By Michael O’Neill

You know you are in for a “snow job” when the Finance Minister’s opening statement to a fiscal update is a weather report. Chrystia Freeland began her speech with “We know the winter ahead will be hard. It will be a winter of loneliness and grief, for far too many families. But we also know that spring will follow winter.”

Unfortunately, that was probably the most accurate statement in the 237 page tome titled “Supporting Canadians and Fighting COVID-19.

The federal government spent $490.7 billion to fight the virus, composed of $322 billion in direct measures, $85 billion in tax deferrals and $83.4 billion in credit support. Those numbers are substantially higher than the government’s projection of a $381.6 billion short-fall for 2020. It’s probably a function of new math, so no worries.

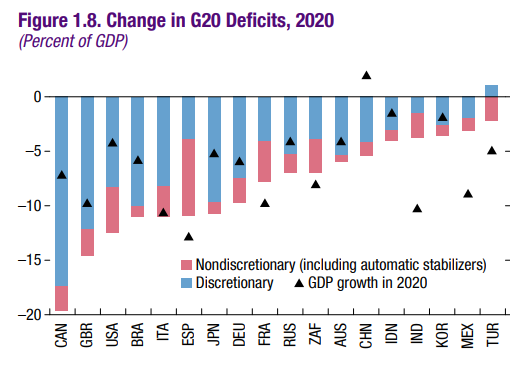

The government was already $30 billion in the hole as of February, which Ms Freeland described as going into the crisis with “a strong fiscal position.” The “strong fiscal position” is no more. Canada’s financial position deteriorated the most of any developed market economy, according to the IMF October Fiscal Monitor.

Source: IMF October Fiscal Monitor.

Even more alarming is the somewhat cavalier approach to spending. Just last year, critics were wailing about the governments 30 billion dollar deficit and its impact on Canada’s ability to fund social programs. Today, $30 billion is a rounding error. Ms Freeland said as much. She noted “ Once the virus is under control, the Government of Canada will invest in a growth plan of roughly three to four per cent of GDP, between up to $70 and $100 billion.” That’s a $30 billion gap.

Politicians used to be cognizant of debt to GDP ratios. Most of them realized that high numbers were “bad” and that anchored their spending plans, helping to prevent massive deficits. Not in Canada! It’s “anchor’s away-bring on the guardrails.”

The government spending frenzy will continue unabated until it hits “fiscal guardrails,” which include the employment rate, total hours worked, and the level of unemployment in the economy. She didn’t say anything about inflation. And inflation is going to be a problem. Certainly, house price inflation.

New Zealand Finance Minister Grant Robertson said the government was reviewing policies relating to the housing market with an eye on getting the Reserve Bank of New Zealand to help stabilize sharply rising property prices. The RBNZ’s really only has one weapon to do so, and that is to raise interest rates.

It isn’t any different in Canada. The average price of a Canadian resale home rose 15% for the year ending October. The largest gains were seen in Quebec, Nova Scotia, and PEI, which rose between 19.5% and 20.27%.

It’s no wonder prices are soaring. Ratehub.ca lists 5-year mortgages from 1.44% to 1.84%, as of December 1. That makes an $800,000 home affordable for a family with a combined income of $150,000 and a $75,000 down payment. However, a 2% rise in mortgage rates changes the outlook dramatically, while a 5% increase would be catastrophic for many.

It can happen. It has before, and history tends to repeat itself.

The major central banks are struggling with how to boost inflation levels. Economics 101 taught that when interest rates go down, inflation rises. Economics 2021 is teaching you to forget whatever you learned in Economics 101.

The US Fed is leading the charge. They have scrapped targeting a specific inflation level and now will only react if inflation rises above an average rate for a considerable period of time. What they are really saying is that they cannot control inflation, in any direction. So, how will they control a spike higher?

Let’s assume that the availability of a COVID-19 vaccine sparks a robust global economic boom in 2021. Air travel returns to pre-pandemic peaks as previously shut-in Marco Polo types fuel their wanderlust. Hotels, resorts, and cruise ships are crammed to capacity and finding space becomes exceedingly difficult. Restaurants and bars are packed, in a spending frenzy fueled by government stimulus measures, aid packages and an employment rebound.

If that happens, there is zero chance that prices are going down.

In fact, businesses will be looking to recoup their COVID-19 losses, and employees will want to recoup lost wages.

Statistic’s Canada says Canadian inflation only rose 0.7% year over year in October. They also said food and vegetables rose 9.5% between September and October, meat prices rose 1.7% year over year, building materials and new houses rose at their fastest pace in 14 years. If you lived in Ontario, and heated year home with natural gas, it cost you 11.6% more than it did in September. StatsCan and the Bank of Canada say inflation is low.

Your bank account begs to differ.

Not so for the Governments bank account. Under the new stealth MMT (Modern Monetary Theory) that appears to have been adopted, billions just represent numbers from 1-9 followed by a string of zeros. Elementary arithmetic class taught that the numbers 1-9 are small, and zeros were nothing. Obviously, the Finance Department believes a billion is just a small number trailed by a string of nothings, so why worry?

If massive government stimulus spending stokes a surge in inflation, the latest fiscal snow job will bury Canadians and the currency in an avalanche of woe.