By Michael O’Neill

It’s common knowledge that poking a bear rarely ends well for the person wielding the pointy stick. Five hundred pounds of fury, fangs, and claws can quickly make short work of any foolhardy intruder.

“Ouch—That Hurt”

Canadian dollar traders might soon find themselves in their own “poke-the-bear” scenario, especially if the September 6 nonfarm payrolls report delivers another grim American employment picture. Job creation has been on the decline since May, while the unemployment rate has jumped from 3.8% in March to 4.3% in July. Fed Chair Jerome Powell has clearly pivoted from an inflation-fighting stance to a focus on maximum employment. This shift follows a year-over-year 2.9% drop in US CPI, continuing the downward trend that began in March and placing inflation squarely within the Fed’s target range.

“I Didn’t See That Coming”

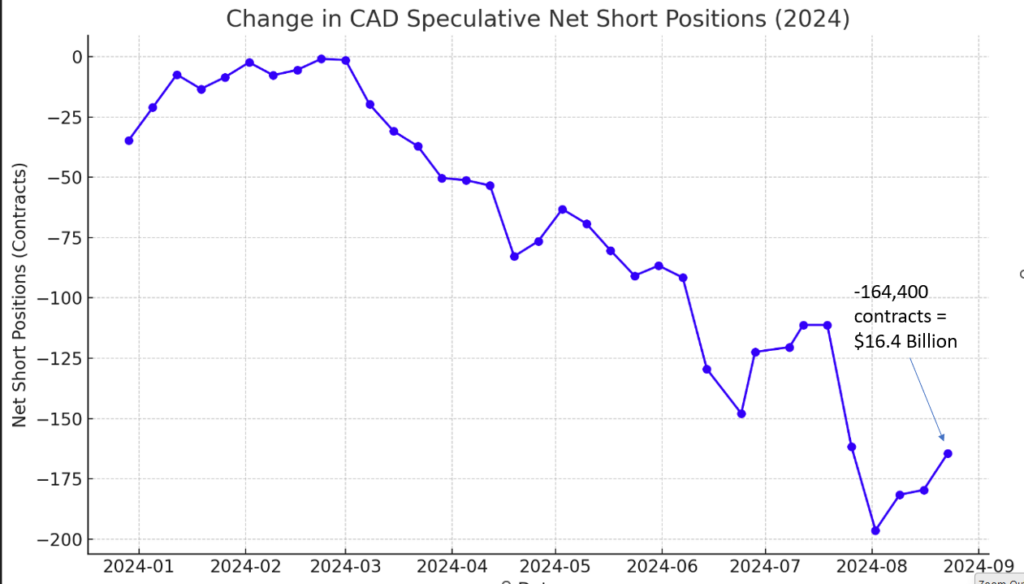

The chart below shows that traders had been steadily increasing their bets against the Canadian dollar since the beginning of the year. They began trimming positions after reaching an all-time high of -196,300 contracts (CAD$19.6 billion) on August 2, but they still hold a $16.4 billion short CAD position (US$12.2 billion at 1.3460) as of August 23. This remains an extreme position, given that the average Commodity and Futures Trade Commission (CFTC) short CAD position has been around 57,200 contracts since 2010.

The Fed’s pivot, though well-signaled and widely expected, seems to have blindsided the speculative Canadian dollar community.

Source: Commitment of Traders

“The Boat Tipped”

FX trading and boating share a few risks, with overcrowding being one of the most perilous. Imagine an overloaded sight-seeing boat crammed with tourists eager for an afternoon of shark watching. If a Great White appears on the starboard side and everyone rushes to the rails, they risk becoming chum if the vessel capsizes.

The FX market isn’t much different. An overcrowded short position can unravel in a flash if sentiment shifts, forcing traders to stampede for the exits. This can drive a currency—like CAD—sharply higher in a swift, feeding-frenzy-like correction.

Start Bailing

It could already be underway. US monetary policy is the key driver of currency movements, and Fed Chair Powell is the maestro orchestrating it all. His speech at the Jackson Hole symposium was unmistakably dovish, effectively announcing the start of a new US monetary easing cycle on September 18 with the first rate cut since March 2020.

The CME Group FedWatch tool currently shows a 65.5% chance of a 25-bp cut, while 34.5% of traders are betting on a 50-bp reduction. Citibank Research head Lucy Baldwin is in the latter camp. On August 28, she reiterated Citibank’s expectation of a 50-bp rate cut in September, followed by another 75 bps by year-end. If the September 6 nonfarm payrolls report disappoints, sparking renewed US dollar selling, Baldwin’s prediction could hit the mark. This would likely boost the Canadian dollar on the back of broad US dollar weakness, with the move supercharged as traders scramble to unwind short CAD$ positions. That could be the final nail in the coffin for Canadian dollar bears.

Over-reactions Are the Norm

What do social media and parents at minor league sporting events have in common? Over-reaction. Someone tweets an well-meaning “thoughts and prayers” message after a disaster or personal tragedy, and the vitriol floods in like a tsunami within minutes. Little Johnny taps the ball off the tee, it dribbles down the first base line, and a chorus of parents screams, “Run!” as if the field was on fire. FX markets are notorious for over-reactions too. Just look at how quickly moves are reversed after surprising data releases. The Canadian dollar is particularly prone to this over-reaction phenomenon. A weaker-than-expected US employment report on September 6 could send USDCAD crashing below major support at 1.3360 and all the way down to 1.3000 in a heartbeat as $12.2 billion worth of US dollars scramble to find buyers.

Silver Linings

The outlook may seem bleak, but it’s far from certain. A 50-bps rate cut in September would likely spark a storm of outrage, with Donald Trump at the forefront, accusing the Fed of meddling in the election. That might push Mr. Powell to assert the Fed’s independence by avoiding the political fray and opting for a more modest 25-bps cut.

But the real question now isn’t whether the Canadian dollar bear is in peril, but whether it’s facing a minor scratch or a deep, gouging wound.”.