Source: Bing AI

It’s vacation time in Canada. School’s out, and families have hit the road, enduring the familiar backseat refrain, “Are we there yet?”

For Tiff Macklem and the governing council of the Bank of Canada, the question is different: “Are you broke yet?” If not, just wait a few months.

The Bank of Canada hiked its benchmark rate by 25 bps to 5.0%,on July 12, continuing its fight to lower inflation to the targeted level of 2.0%. Mr. Macklem cited several reasons to justify the increase, including the persistence of underlying inflationary pressures, the need to slow demand growth in the economy through higher interest rates, and the tight labor market.

Canadians just shook their heads and joined Aerosmith in singing “It’s the same old story, same old song and dance.”

And for good reason. BoC communications have repeated the rate hiking rationale since the first hike in March 2022 and continuing into January 2023 followed by a period of inaction until June. Then, they raised the overnight rate to 4.75%, always accompanied by the excuse that things didn’t unfold as expected.

Is inflation the problem, or is it the Bank of Canada’s actions, forecasts, and guidance that pose the real issue?

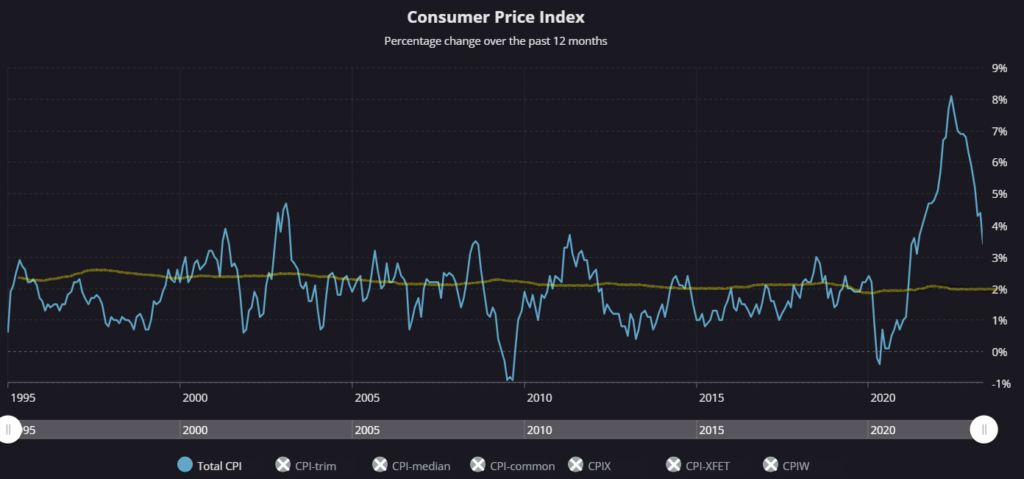

Let’s begin with the inflation target. In the late 1970s and early 1980s, high inflation plagued Canada, with the CPI rising to 12.5%, while the US experienced 13.5% inflation. Fed President Paul Volcker responded by raising the Fed Funds rate to 19% in June 1981, while Bank of Canada Governor John Crow raised the Bank Rate to 21% in August 1981.

To avoid a repeat of such an episode, central bankers worldwide incorporated inflation targeting into their monetary policies. This involved setting specific inflation targets and utilizing monetary policy tools to achieve and sustain them. The chosen target was 2.0% because the Federal Open Market Committee (FOMC) believed it was most consistent with the Federal Reserve’s mandate for maximum employment and price stability. The Bank of Canada adopted a 2.0% inflation target within a 1-3% range in 1991.

Central bankers also recognized the need for transparency, leading to the use of forward guidance to manage long-term interest rates, financial conditions, and inflation expectations.

Financial turmoil is not uncommon, as it is an inherent part of market dynamics. Since the adoption of inflation targeting, numerous events have caused economic distress and instability, including the Savings and Loan crisis in the early 1990s, the Asian Financial crisis of 1997-98, the dot-com bubble burst in 2000, the 9/11 terrorist attack, and the Global Financial crisis of 2008.

However, the current situation is different. While previous events had significant impacts confined to specific regions, the COVID-19 pandemic has had a truly global impact, devastating major economies worldwide. To compound matters, the situation was further worsened by the Russian invasion of Ukraine.

Central bankers shifted their focus from inflation to ensuring financial system stability and sufficient liquidity. They largely succeeded in this aspect. However, they lost sight of the importance of maintaining price stability. The Bank of Canada failed to react promptly to rising inflation and was subsequently forced to raise interest rates in 10 out of the last 12 monetary policy meetings.

Now, inflation rates are falling, but not at the desired pace for the Bank of Canada, leaving the door open for additional rate increases.

The Bank of Canada remains fixated on achieving a 2.0% inflation target, even though their website indicates a target within a 1-3% inflation-control range. In theory, they could aim for 3.0% while still meeting their mandated range.

Source: Bank of Canada

It appears that the Bank of Canada may be overcompensating for its previous failure to address rising inflation by stubbornly raising rates in a declining inflation environment. Their forecasting track record over the past year has been poor, and combined with Mr. Macklem’s tendency to provide misguided advice to consumers, today’s monetary policy statement is better suited as kindling than as guidance.

Governor Tiff Macklem is going for broke on the inflation front and unfortunately, his actions mean Canadians are just going broke.