Photo: Marvel

By Michael O’Neill

Yes Victoria, there is a Thunder god, and his name is Tiff Macklem.

Stung by criticism that the Bank of Canada bungled its most critical function of using monetary policy to keep inflation low and stable, the BoC Governing Council put the hammer down.

They hiked the overnight rate by one hundred basis points or 1.00%. It is an aggressive move designed to front-load rate increases to prevent inflation from becoming entrenched.

It’s a good first step.

Mr Macklem said that more people were getting worried that inflation is here to stay and stressed “we cannot let that happen.”

He also said the Canadian economy was overheated, blaming goods, services, and worker shortages for rising prices.

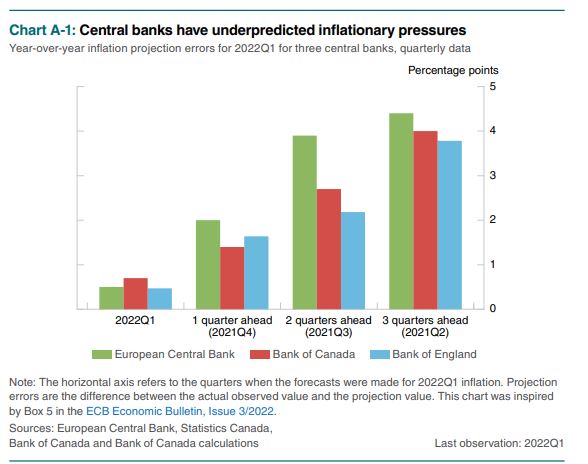

David Reevely from The Logic asked the Governor to explain what the BoC learned after it published forecasting errors in the Monetary Policy Report. The question wasn’t popular, and Mr Macklem handed it off to Deputy governor Carolyn Rogers.

She was defensive. She said the BoC has been very clear that the forecasting environment was difficult. “We were in a pandemic. We are in a war.” The combination of the two events doubled the difficulty in forecasting.” The short answer is “it’s a teaching moment.”

Chart: Central Bank forecasting errors. The chart is a tad confusing as it merely shows what the BoC, BoE and ECB predicted for inflation, but it doesn’t show how badly they miss-guessed.

Source: BoC MPR

The BoC downgraded its 2022 growth prediction to3.5% from 4.2% in April while boosting its 2022 inflation guess to 7.2% from 5.3%.

While impressive, the 1.00% rate hike just brought the overnight rate into the middle of the BoC neutral policy rate band of 2-3%.

It’s not enough to lower inflation, and the BoC said as much.

“The Governing Council continues to judge that interest rates will need to rise further, and the pace of increases will be guided by the Bank’s ongoing assessment of the economy and inflation. Quantitative tightening continues and is complementing increases in the policy interest rate.”

The statement also described the rate hike as being “front-loaded” which suggests rate hikes in September and October will be in the 0.50-0.75% range. It wouldn’t be much of a stretch to believe the year will end with the overnight rate at 4.50%.

Will the rates tame inflation. Not at current or even at projected year end levels.

The BoC went to great lengths to blame supply chain disruptions, lingering fallout from the pandemic, the war in Ukraine, and high commodity prices for the surge in inflation. They are not wrong, but it is difficult to see how a Canadian rate hike will have any impact on those issues.

If inflation is a problem in Canada, the US is in dire straits. Tiff Macklem may be on the “missed-the-boat-on-inflation team, but Jerome Powell is the captain. The Fed Chair is the monetary policy maestro for the global economic orchestra, and he has been conducting the music from the deck of the RMS Titanic.

Source: Historic UK.com

The July 13 US inflation reading may be Mr Powell’s “come to Jesus” moment.

US CPI soared 9.1% y/y in June and 1.3% m/m. The results were well above forecasts and left no doubt that the Fed will need to respond aggressively. The CME Fedwatch tool has the probability of a 1.00% Fed rate hike on July 27 at 60.0%.

That shouldn’t be good news, but if so, it’s not reflected in FX, bond, or equity markets. The US dollar has given back all of its post-CPI gains, while the S&P 500 index turned a 1.25% loss to a minor positive by mid-day. Bond traders do not seem to fear higher US rates. The yield on the 10-year Treasury fell to 2.91% from 3.05% in the morning. The US dollar gave back all of its inflation gains as well.

Those moves are probably wrong and more a reflection of profit-taking in thin summer markets.

In reality, it makes zero sense to believe that rapid and aggressive Fed rate hikes will not drive the US and the global economy into a recession.

The International Monetary Fund (IMF) agrees. IMF Managing Director Kristalina Georgieva wrote in a blog that the upcoming World Economic Outlook will downgrade global growth in 2022 and 2023. She noted that there was an increased recession risk for 2023.

USDCAD direction has been dictated by risk sentiment as reflected in S&P 500 price action. There is no reason to think things will change in the second half of 2022. If so, USDCAD will continue to trade with a bullish bias, especially if recession fears drive WTI oil below long term support at $75.00/barrel. And that is also inflationary, as a weak Canadian dollar means higher prices for imports. It will also turn the Federal government’s “fiscal anchor” into a fiscal albatross.

The BoC slammed the hammer at inflation, but the Canadian dollar may be the thumb to the inflation nail.