Brexit fever has gone viral, although not in the YouTube sense of the word. The Brexit virus has spread throughout global markets; from equities and commodities to fixed income and foreign exchange. And lately, it has infected the major central banks of the world.

Brexit is the term coined by pundits to describe the UK referendum on European Union membership. The debate began on February 20, when UK Prime Minister, David Cameron announced that the referendum vote would be held on June 23, 2016.

The referendum ballot asks the question: “Should the United Kingdom remain a member of the European Union or leave the European Union”?

The question also determined the two sides for Pollsters-Remain and Leave.

There have been numerous polls since the referendum was announced and for the most part, FX moves were mostly contained to GBPUSD and EURGBP. That has changed as we make the club-house turn and gallop down the home stretch Since last week, the impact of poll results has leaked into the other G10 currencies and have had an out-sized impact on FX markets.

If the Remain side wins, the world can go back to fretting about when the Fed hike rates or when the Bank of Japan will provide more stimulus. The Remain side which includes the Prime Minister warns that quitting the EU would lead to job losses, higher taxes, a recession and higher mortgage costs. Those views appear to echoed by the Bank of England, the Organization for Economic Cooperation and Development (OECD) and the International Monetary Fund (IMF) Or as the leave side would say “the ruling elite”.

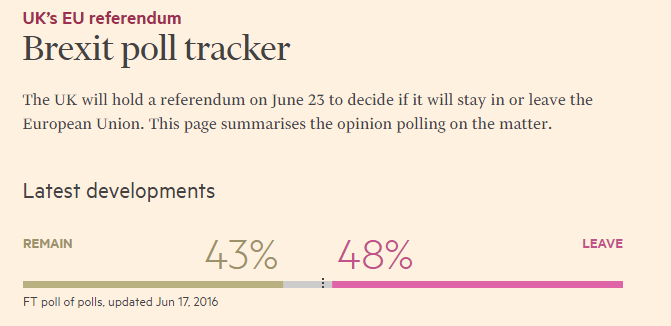

The risk to markets is “What happens if the Leave side wins”? No one really knows and therein lies the problem. Uncertainty breeds volatility and that it is why the poll results have wreaked havoc across asset classes. As of June 17, the Leave side has a 5 percentage point lead over the Remain side

Financial Times Poll of Polls tracker as of June 17, 2013

UK has Brexit Fever and the Fed gets Cold Feet

The Federal Reserve has a bit of a reputation for focussing too closely on the domestic economy while ignoring or downplaying international developments. As they should. Their mandate is to set monetary policy to promote the objectives of maximum employment, stable prices and moderate long term interest rates for the Untied States of America, not the world.

Unfortunately, the world intruded into their little clubhouse. Fed Chair Janet Yellen gave financial markets a “heads-up” just two weeks ago when she said that it would be appropriate to raise the overnight interest rate in the coming months. Then she chopped their heads off.

On Wednesday, the FOMC left rates unchanged and downgraded both their GDP and interest rate outlooks.

During her press conference following the release of the interest rate statement, Ms. Yellen said about Brexit,” It was fair to say that it was one of the factors that factored into today’s decision”. She went on to say that Brexit could have “consequences” for the US economic outlook.

And Bank of Japan gets chills

A few hours after the FOMC announcement, the Bank of Japan stepped onto the podium. The BoJ was expected to leave rates unchanged and that’s just what they did. At the same time, their was a market faction that expected some sort of stimulus measures to counter the effects of falling inflation and the rising yen. There wasn’t any and USDJPY got thrashed. During his press conference, BoJ Governor, Haruhiko Kuroda, said that the central bank was closely monitoring financial markets and was in touch with the Bank of England due to Brexit concerns which he said impacted bond markets. Those words injected risk aversion into global markets.

Wild Thing Making Hearts Sing

Mr. Toads Wild Ride has nothing on the recent FX activity. When the sign said that “You must be this high to ride”, it wasn’t referring to Colorado’s newest past-time. However, in these markets, that may not be such a bad thing.

Since Thursday morning in Europe, the US dollar has been up and down like a fat man on a pogo stick. Sterling was a big mover. GBPUSD dropped from 1.4202 to 1.4010 and then back to 1.4293 in Asia on Friday morning, a 0.500 point move when you include travel time. USDJPY had a similar day. It dropped from 106.10 to 103.55 and then back to 104.85. EURUSD recouped almost all of it’s 0.180 point loss. The commodity bloc currencies were just as choppy.

Brexit is Patient Zero for the FX Moves

The FX volatility in the past 24 hours can be traced back to events in the UK. A Labour MP, Jo Cox, was brutally murdered in an attack some claim was related to her support for the “Remain” campaign. The US dollar sell-off began when the news was announced with some believing that her death will boost the fortunes of the Remain camp.

That may be the case for the GBPUSD rally but for the other G10 currencies it was just one factor. FX traders had bought US dollars in anticipation of a hawkish bent to the FOMC statement with the Brexit frenzy fueling the demand. Intraday positions may have gotten a tad overdone and when the dollar sellers triggered the first stop loss it caused a stampede for the exits.

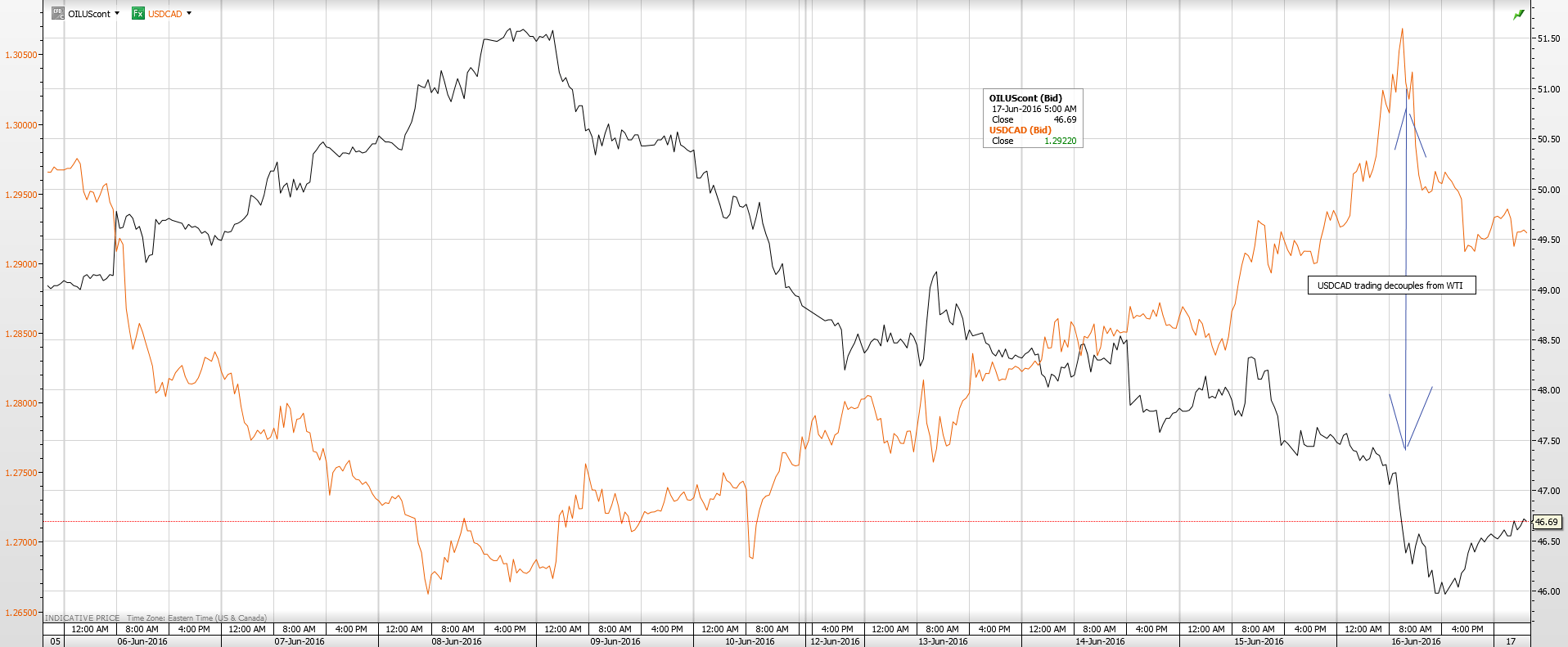

The Loonie is the proof

USDCAD soared to 1.3085 on Thursday and hit 1.2901 in early Asia trading while WTI fell from $48.75 on Wednesday to $45.80 at the New York close on Thursday. Normally the Loonie doesn’t rise when oil prices are falling. That move suggests that other factors are at play. Those other factors included a reduction in stretched long intraday USDCAD positions due to a more benign Fed outlook and the (very slightly) diminished risks that the Brexit Leave side will prevail do the murder.

Chart: USDCAD and WTI oil 30 minute chart

Source: Saxo Bank

It Ain’t Over until the Fat Brexit Lady Sings

The volatility of the past few days and weeks isn’t going to disappear anytime soon. In fact, if the UK polls prove correct and the “Leave” camp prevails, FX volatility will increase for a long time. There have been a number of press reports indicating that if Britain leaves the EU, other nations my follow or at least attempt to renegotiate their membership. The Brexit saga would drag on, akin to the Greek debt crisis, as the British government attempts to negotiate new trade deals with a jilted EU.

The Canadian dollar may be a bystander in all of this, but not an idle one. USDCAD volatility may increase due to safe-haven Canadian dollar demand which may act as a bit of a brake against USDCAD demand from falling oil prices due to slowing global growth. Brexit fever has indeed gone viral.