The Bank of Canada ladled up a hearty bowl of porridge on Wednesday. Their recipe was not the Martha Stewart version of steel cut oats; one made with a cinnamon stick and finished with a banana and dates and a delicious way to start the morning. Instead, theirs was an instant oatmeal dish that was zapped in a faulty microwave for two minutes. The Stephen Poloz oatmeal was unevenly cooked, overdone in some places, raw in others and essentially an inedible glob of gruel that appealed to no one.

As expected, the Bank of Canada (BoC) left interest rates unchanged and then deftly danced around a definitive outlook. The interest rate statement and the Monetary Policy Report were studies in contrasts.

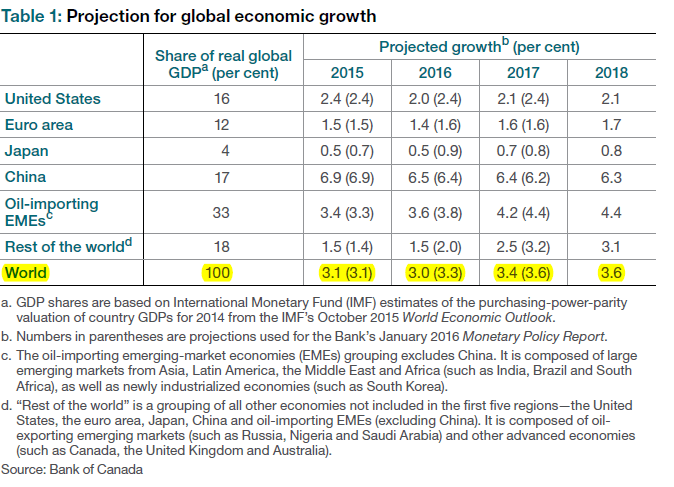

The BoC trumpeted that growth in the global economy was strengthening to 3% in 2016 and then admitted that the forecast was downgraded from January’s outlook.

They said that, after a slow start in 2016, “the US economy is expected to regain momentum” then offset that positive by adding “but with a lower profile and a composition that is less favourable for Canadian exports”.

They noted that prices of oil and other commodities were off their earlier lows and even slightly above the levels that the BoC assumed in January. Then they pointed out that “the Canadian economy’s complex structural adjustment to the oil price shock is ongoing and will dampen growth throughout the Bank’s projection horizon”.

The glass half-empty-half-full routine continued throughout the statement. Most telling was that the BoC admitted that: the combination of “global and domestic developments would have resulted in a modest downgrade to the Bank’s outlook “It could be good or it could be bad” except for the federal government’s fiscal stimulus.

Despite all of the above, the financial press headlines were mostly positive noting that the BOC raised their forecasts for 2016 GDP growth to 1.7% (January was 1.4%) and trimming 2017 GDP growth to 2.3% (January 2.4%).

Even as the BoC was changing its GDP growth forecasts, the International Monetary Fund (IMF) was doing the same thing, except the IMF lowered their prediction for 2016 GDP, to 1.5% from 1.7%. So there you have it.

The Canadian economy will either grow or shrink this year.

Wednesday’s BoC interest rate statement and MPR were eagerly anticipated. Financial markets were expecting a bit of clarity on the Bank’s view of the economy following a string of very strong economic reports. They were disappointed. All they got was more baffle-gab disguised as a balanced view.

The BoC didn’t provide any additional insight into the short term direction of the Canadian dollar. Numerous references to downside risks to the outlook may have been very subtle verbal intervention although that conclusion may be a bit of a stretch.

Nevertheless, if the Bank of Canada is unwilling to provide currency direction, Opec or the Fed may rise to the challenge.

Oil prices have been on a tear since the first reports that Russia and Opec (particularly Saudi Arabia) were discussing a production cap back in February. Those rumors and reports have culminated in a meeting in Doha, Qatar on the weekend.

Tuesday, Interfax reported that Russia and the Saudi’s had agreed to a deal regardless of Iran’s participation and WTI probed the $42.50/b area. Traders were bullish.

On Wednesday, the oil market got what should have been very negative news. The Energy Information Administration (EIA) reported that US Crudes Stocks inventories rose 6.634 million barrels from the previous week confirming the American Petroleum Institute result the day before. In addition, Opec cut its forecast for global oil demand in 2016. It was only 50,000 barrels/day but it was due, in part, to concern about economic developments in China and Latin America.

Oil traders essentially ignored the news as WTI only slipped $1.00, even though it was trading at prices not seen since December. That may be a case of the facts getting in the way of a good story.

Opec and Russia are essentially fixing prices, a practice that is illegal in the Western world. Canadian, American, British and French producers will not be participating in production caps or cuts. Neither will Iran.

A slowdown in demand and a splintered Opec is not a recipe for higher oil prices which may lead to a quick drop in WTI and a higher USDCAD.

Stephen Poloz, Governor of the Bank of Canada was following a similar script as the one Fed Chair, Janet Yellen used in March, in his remarks at the MPR press conference. He erred on the side of caution despite a recent string of strong data releases.

Ms. Yellen was overtly doveish in the face of improving US data while a number of her colleagues were telling a fairly hawkish tale. The Fed chair’s doveish stance sparked a major US dollar sell-off in March and the dollar has not recovered.

Politics is also playing a role, at least in the timing of a US move. The Presidential election is Tuesday November 8th which arguably, removes the September 21th and the November 2 meetings as possible rate hike meetings (assuming only two hikes in 2016) in order to avoid any appearance of impacting the vote. The April 27 meeting is probably too close to the March meeting for Ms. Yellen to turn hawkish from doveish. That leads June 15 as a prime candidate for the first rate hike of 2016 and something that would be bullish for USDCAD.

The Bank of Canada’s principle role may be “promoting the economic and financial welfare of Canada” but for the time being, it is Opec and the Federal Reserve that are really in charge.

By David Marks, Agility Forex Analyst