“Every Who down in Whoville liked Christmas a lot…But the Grinch at the Federal Reserve did not!”

Raising interest rates by 50 bps eleven days before Christmas is hardly in keeping with the spirit of the season. Nevertheless, that is exactly what the Fed did on December 14 when they increased the fed funds rate to 4.25-4.5%.

Fortunately, almost no one was surprised since many policymakers tacitly preannounced the outcome in speeches after the previous FOMC meeting.

Analysts and traders expected a dovish outcome from this FOMC meeting. Two consecutive lower than expected inflation reports stoked speculation the Fed would hint that interest rates were near to the peak for this cycle.

Fed Chair Jerome Powell stuffed coal in that stocking.

Photo: Etsy

He said about interest rates, “we still have some ways to go.” He also said that the more important question is not “the speed of rate hikes” but how “long the Fed will remain restrictive.”

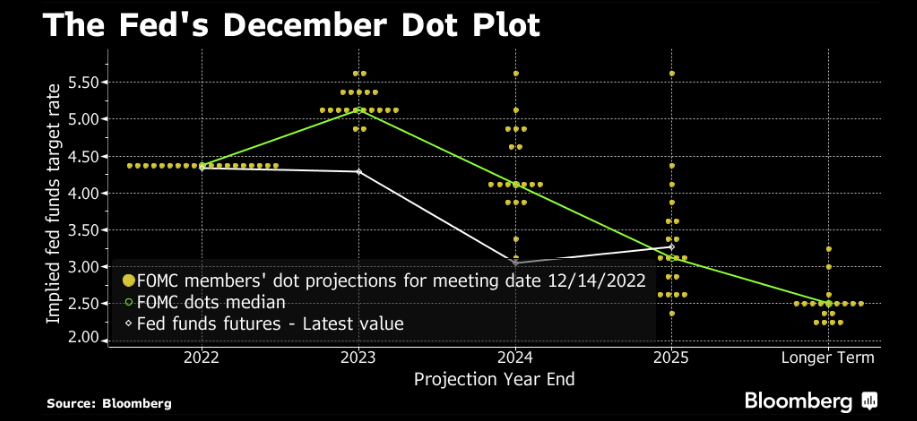

The Summary of Economic Projections (SEP) reinforced the hawkish bias. Policymakers see growth slowing to just 0.5% in 2023 (previous forecast 1.2%) higher inflation (forecast Core PCE 3.5%, September 3.1%) and higher unemployment (4.6% vs September 4.4%).

The FOMC also raised its estimate for Fed funds to 5.1% in 2023 from the 4.6% they expected in September. They also raised the 2024 estimate to 4.1% from 3.9%.

Source: Bloomberg

The market reaction is a cross between “you’re kidding, right? and “why should we believe you, your forecasting sucks.” Or else it may be due to everyone watching France beat Morocco 2-0 in the World Cup semi-final.

The Dow Jones Industrial Average and the S&P 500 index closed with small losses while the G-7 major currencies are little changed from their levels immediately prior to the FOMC statement. The exception is the Japanese yen which fell despite a slide in the US 10-year Treasury yield from 3.561% pre-FOMC to 3.46% at the close.

The Fed meeting also served to shift the holiday season into high gear. Those who have not booked holidays will be enjoying early and long lunches as many businesses have closed the books on 2022.

The new year is just the old year with a fresh coat of pain.

Risk sentiment will continue to dance between positive and negative with doves expecting incoming data to convince the Fed of the error of its ways. The doves expect to see rising global growth from China accelerating its reopening from Covid-zero policies, which will alleviate supply chain pressures and support lower prices. Many of them also believe in Santa Claus.

The negative sentiment camp is spooked by the Russian war in Ukraine, the lack of a nuclear treaty with Iran, and North Korea’s penchant for firing long range missiles willy-nilly.

Russian President Putin is sounding more unhinged with every speech. On December 9, while talking about nuclear weapons, he said, “As for the idea that Russia wouldn’t use such weapons first under any circumstances, then it means we wouldn’t be able to be the second to use them either — because the possibility to do so in case of an attack on our territory would be very limited.”

Oil prices are another wild card. Opec is not thrilled that even after cutting production in October, oil prices remain depressed. The cartel is hoping for prices in the $90.00/barrel level, and they have not ruled out further cuts. It is not a stretch to say that renewed Chinese demand for crude will boost prices which will help limit inflation declines in the short term.

The Canadian dollar managed to squeeze out a gain in the post-FOMC world and it has the possibility to extend those gains further.

The Fed and Bank of Canada (BoC) benchmark rates are the same (4.25%), but the BoC hinted that further rate cuts may not be needed. Mr Powell said no such thing and the SEP forecasts predict another 75 bps of hikes in 2023.

BoC Governor Tiff Macklem said he is trying to balance the risks between over and under tightening.

He said If we raise rates too much, we could drive the economy into an unnecessarily painful recession and undershoot the inflation target. If we don’t raise them enough, inflation will remain elevated, and households and business will come to expect persistently high inflation. With inflation running well above target, this is the greater risk.”

That is enough to limit USDCAD downside to the 1.3350-1.3400 area.

Mr Powell may be the Grinch who stole Christmas, and his heart is not growing three sizes at all.