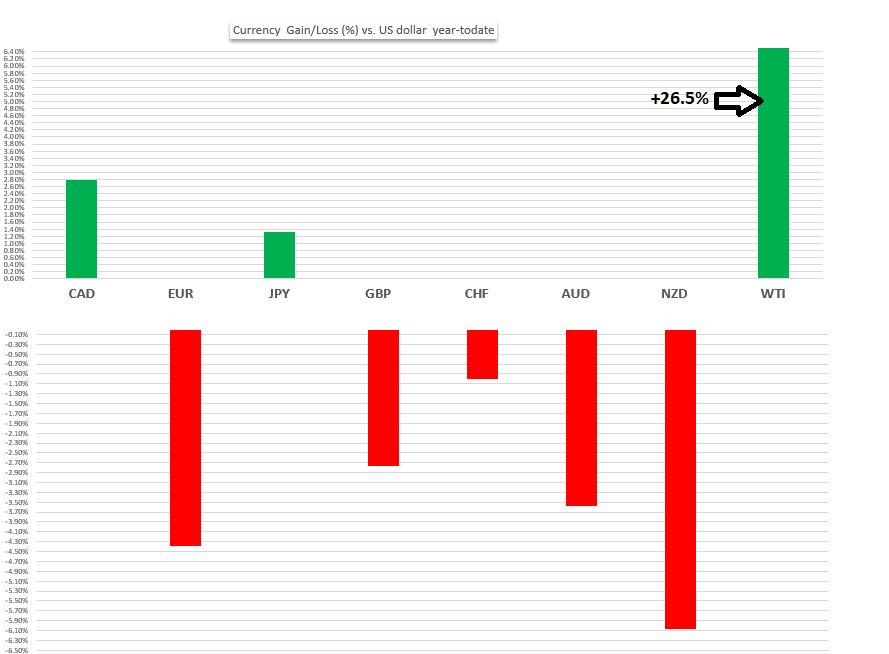

FX markets are heading into the final quarter of 2019. The Canadian dollar is the best performing major G-10 currency, this year, despite all the global turmoil. The Japanese yen is the only other major currency to rise, benefitting from its status as a safe-haven. The New Zealand dollar is the worst-performing currency followed by the Euro and Australian dollar. The Loonies outperformance is easily explained. The Bank of Canada has not cut interest rates. The others have. The Reserve Bank of New Zealand lowered its overnight rate by 0.75% and its Australian counterpart trimmed rates by 0.50%. (They could cut again, next week) The European Central Bank (ECB) cut their benchmark deposit rate deeper into negative territory and embarked on a new round of quantitative easing.

Chart: Change in US dollar vs major currencies-year-to-date

Source: Saxo Bank/IFXA

The Bank of Canada may continue to stand pat, thanks to upside surprises to some recent economic data. Also, core inflation sits at the BoC target of 2.0%, nationwide housing prices have stabilized, and consumer sentiment is still at elevated levels. On September 4, the BoC said, “Canada’s economy is operating close to potential and inflation is on target.” They admitted “trade uncertainties” were taking a toll on the domestic economy. Those trade uncertainties have diminished in the past few days, which reduces the BoC incentive for lower rates. Continued US and China progress on the trade front, will support a steady BoC policy outlook. That suggests continued Canadian dollar outperformance, at least against the commodity bloc currencies.

The US stock market continues to flirt with record highs, although fears of a looming recession waft through markets. The US dollar is rising against the currencies where the central bank has cut interest rates. Treasury yields are plumbing their lows. Oil prices gave up their gains after the drone strike on Saudi Arabian oilfields, but the risk of open warfare against Iran, is underpinning prices.

Year-end is fast approaching. The Dow Jones Industrial Average is up 15.4% year-to-date. The US dollar has solid results against five of the seven-major G-10 currencies. Bond, oil, and gold prices have healthy gains. Soon, traders will be looking to lock in those profits for year-end. Wall Street traders are well-aware of the nasty surprises that have often occurred in the last quarter.

American Democrats will be singing “American Im-peach Pie” even as “good ole boys” book profits while “drinking whiskey and rye.”