By Michael O’Neill

The Bank of Canada left its benchmark rate unchanged at 2.75% this morning, which surprised about half the market. But “unchanged” doesn’t mean “unmoved.” The central bank now finds itself tap-dancing in an economic minefield. As the Monetary Policy Report put it: “The unpredictability of U.S. trade policy, and the speed and magnitude of the shifts, are making the economic outlook very uncertain.”

The Canadian economic outlook took a nasty turn for the worse. It was just over a month ago, when the BoC cut rates by 25 basis points due to what appeared to be strong economic momentum and fading inflation. It was viewed as a pre-emptive cut as policymakers adopted a “wait-and-see” attitude because of American tariff threats.

The waiting is over and what they see is akin to a 17th century painting of a biblical massacre (Peter Paul Rubens’ or Caravaggio). It isn’t pretty. Now final domestic demand has stalled. Consumer spending shrank from 5.5% in Q4 to just 1.5% in Q1. Residential investment, previously roaring at 17%, plunged by 7%. Business investment pulled the brakes entirely, down 2%. Job growth in March, and the unemployment rate is creeping up again.

Tariffs and Trade Tantrums

The culprit behind this mess? No surprise: Washington. Since February, the U.S. has ricocheted between imposing, suspending, and reimposing tariffs like a toddler with a light switch. Steel, aluminum, motor vehicles—you name it, it’s taxed. Canada’s response has been measured but direct, with countermeasures targeting $115 billion in U.S. goods and select retaliatory tariffs on vehicles.

The BoC admits that the sheer scale and unpredictability of these actions make modeling nearly useless. Households are worried. Businesses are paralyzed. Inventories were hoarded in Q1 to beat tariff deadlines—meaning Q2 trade will probably collapse. Exports and imports are expected to fall off a cliff, and inflation, once a steady ship, could capsize under pressure from tariff-driven input costs.

Keep Your Powder Dry

But despite all this, the Bank held its fire. Why?

That’s easy—they didn’t even pretend to have a handle on things. So, it published two scenarios:

Scenario 1: A muddle-through world where most tariffs get negotiated away and inflation dips below target temporarily before returning to 2%.

Scenario 2: A full-blown global trade war where Canada slides into a year-long recession, core inflation spikes above 3%, and potential output gets permanently kneecapped.

Arguably, the first scenario is the Goldilocks outcome. It assumes that the U.S. administration has a well-planned strategy for using, or threatening to use, tariffs to repatriate manufacturing jobs and reduce its trade deficit. But that assumption goes out the window when you remember that the White House levied tariffs on an Antarctica area island solely populated by penguins.

The second scenario is the most likely, but the Bank of Canada can hardly stress that the economy is heading into the dumpster, especially with a federal election going on, even though that is the direction.

But Governor Tiff Macklem and company cannot even be sure of that outcome due to constantly shifting U.S. tariffs.

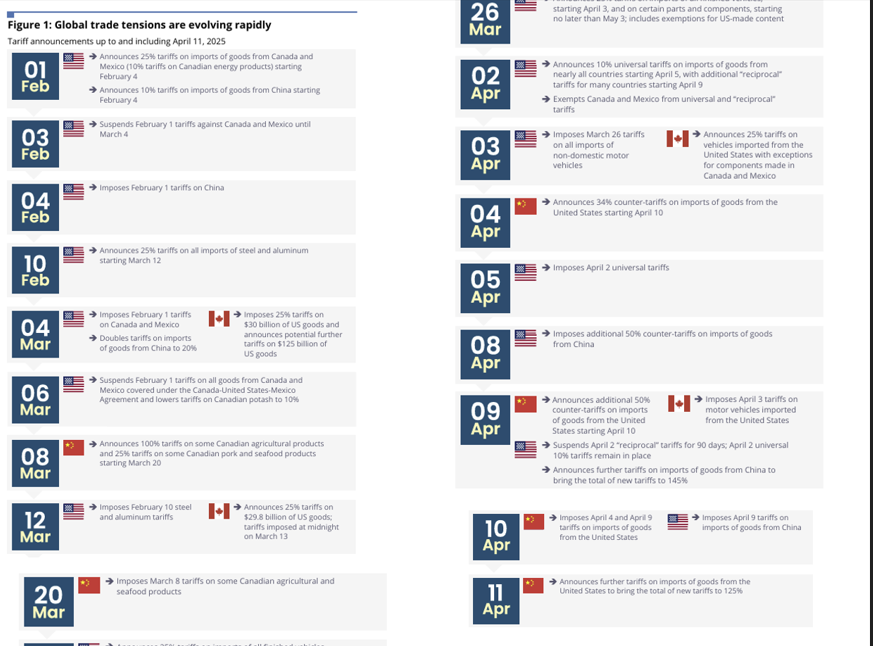

The BoC Monetary Policy Report graphically explains why.

Global Tariff Timeline

The global tariff timeline is a chaotic mess of sudden impositions, reversals, and retaliatory measures. Businesses don’t know whether to hoard inventory, delay investment, or reroute supply chains, because trade rules seem to change by tweet. The uncertainty has neutered traditional economic models, and central banks, including the BoC, have been forced to abandon baseline forecasts in favor of scenario planning. It’s a craps game with loaded dice.

Are the Loonie’s Days Numbered?

The BoC is frozen, and fundamentals are in flux, so why would the Canadian dollar rally after the BoC left rates unchanged? The simple reason is the narrowing of Canada and U.S. interest rate differentials. Fed Governor Christopher Waller made a good case for why the Fed needs to cut rates when he spoke on Monday, and with the BoC hitting pause, the U.S. dollar, already under broad-based selling pressure, becomes more unattractive.

However, the sustainability of the gains is questionable. Fundamentally, the rising odds for a deep and long-lasting Canadian recession while U.S. economic growth slows sharply is never a recipe for Canadian dollar gains, and this time will be no different. If Scenario 2 gains traction, the BoC will be forced to cut further, even if inflation is temporarily above 2%.

That’s bearish CAD, and for importers and consumers, a reason to be “Tariffied.”

{kind=link}

.jpg){kind=link}