Photo: iJDMToy.com

By Michael O’Neill

A popular metaphysics question is, “if a tree falls in the forest and no one is around to hear it, does it make a sound?”

Bank of Canada Governor Tiff Macklem may be having his own metaphysical dilemma. “If a central bank hikes interest rates and no one cares, does it mean anything?”

If the reaction to the latest 75 basis point rate hike is a guide, then the answer is “No!”

USDCAD barely budged despite being within spitting distance of its 2022 peak. The TSX Composite Index dipped but quickly recovered as traders took their cue from Wall Street. The 10-year Government of Canada bond yield ticked lower, tracking a similar move in the US 10-year Treasury yield. Ho-hum.

The BoC increased its benchmark overnight rate from 2.50% on July 13 to 3.25% on September 7. The move takes monetary policy from “neutral” to “restrictive.” The Bank does not plan to stop at this level but said, “Given the outlook for inflation, the Governing Council still judges that the policy interest rate will need to rise further.”

The BoC justified the rate hike by saying, “The Canadian economy continues to operate in excess demand, and labour markets remain tight. Canada’s GDP grew by 3.3% in the second quarter. While this was somewhat weaker than the Bank had projected, indicators of domestic demand were very strong – consumption grew by about 9½% and business investment was up by close to 12%.”

The statement also noted that “The Bank’s core measures of inflation continued to move up, ranging from 5% to 5.5% in July. Surveys suggest that short-term inflation expectations remain high. The longer this continues, the greater the risk that elevated inflation becomes entrenched.”

In a nutshell, policymakers are worried that inflation may become entrenched, especially as domestic demand remains very strong.

So, why hit the brakes?

The BoC hiked rates by 100 bps on July 13 because 1) “inflation is too high, and more people are getting more worried that high inflation is here to stay. We cannot let that happen”. 2) “the Canadian economy is overheated.” 3) “our goal is to get inflation back to its 2% target. “To accomplish that, we are increasing our policy interest rate quickly to prevent high inflation from becoming entrenched.”

If the BoC believed what they said in July, rates would have risen by 100 bps. Officials were happy to point out that CPI inflation eased in July, to 7.6% from 8.1% in June. That is just cherry-picking data.

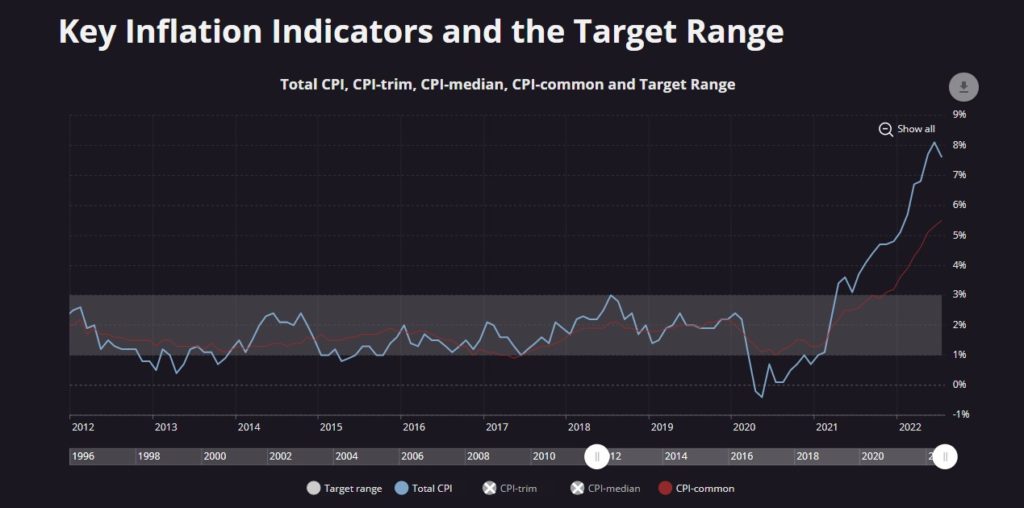

The BoC has three preferred measures of inflation (CPI-Trim, CPI-Median, and CPI-Common). Of the three, the BoC claims CPI-Common is the best gauge of the economy’s performance.

CPI-Common rose to 5.5% in July from 5.3%, which if the BoC’s rhetoric was to be believed, warranted another 100 bp hike, especially as the latest statement warns of even more rate hikes.

Why wait?

Chart: BoC inflation-Blue line CPI, Red line CPI-Common

Source: Bank of Canada

At the end of the day, it’s just nit-picking. Global investors do not care about the Bank of Canada’s monetary policy unless it deviates sharply from the Fed’s.

Fed Chair Jerome Powell is an inflation hawk, at least that’s the impression he gave to the audience at the Jackson Hole Symposium on August 26.

He opened his speech with a blunt statement saying, “The Federal Open Market Committee’s (FOMC) overarching focus right now is to bring inflation back down to our 2 percent goal.”

Unlike the BoC, Mr Powell was not impressed with the lower inflation reading in July, saying “a single month’s improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down.”

Cleveland Fed President Loretta Mester doubled down on Mr Powell’s comments and predicted that fed funds would be over 4.0% by year-end and stay at or above that level for all of 2023.

The hawkish sentiment took hold and then accelerated post-Labor Day, fueled by a sharp jump in the US 10-year yield, which went from 3.02% on August 25 to 3.65% on September 7.

Mick Jagger’s stage moves were once described as “akin to a rooster on acid,” which is an apt metaphor for how global markets react to US Treasury yield moves.

The Fed is going to greet the arrival of autumn with a 75 bp rate hike on September 21, which makes one wonder why the BoC is tapping the rate hike brakes.