By Michael O’Neill

The world’s major central banks are at a loss to explain low inflation and low economic growth with any degree of confidence. Their recent policy statements cite a litany of risks for their economic malaise, but the common denominator in their assessments is China.

European Central Bank President (ECB) Mario Draghi didn’t come right out and blame China for his view that euro area growth risks were to the downside. He was a tad subtle. During his April 10 press conference following the ECB meeting, he characterized the risks as “uncertainties related to geopolitical factors, the threat of protectionism and vulnerabilities in emerging markets.” The “threat of protectionism” is a not so veiled reference to the ongoing China/US trade war and America’s threat to levy tariffs on eurozone aircraft imports.

The Federal Open Market Committee (FOMC) members were more specific about US economic risks. The minutes of the March 20 meeting underscored concerns about ongoing trade talks, Brexit and dangers from a worse than expected slowdown in Europe and China.

Reserve Bank of Australia Deputy Governor Guy Debelle explicitly said that slowing growth in China and the escalation of trade tensions were key factors in lower global growth.

The Bank of Canada monetary policy statement of March 6 cited a more pronounced and widespread slowdown in the global economy for keeping domestic interest rates below their “neutral” range.

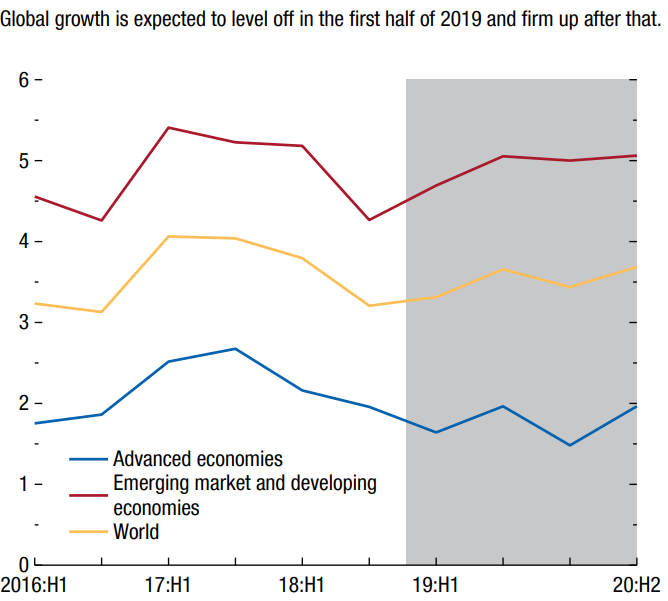

The International Monetary Fund (IMF) quantified the central banker’s global growth fears. They slashed their 2019 global economic growth forecast to 3.3% from 3.6% in the April World Economic Outlook, blaming a slowdown in China for increased trade tensions with America.

Central bankers are unanimous in their views that slowing China growth is behind the downturn in the global economic expansion.

Source: IMF World Economic Outlook April 2019

It’s not all China’s fault. The blame for a large part of China’s growth issues rests on the doorstep of the Whitehouse.

President Trump has carpet-bombed friends and foes with punitive trade tariffs in a strategy using access to the American consumer to bend foreign nations to his will. It is working. Canada and Mexico caved to US demands and Canada still suffers from US tariffs on imports of Canadian steel and aluminum despite the new US- Mexico- Canada Agreement on trade. (USMCA) The USMCA deal didn’t stop him from threatening to close the US/Mexico border entirely, during one of his “build me a wall” rants.

The President tweeted a grenade at the European Union. On April 9, he wrote: “The World Trade Organization finds that the European Union subsidies to Airbus has adversely impacted the United States, which will now put Tariffs on $11 Billion of EU products! The EU has taken advantage of the U.S. on trade for many years. It will soon stop!”

Mr Trump may find this opponent to be more formidable than any of the others. The EU countries are America’s number one export market. The Office of the US Trade Representative said that trade of goods and services between the EU and the US totaled $1.1 trillion in 2016, supporting an estimated 2.6 million jobs. Trump likes to exert leverage, and he doesn’t have much to exert against the EU. Arguably, this trade war may be a non-starter.

Trump’s tariff strategy may have worked with China, though. Treasury Secretary Steven Mnuchin said he had a productive meeting with Chinese Vice Premier Liu He on April 10, He said they have “pretty much agreed to a trade deal enforcement mechanism,” which raises the odds of a trade agreement before the end of April.

ECB President Mario Draghi seems to have summed up the mood of the global central bankers in four words. He described his eurozone outlook as “continuing confidence with increasing caution.”

FOMC members expressed a similar view. The FOMC minutes of April 10 said “members continued to view sustained expansion of economic activity, strong labour market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcomes for the U.S. economy in the period ahead.

The Bank of Canada was more forthright with its thoughts about the benefits of a US/China trade agreement. They wrote, “It is difficult to disentangle these confidence effects from other adverse factors, but it is clear that global economic prospects would be buoyed by the resolution of trade conflicts.”

Oil traders may have jumped upon the trade deal bandwagon early. Oil prices have soared over 50% since Christmas and 18% in the past month. Most of the gains are a result of Opec supply cuts, and US sanctions on Iran, however, improving prospects for a rebound of global growth have also underpinned prices.

The oil price surge continues to provide a degree of insulation for the Canadian dollar against adverse US dollar moves.

A US/China trade deal would jumpstart global growth, and if so, Blame it on Beijing.